Master HELOC vs Cash-Out Refinance Strategy [2025]

![Master HELOC vs Cash-Out Refinance Strategy [2025]](/_next/image?url=https%3A%2F%2Fcdn.sanity.io%2Fimages%2F2a445j5i%2Fproduction%2F07c10026f046d7cb8b0ee80e97a01d376b45b635-1024x585.jpg%3Fauto%3Dformat&w=3840&q=75)

Table of Contents

Navigating the world of home equity can be complex, especially when choosing between a HELOC and a cash-out refinance. These two popular options offer homeowners different ways to tap into their property's value.

At HELOC360, we've seen firsthand how the right HELOC strategy can transform a homeowner's financial outlook. This guide will break down the key differences between HELOCs and cash-out refinances, helping you make an informed decision for your unique situation.

What Are HELOCs and Cash-Out Refinances?

HELOCs: Flexible Borrowing Power

A Home Equity Line of Credit (HELOC) offers a revolving credit line secured by your home. It functions like a credit card but with significantly lower interest rates. You can borrow up to a set limit, repay, and borrow again during the draw period (typically 5 to 10 years).

HELOCs excel for ongoing expenses or projects with uncertain costs. For instance, a kitchen renovation with an unclear final bill allows you to draw funds as needed. A key advantage: you only pay interest on what you borrow, potentially leading to substantial savings compared to lump-sum loans.

Cash-Out Refinance: Lump Sum Liquidity

A cash-out refinance pays off your existing first mortgage. This results in a new mortgage loan which may have different terms than your original loan. You receive the difference between your new loan amount and your current mortgage balance in cash.

This option suits homeowners who need a large sum upfront and accept a new mortgage term. It's particularly useful for major one-time expenses (debt consolidation or funding a child's education).

Cash-out refinances often feature fixed interest rates, providing stable monthly payments. However, they typically involve higher closing costs than HELOCs.

