Can You Use a HELOC to Build Wealth?

Table of Contents

At HELOC360, we often get asked about innovative ways to build wealth. One strategy that's gaining traction is HELOC investing.

Home Equity Lines of Credit (HELOCs) offer a unique opportunity to leverage your home's value for potential financial growth. In this post, we'll explore how HELOCs can be used as wealth-building tools and discuss the strategies, risks, and considerations involved.

What Are HELOCs and How Can They Build Wealth?

The Mechanics of HELOCs

A Home Equity Line of Credit (HELOC) allows homeowners to borrow against the equity they've built in their property. HELOCs function similarly to a credit card, providing a revolving line of credit based on your home's equity. You can borrow up to a certain limit during a set draw period (typically 10 years) and only pay interest on the amount you use. After the draw period, you enter the repayment phase, where you pay back both principal and interest.

HELOC vs. Traditional Loans

HELOCs offer more flexibility compared to traditional loans that provide a lump sum. You can access funds as needed, which proves particularly advantageous for long-term projects or investments. This flexibility often results in lower overall interest payments compared to fixed loans, as you don't pay interest on unused funds.

Leveraging HELOCs for Wealth Creation

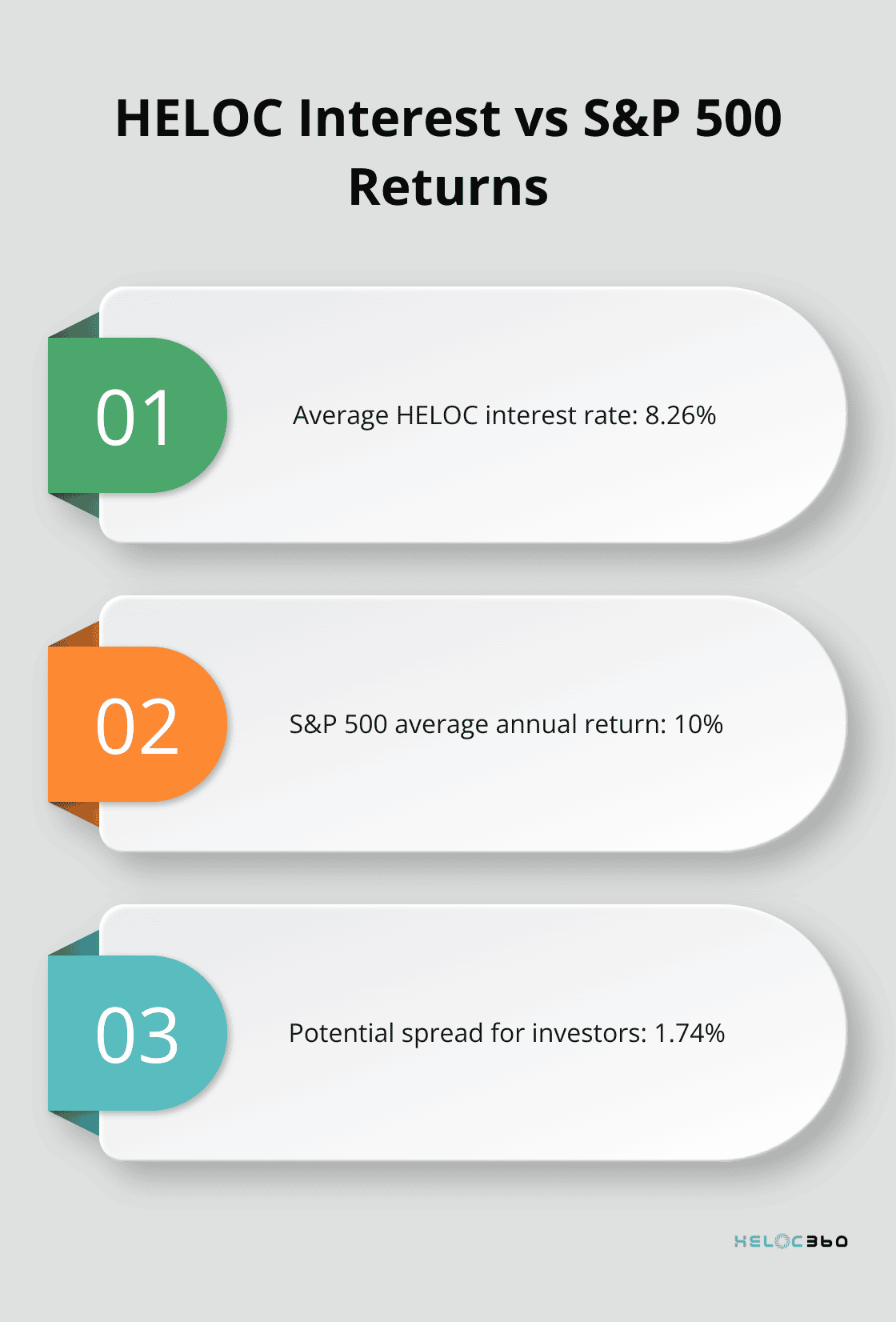

The potential for wealth creation with HELOCs lies in their ability to access large sums of money at relatively low interest rates. According to Bankrate, as of January 29, 2025, the average HELOC interest rate is 8.26% (significantly lower than many credit cards or personal loans).

This lower-cost borrowing can fund investments with potentially higher returns. For instance, the S&P 500 has historically provided an average annual return of about 10% over the long term. Using HELOC funds to invest in a diversified stock portfolio could potentially earn a spread between your borrowing costs and investment returns.

Real Estate Investments with HELOCs

Real estate investments represent another popular use of HELOCs. Using a HELOC to purchase rental properties or fund home improvements can increase your overall real estate portfolio value and generate additional income streams.

Risks and Considerations

It's important to approach HELOC investing with caution. The variable interest rates of HELOCs can fluctuate based on market conditions, potentially impacting your investment returns. Always consider your risk tolerance and have a solid repayment plan in place before using a HELOC for wealth-building purposes.

As we move forward, let's explore specific strategies for using HELOCs to build wealth, including real estate investments, home improvements, debt consolidation, and business expansion.

How to Leverage a HELOC for Wealth Building

Real Estate Investments: A Path to Passive Income

HELOCs offer a powerful tool for real estate investments. You can use HELOC funds as a down payment on a rental property. The median monthly mortgage payment is $2,040. This income could cover your HELOC payments while you build equity in a second property.

House flipping presents another opportunity. ATTOM Data Solutions reveals that the average gross profit on a flipped home stood at $67,000 in 2024 (before renovation costs). This figure highlights the potential for significant returns in real estate investing.

