Maximizing Your HELOC Credit Line A Homeowner's Guide

Table of Contents

At HELOC360, we understand that homeowners are always looking for ways to make the most of their property's value. A HELOC credit line can be a powerful financial tool when used wisely.

This guide will show you how to maximize your HELOC, from understanding the basics to implementing smart strategies for increasing your credit limit. We'll also explore responsible ways to use your HELOC that can potentially improve your financial situation.

Understanding Your HELOC Credit Line

What is a HELOC?

A Home Equity Line of Credit (HELOC) allows homeowners to access their property's equity. This financial tool provides a revolving credit line secured by your home, often with lower interest rates than unsecured loans. It's important to note that lenders may freeze or reduce your credit line if your home's value decreases or if they notice a negative change in your financial situation.

How a HELOC Functions

When you open a HELOC, the lender sets a credit limit based on your home's value and outstanding mortgage balance. The HELOC operates in two phases:

- Draw Period: This phase lasts 5-10 years. You can borrow up to your credit limit and pay interest only on the amount you use.

- Repayment Phase: After the draw period, you enter a 10-20 year repayment phase. You can no longer withdraw funds and must repay both principal and interest.

Factors Influencing Your HELOC Credit Limit

Lenders consider several elements when determining your HELOC credit limit:

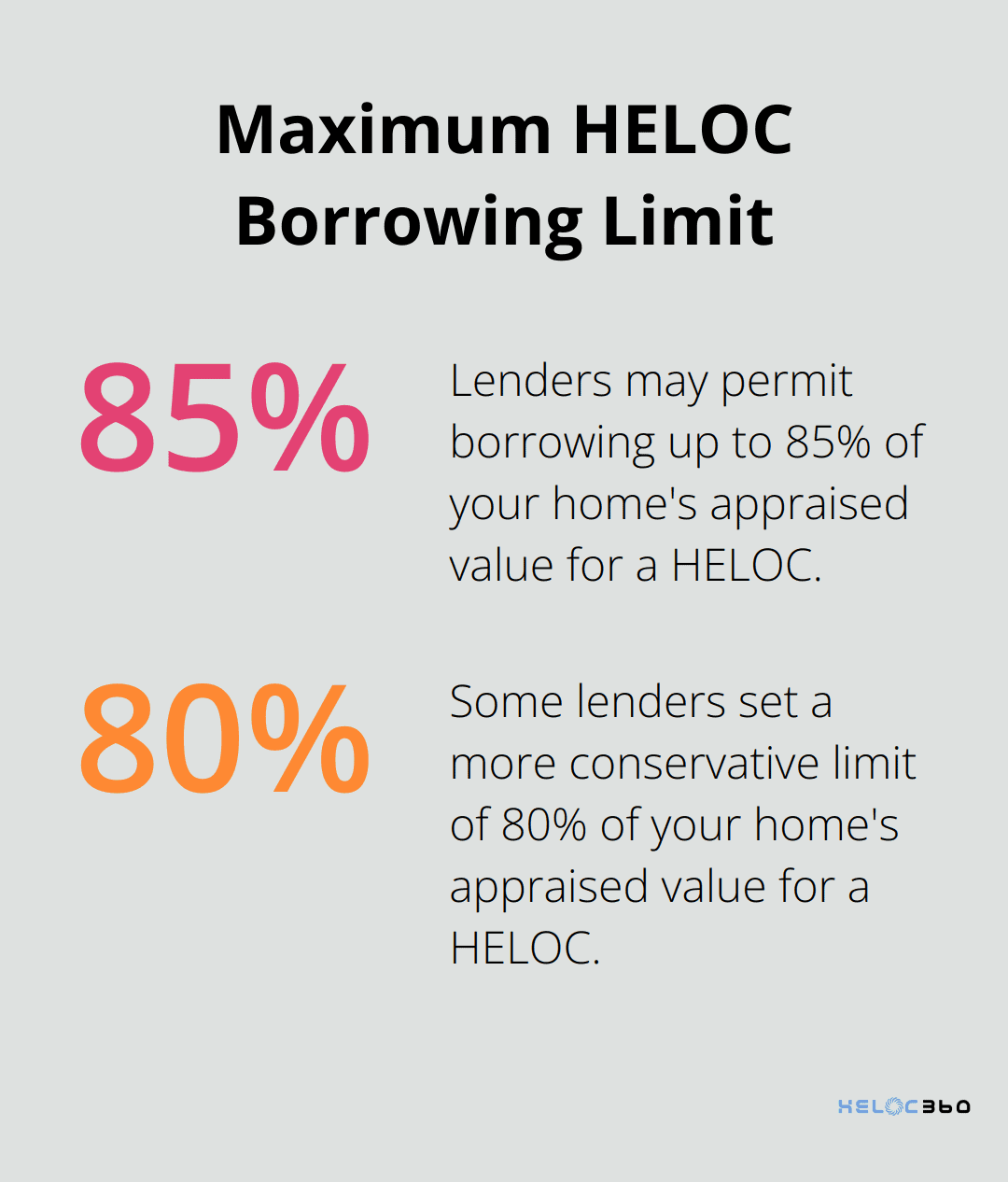

- Home Value: Most lenders permit borrowing up to 80%-85% of your home's appraised value (minus your outstanding mortgage balance).