Tapping Into Home Equity

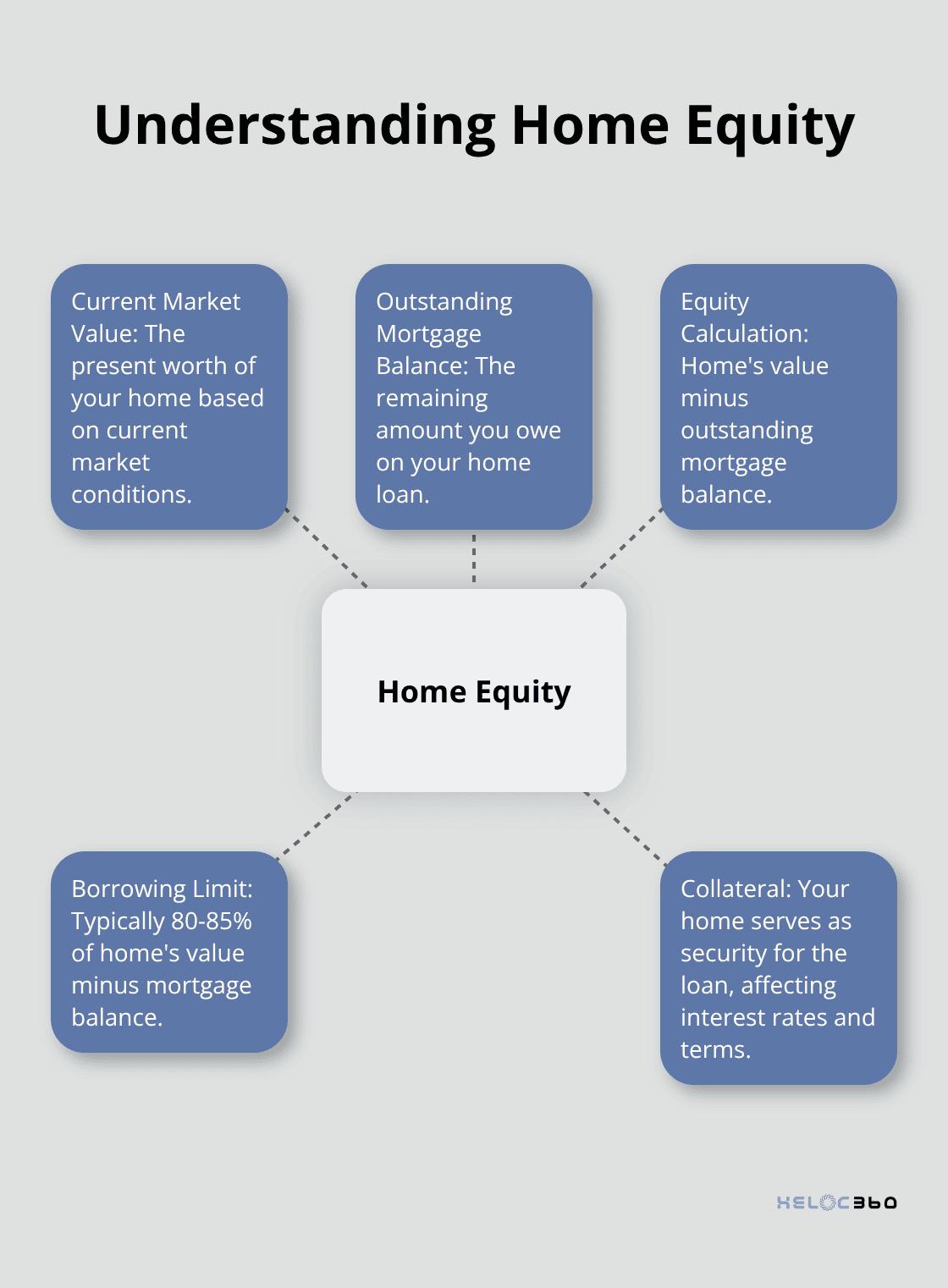

Both HELOCs and cash-out refinances allow you to access your home's equity. Home equity represents the difference between your home's current market value and your outstanding mortgage balance.

Example: If your home is worth $400,000 and you owe $250,000 on your mortgage, you have $150,000 in home equity. Lenders usually allow borrowing up to 80–85% of your home's value minus your outstanding mortgage balance.

Collateral Considerations

It's crucial to note that both options use your home as collateral. This results in lower interest rates compared to unsecured loans, but it also means your home is at risk if you default on payments.

Choosing the Right Option

Your choice between a HELOC and a cash-out refinance depends on your specific financial needs and goals. Consider factors such as:

- The amount you need to borrow

- Your preferred repayment structure

- Your current mortgage terms

- Your long-term financial plans

As we move forward, we'll compare these options in more detail to help you make an informed decision that aligns with your unique situation.

How Do HELOCs and Cash-Out Refinances Compare?