Home Improvements: Boost Your Property Value

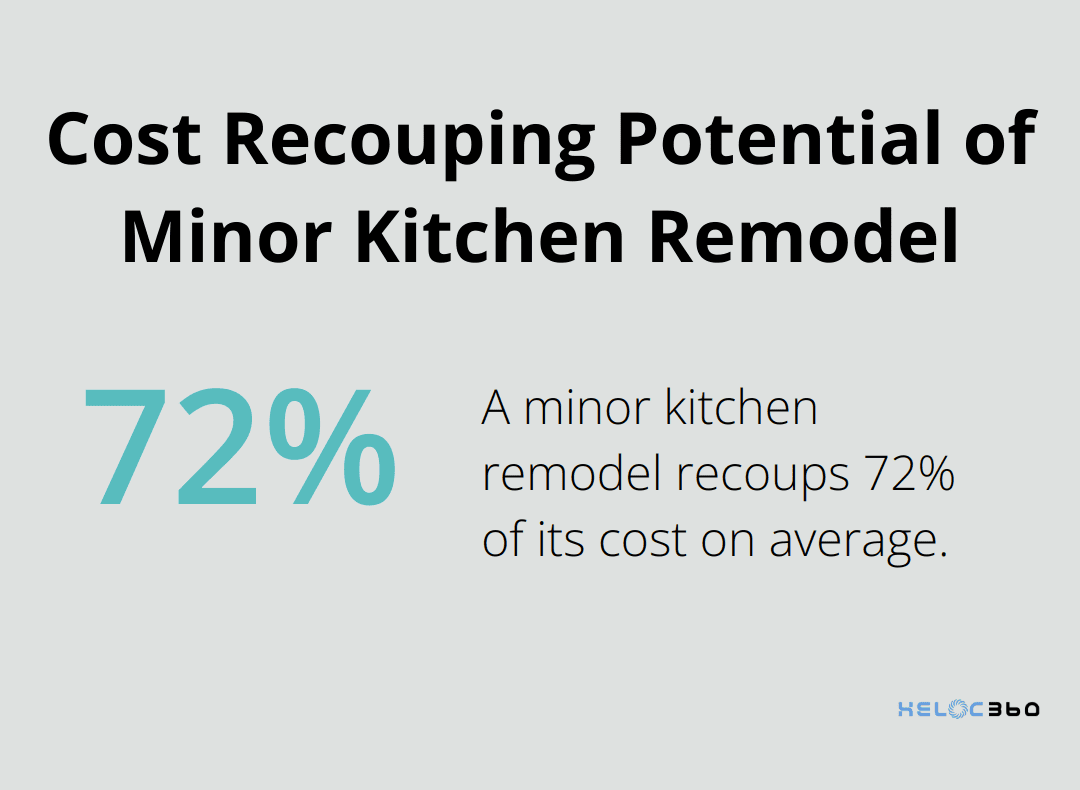

Strategic home improvements can increase your property value, creating more equity to borrow against in the future. A minor kitchen remodel recouped approximately 72% of its cost, according to the 2023 report. A $30,000 kitchen renovation could add $21,600 to your home's value.

Energy-efficient upgrades provide another smart option. The U.S. Department of Energy states that adding insulation can save homeowners an average of 15% on heating and cooling costs. These savings, combined with potential increases in home value, can offset the cost of using your HELOC for such improvements.

Debt Consolidation: A Strategic Financial Move

If you carry high-interest debt, using a HELOC to consolidate can save you money and accelerate wealth building. For example, $20,000 in credit card debt at 18% APR costs you $3,600 in interest annually. Consolidating this debt with a HELOC at 8% APR would reduce your annual interest to $1,600, saving you $2,000 per year.

Business Expansion: Fuel Your Entrepreneurial Dreams

For entrepreneurs, a HELOC can provide capital to start or expand a business. The average cost of launching a retail business is $32,000, and store owners have reported they started with only $5,000 saved. Using a HELOC for this purpose could prove more cost-effective than traditional business loans or credit cards.

When considering these strategies, you must create a solid plan for repayment and understand the associated risks. HELOCs can serve as powerful tools for wealth building, but they also put your home at risk if you can't repay the borrowed funds.

As you explore these wealth-building strategies, it's important to consider the potential risks and challenges that come with using a HELOC. Let's examine some key factors you should keep in mind to make informed decisions about leveraging your home equity.

What Are the Risks of Using a HELOC for Wealth Building?