- Credit Score: A higher score (ideally 740 or above, according to Experian) can lead to a higher credit limit and better terms.

- Debt-to-Income Ratio (DTI): Lenders typically prefer a DTI of 43% to 50% at most, with some requiring even lower ratios. A lower DTI could result in a higher credit limit.

- Income Stability: Consistent, verifiable income improves your chances of securing a higher credit limit.

HELOC vs. Home Equity Loan

While both use your home's equity as collateral, HELOCs and home equity loans differ in several ways:

- Disbursement: A HELOC provides a revolving credit line (similar to a credit card), while a home equity loan gives you a lump sum upfront.

- Interest Rates: HELOCs typically have variable rates, while home equity loans often offer fixed rates.

- Repayment: With a HELOC, you pay interest only on what you borrow during the draw period. Home equity loans require immediate repayment of both principal and interest.

- Flexibility: HELOCs offer more flexibility in borrowing and repayment, making them suitable for ongoing expenses or projects with uncertain costs.

Understanding these differences helps you choose the right option for your financial needs. HELOCs provide great flexibility but require discipline in managing variable payments. Home equity loans offer more predictability but less flexibility.

As you consider your options, it's important to evaluate your financial goals and risk tolerance. The next section will explore strategies to increase your HELOC credit line, helping you maximize the potential of your home equity.