Interest Rates and Repayment Terms

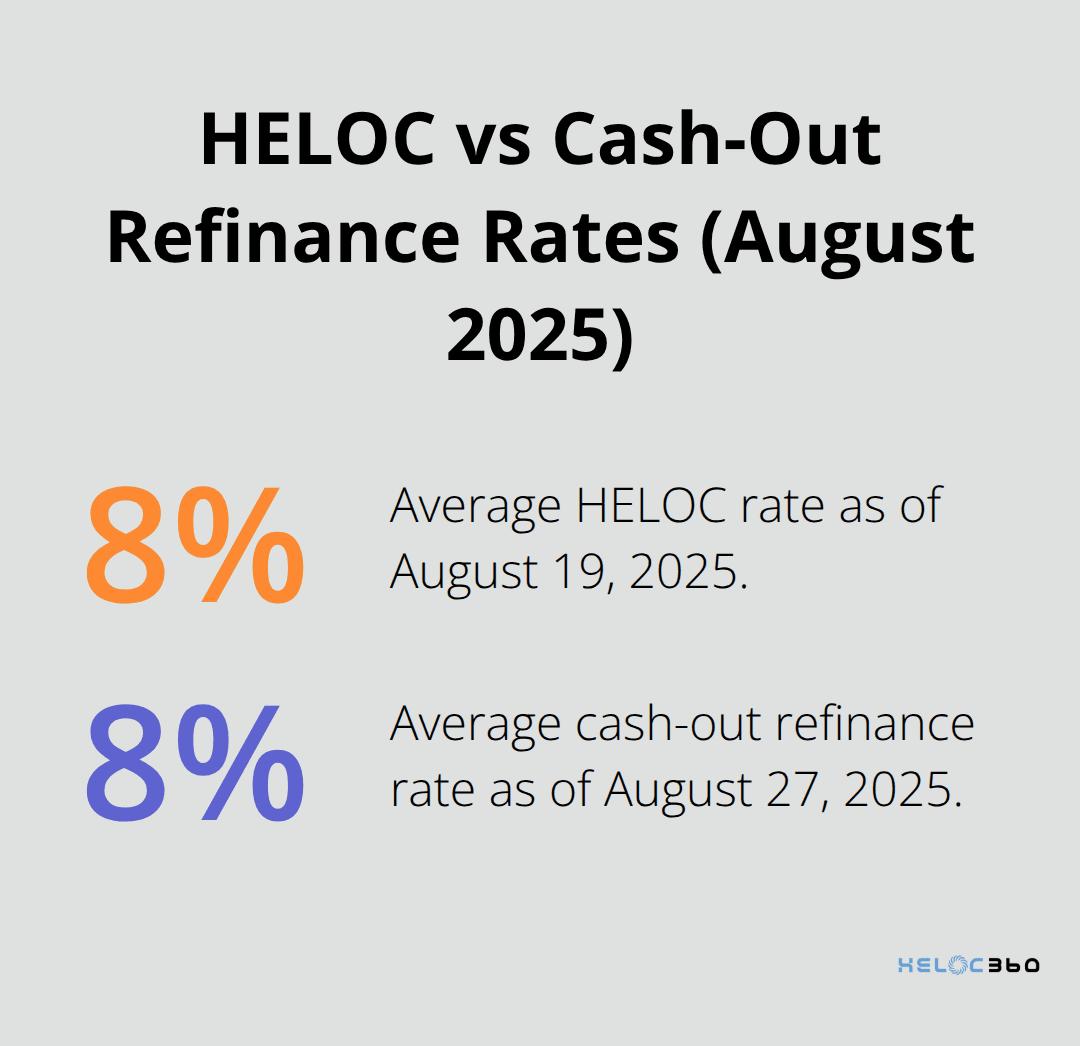

HELOCs typically feature variable interest rates, which fluctuate based on market conditions. As of August 19, 2025, the average home equity loan rate is 8.23%, according to Bankrate's regular survey of rates. These rates often link to the prime rate, so they can change over time.

Cash-out refinances usually offer fixed interest rates. The national average home equity loan interest rate is 8.22% as of August 27, 2025, according to Bankrate's latest survey of the nation's largest home equity lenders.

Repayment terms differ significantly. HELOCs have two phases: a draw period (usually 5–10 years) where borrowers can access funds and make interest-only payments, followed by a repayment period. Some draw periods can be as short as three or five years. Cash-out refinances function like traditional mortgages, with set terms typically ranging from 15 to 30 years.

Borrowing and Repayment Flexibility

HELOCs offer unmatched flexibility. Borrowers can access funds up to their credit limit, repay, and borrow again. This makes HELOCs ideal for ongoing expenses or projects with uncertain costs.

Cash-out refinances provide a lump sum upfront. While this benefits large, one-time expenses, it lacks the revolving nature of a HELOC. Borrowers commit to the full loan amount from day one.

Credit Score and Debt-to-Income Impact

Both options affect credit scores and debt-to-income (DTI) ratios differently. HELOCs are revolving credit, similar to credit cards. Using a high percentage of available credit can negatively impact credit scores. However, responsible use can potentially improve scores over time.

Cash-out refinances replace existing mortgages with larger ones. This increased debt load could raise DTI ratios, potentially making it harder to qualify for other loans in the future. However, using the cash to pay off high-interest debt might improve credit scores.