The Challenge of Variable Interest Rates

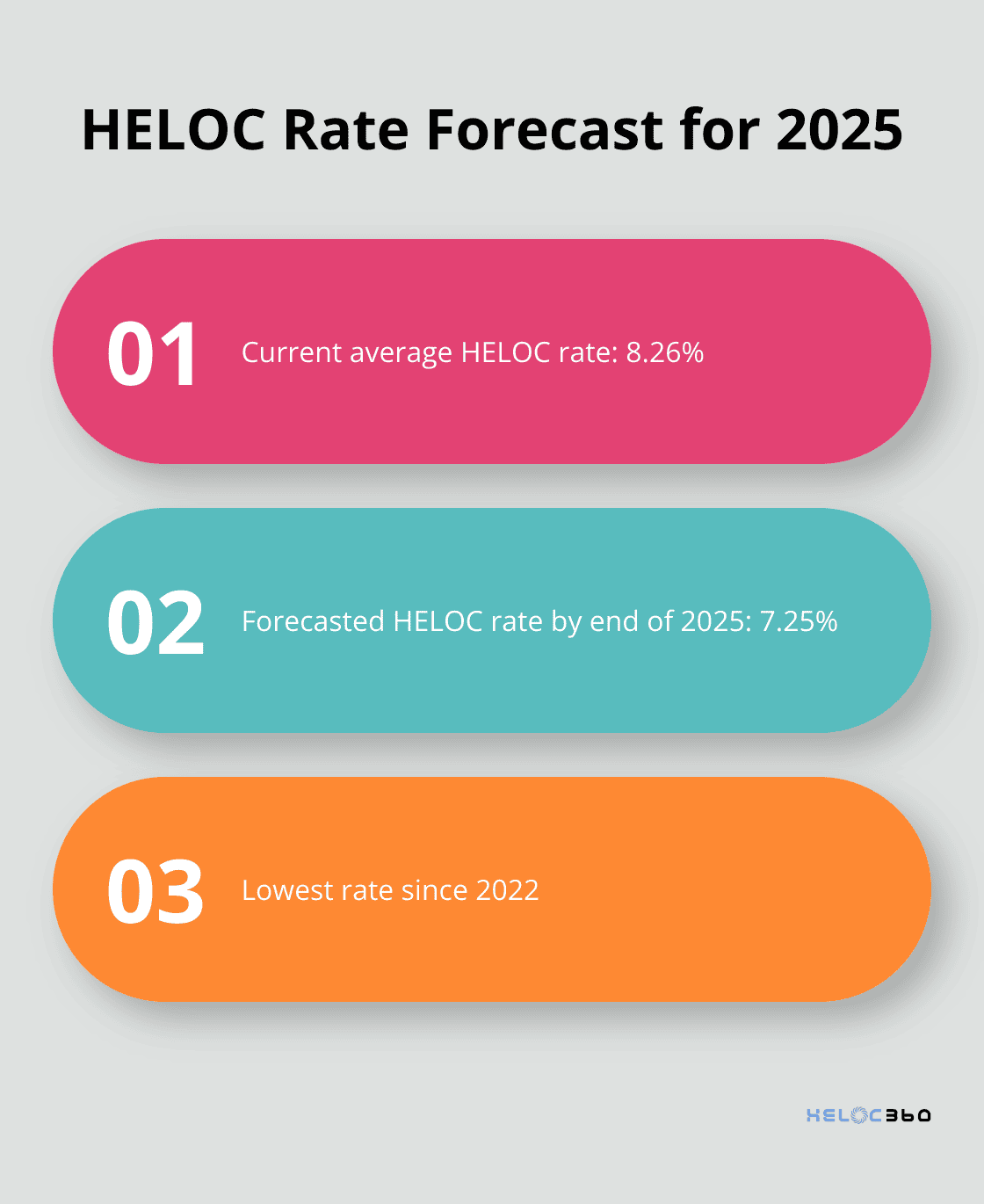

HELOCs typically come with variable interest rates, which can fluctuate based on market conditions. McBride forecasts that HELOC rates will continue to fall in 2025, sending the average HELOC to 7.25 percent by the end of the year, a low not seen since 2022. This illustrates how quickly borrowing costs can change, potentially impacting investment returns or ability to repay.

To mitigate this risk, you can set aside a portion of your HELOC funds as a buffer against rate increases. Some lenders offer rate caps or fixed-rate options for a portion of your HELOC balance, which can provide some stability in a volatile market.

The Risk of Overleveraging

Using a HELOC for investments can be tempting, but it's important to avoid overleveraging. The National Association of Realtors reported median home values for 3,110 counties and county-equivalents in January 2025. However, access to this equity doesn't mean you should use all of it.

Financial experts often recommend maintaining at least 20% equity in your home to protect against market downturns. You should create a comprehensive financial plan that accounts for potential market fluctuations and ensures you're not putting your home at unnecessary risk.

Effects on Credit Score and Future Borrowing

Opening a HELOC can affect your credit score in several ways. Applying for, opening and using a HELOC can help or hurt your credit scores depending on your overall credit profile and how you manage the account.

A HELOC is a secured debt, which means defaulting on payments could result in foreclosure. This severe consequence underscores the importance of having a solid repayment plan in place before borrowing against your home equity.