How to Boost Your HELOC Credit Line

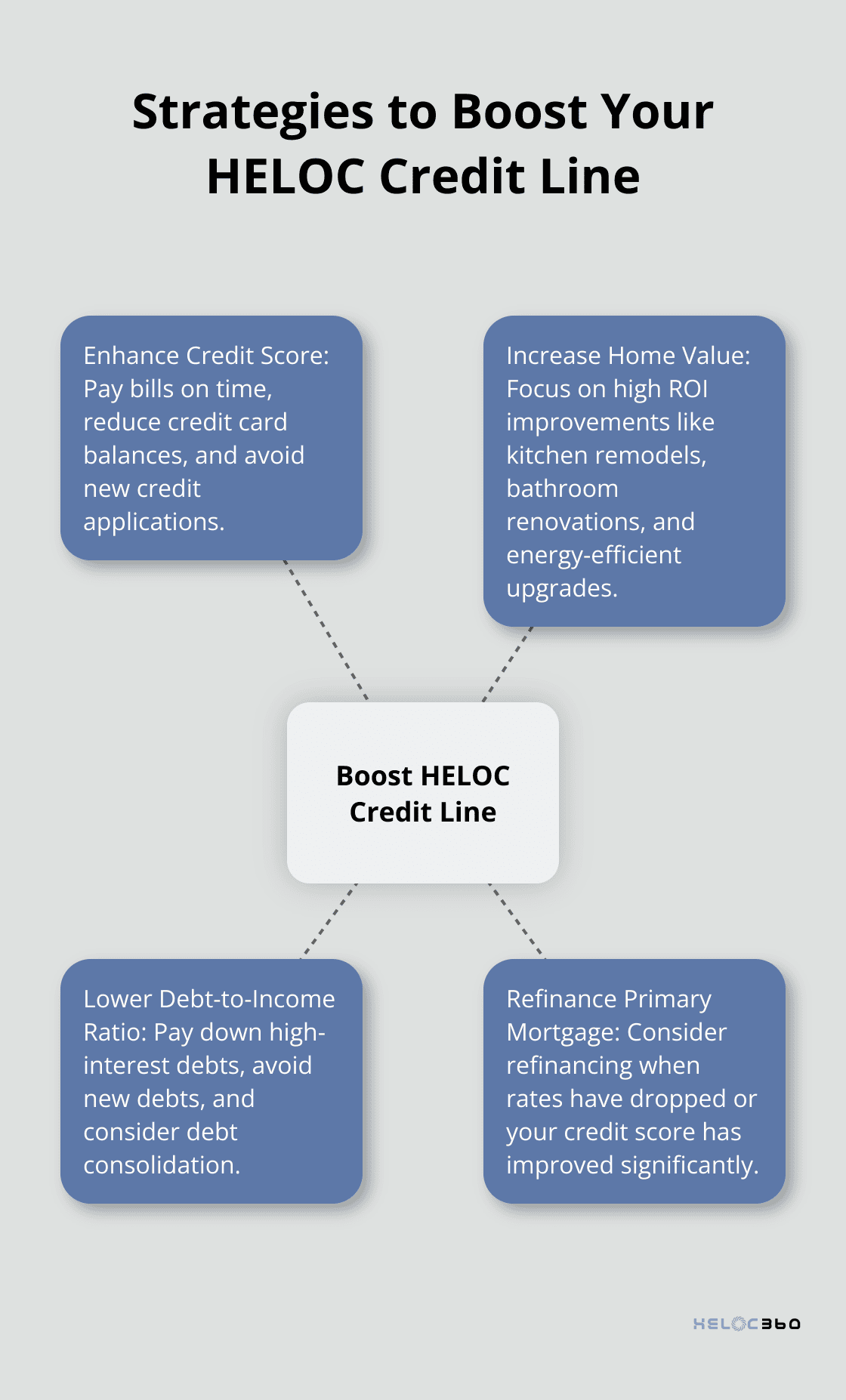

Enhance Your Credit Score

Your credit score significantly influences your HELOC credit limit. A score of 620 or above can secure better terms, with some lenders requiring higher scores. To improve your score:

- Pay all bills on time

- Reduce credit card balances to below 30% of their limits

- Avoid new credit applications before your HELOC application

- Review your credit report and dispute any inaccuracies

Increase Your Home's Value

Boosting your home's value directly impacts your available equity and potential HELOC limit. Focus on improvements with high return on investment (ROI):

- Kitchen remodels (96.1% ROI for minor remodels)

- Bathroom renovations

- Energy-efficient upgrades

Document all improvements to support a higher appraisal value when applying for or refinancing your HELOC.

Lower Your Debt-to-Income Ratio

Lenders typically prefer a debt-to-income (DTI) ratio of less than 47%. To improve your DTI:

- Pay down high-interest debts (especially credit cards)

- Avoid new debts before applying for a HELOC

- Consider debt consolidation to lower monthly payments

- Increase your income through side gigs or a raise (if possible)

Refinance Your Primary Mortgage

Refinancing your first mortgage can free up equity for a larger HELOC. This strategy works best when:

- Interest rates have dropped significantly since your original mortgage

- You've built substantial equity in your home

- Your credit score has improved since your initial mortgage application

Weigh the costs against potential benefits before refinancing. Closing costs typically range from 2% to 5% of the loan amount, so ensure long-term savings outweigh upfront expenses.

These strategies can significantly increase your HELOC credit line. However, it's important to approach this process responsibly. Try to assess your financial situation and long-term goals thoroughly before pursuing a larger credit line. The next section will explore smart ways to use your HELOC, helping you make the most of your increased borrowing power.

How Can You Use Your HELOC Wisely?