Closing Costs and Fees

Cash-out refinances typically involve higher closing costs, averaging 2–5% of the loan amount. These costs can include appraisal fees, title insurance, and origination fees.

HELOCs generally have lower upfront costs. Some lenders even offer no-closing-cost HELOCs, but this often means higher interest rates or annual fees.

The choice between a HELOC and a cash-out refinance depends on individual financial needs and goals. A HELOC might suit those who need ongoing access to funds and can manage variable rates. A cash-out refinance could benefit those who need a large sum upfront and want fixed payments. Both options use your home as collateral, so careful consideration and professional advice can help make the best decision.

Which Option Fits Your Financial Needs?

Evaluating if a HELOC aligns with your financial goals is crucial when deciding between a HELOC and a cash-out refinance. Each option has its strengths, and the best choice depends on your specific situation.

HELOCs: Flexibility for Ongoing Expenses

HELOCs excel for ongoing or unpredictable expenses. If you plan a multi-phase home renovation or need funds for recurring costs like college tuition, a HELOC offers the flexibility to borrow as needed. This can lead to significant interest savings compared to taking out a lump sum upfront.

For example, if you start a small business from home, a HELOC allows you to draw funds for equipment or inventory as your business grows. You only pay interest on the amount you use, making it a cost-effective option for fluctuating expenses.

HELOCs also work well for those who want to maintain their current mortgage terms. If you've secured a low interest rate on your existing mortgage, a HELOC lets you tap into equity without disturbing those favorable terms.

Cash-Out Refinances: Ideal for Large, One-Time Expenses

Cash-out refinances suit large, one-time expenses best. If you need a substantial sum for debt consolidation, a major home improvement project, or to purchase an investment property, a cash-out refinance provides immediate access to funds.