The Need for Disciplined Repayment

Successful wealth building with a HELOC requires strict financial discipline. You should create a detailed repayment plan before drawing on your HELOC, and stick to it religiously. Consider setting up automatic payments to ensure you never miss a due date.

If you're using your HELOC for investments, try to find opportunities that generate returns exceeding your borrowing costs. For example, if your HELOC rate is 7%, look for investment opportunities that consistently yield more than 7% annually to make the strategy worthwhile.

Final Thoughts

HELOC investing offers a unique opportunity for wealth building, but it requires careful consideration and strategic planning. When used responsibly, it can become a powerful tool to leverage your home's equity for financial growth. HELOCs provide flexibility and potentially lower interest rates compared to other borrowing options for real estate investments, home improvements, debt consolidation, and business expansion.

The risks of variable interest rates, potential overleveraging, and impacts on credit scores cannot be overlooked. Successful wealth building with a HELOC demands financial discipline, a solid repayment plan, and a thorough understanding of the associated risks. You must approach HELOC investing with caution and create a comprehensive strategy before proceeding.

At HELOC360, we understand the complexities of leveraging home equity for financial growth. Our platform helps homeowners navigate the HELOC landscape with confidence. We provide expert guidance, simplify the process, and connect you with lenders that align with your unique financial goals. For comprehensive solutions tailored to your needs, visit HELOC360 today.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.