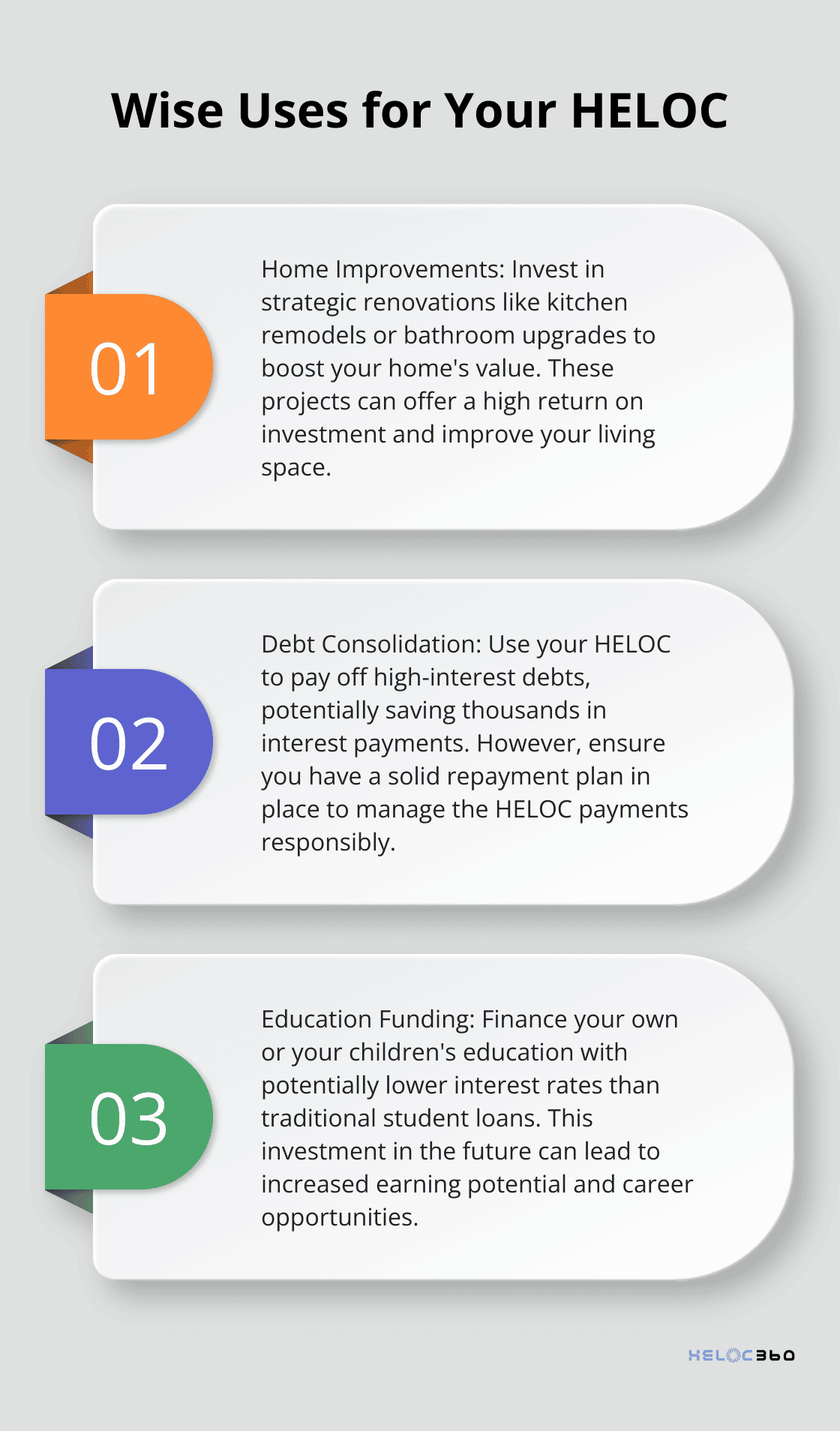

Boost Your Home's Value with Strategic Renovations

A Home Equity Line of Credit (HELOC) can serve as a powerful financial tool when used wisely. Many homeowners leverage their HELOCs to improve their financial situations and achieve their goals. One popular use for a HELOC is funding home improvements. The National Association of Realtors reports that kitchen remodels can yield a return on investment (ROI) of up to 80%. Bathroom renovations also offer a strong ROI, averaging 60-70%. When you plan renovations, focus on projects that enhance your living space and increase your home's market value.

Upgrading to energy-efficient appliances and windows can lower your utility bills and appeal to potential buyers if you decide to sell. For example, households installing residential solar have saved a median of $2,230 annually.

Tackle High-Interest Debt

Using a HELOC for debt consolidation can prove a smart move, especially if you face high-interest credit card debt. The average credit card interest rate hovers around 20%, while HELOC rates typically fall much lower. You could potentially save thousands in interest payments if you use your HELOC to pay off high-interest debts.

However, you must create a solid repayment plan. Your home serves as collateral, so ensure you can comfortably manage the payments.

Invest in Your Future

Education often represents a worthwhile investment, and a HELOC can help fund it. Whether you plan to return to school or save for your children's college education, using a HELOC can cost less than traditional student loans.

The College Board reports that the average cost of tuition and fees for the 2021-2022 school year reached $10,740 for in-state public colleges and $38,070 for private colleges. You might save significantly on interest compared to federal or private student loans if you use a HELOC to cover these costs.

Create an Emergency Fund

A HELOC can serve as a financial safety net. You can establish an emergency fund to cover unexpected expenses (such as medical bills or sudden home repairs). This approach can prevent you from resorting to high-interest credit cards or payday loans in times of crisis.

Fund Business Ventures

Entrepreneurs often use HELOCs to finance business startups or expansions. The lower interest rates compared to business loans or credit cards can make this an attractive option. However, you should carefully consider the risks involved in using your home equity for business purposes.

Final Thoughts

Maximizing your HELOC credit line requires a strategic approach and careful planning. You can potentially access more of your home's equity by improving your credit score, increasing your home's value, and managing your debt-to-income ratio. Refinancing your primary mortgage might also open up opportunities for a larger HELOC.

A HELOC offers flexibility and potentially lower interest rates compared to other financing options. You can use it to fund home improvements, consolidate high-interest debt, invest in education, or create an emergency fund. However, you must approach HELOC borrowing responsibly and have a solid repayment plan in place.

HELOC360 offers valuable support for homeowners looking to make the most of their home equity. This platform simplifies the process of exploring HELOC options, providing expert guidance and connecting you with lenders that match your specific needs. HELOC360 can help you unlock the full potential of your home's value and turn it into a powerful financial tool.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.