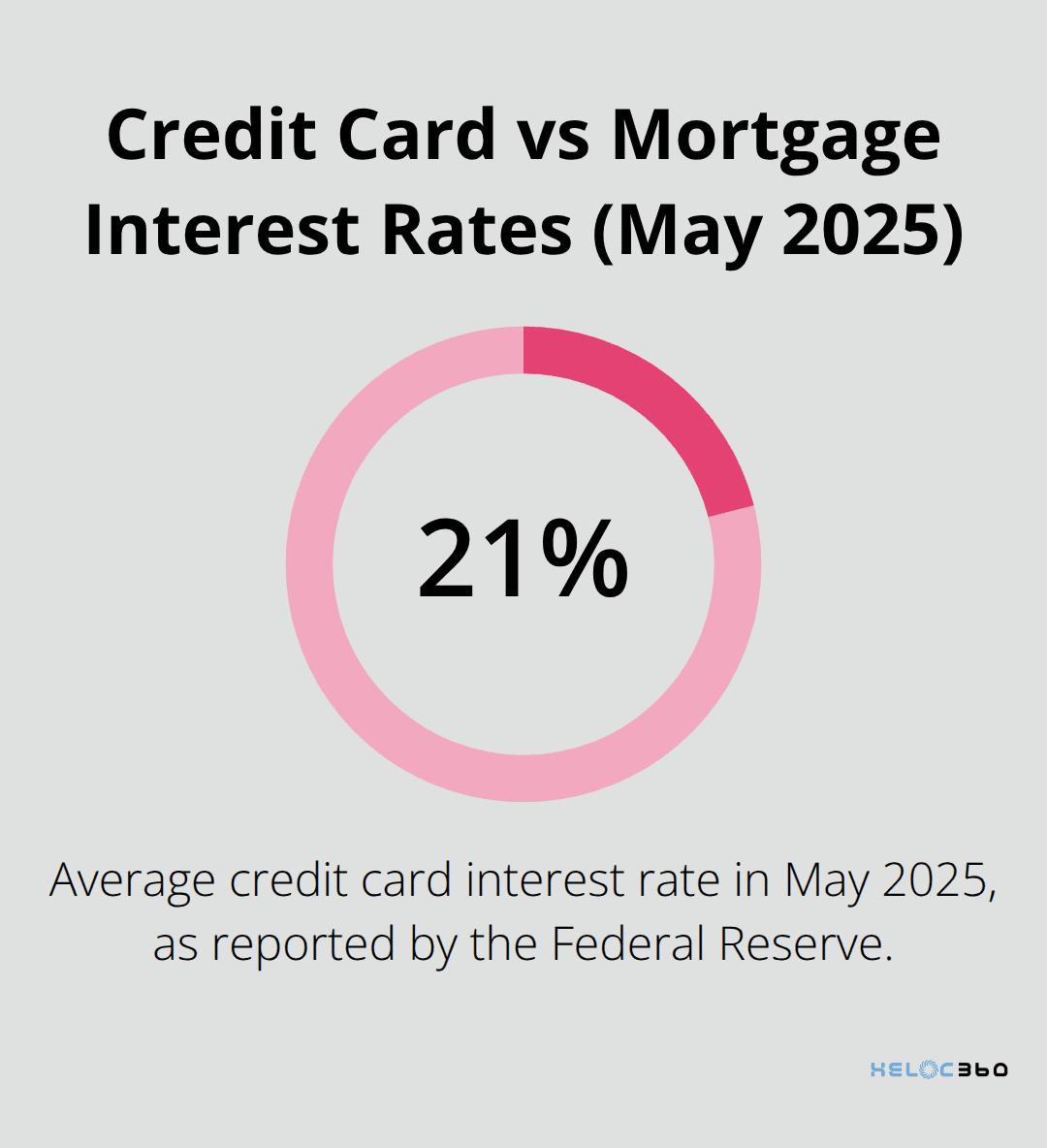

For instance, if you carry high-interest credit card debt, a cash-out refinance could help you pay it off at a much lower interest rate. The Federal Reserve reported that the average credit card interest rate was 21.16% in May 2025, while mortgage rates were significantly lower.

Cash-out refinances also make sense if current mortgage rates are lower than your existing rate. You could potentially lower your monthly payments while accessing your home equity.

Aligning with Your Financial Goals

Your long-term financial objectives play a key role in this decision. If you plan to stay in your home for many years and want predictable payments, a cash-out refinance with a fixed rate might be the better choice.

On the other hand, if you value flexibility and anticipate varying financial needs over time, a HELOC could be more appropriate. This holds true especially if you feel comfortable managing a variable interest rate.

Tax Implications to Consider

Both HELOCs and cash-out refinances can have tax implications. As of 2025, interest you pay on the borrowed funds is classified as home acquisition debt and may be deductible, subject to certain dollar limitations.

For cash-out refinances, if the new loan amount exceeds your original mortgage balance by more than $750,000 for married couples filing jointly ($375,000 for single filers), the interest on the excess amount isn't tax-deductible.

It's important to consult with a tax professional to understand how these options might affect your specific tax situation. The rules can be complex, and individual circumstances vary widely.

Making the Right Choice

The decision between a HELOC vs Cash-Out Refinance depends on your specific financial situation and goals. Try to assess your needs carefully, understand the terms of each option, and choose the one that aligns best with your long-term financial strategy.

(Note: The information provided here is general in nature. For personalized advice, consult with a financial professional who can evaluate your unique circumstances.)

Final Thoughts

The choice between a HELOC and a cash-out refinance depends on your financial goals and current situation. HELOCs provide flexibility with revolving credit and lower upfront costs, while cash-out refinances offer a lump sum at a fixed rate. Your decision should account for interest rates, repayment terms, and the impact on your credit score and debt-to-income ratio.

A sound HELOC strategy or cash-out refinance decision requires careful consideration of your long-term financial objectives. You should assess how long you plan to stay in your home and your comfort level with variable interest rates. Tax implications also play a role, as interest deductibility can vary between these options (consult a tax professional for personalized advice).

HELOC360 can guide you through the process of unlocking your home's equity potential. We understand that every homeowner's situation is unique and aim to provide tailored solutions. Our platform connects you with lenders that match your specific needs, helping you create new financial opportunities and work towards achieving your aspirations.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.