Converting Your HELOC to a Fixed-Rate Loan

Table of Contents

Are you considering a HELOC conversion? Many homeowners find themselves in this position, weighing the benefits of switching from a variable-rate home equity line of credit to a fixed-rate loan.

At HELOC360, we understand the complexities of this decision and its potential impact on your financial future. This guide will walk you through the process, highlighting key factors to consider and helping you make an informed choice about your home equity.

Why Convert Your HELOC?

The Basics of HELOCs and Fixed-Rate Loans

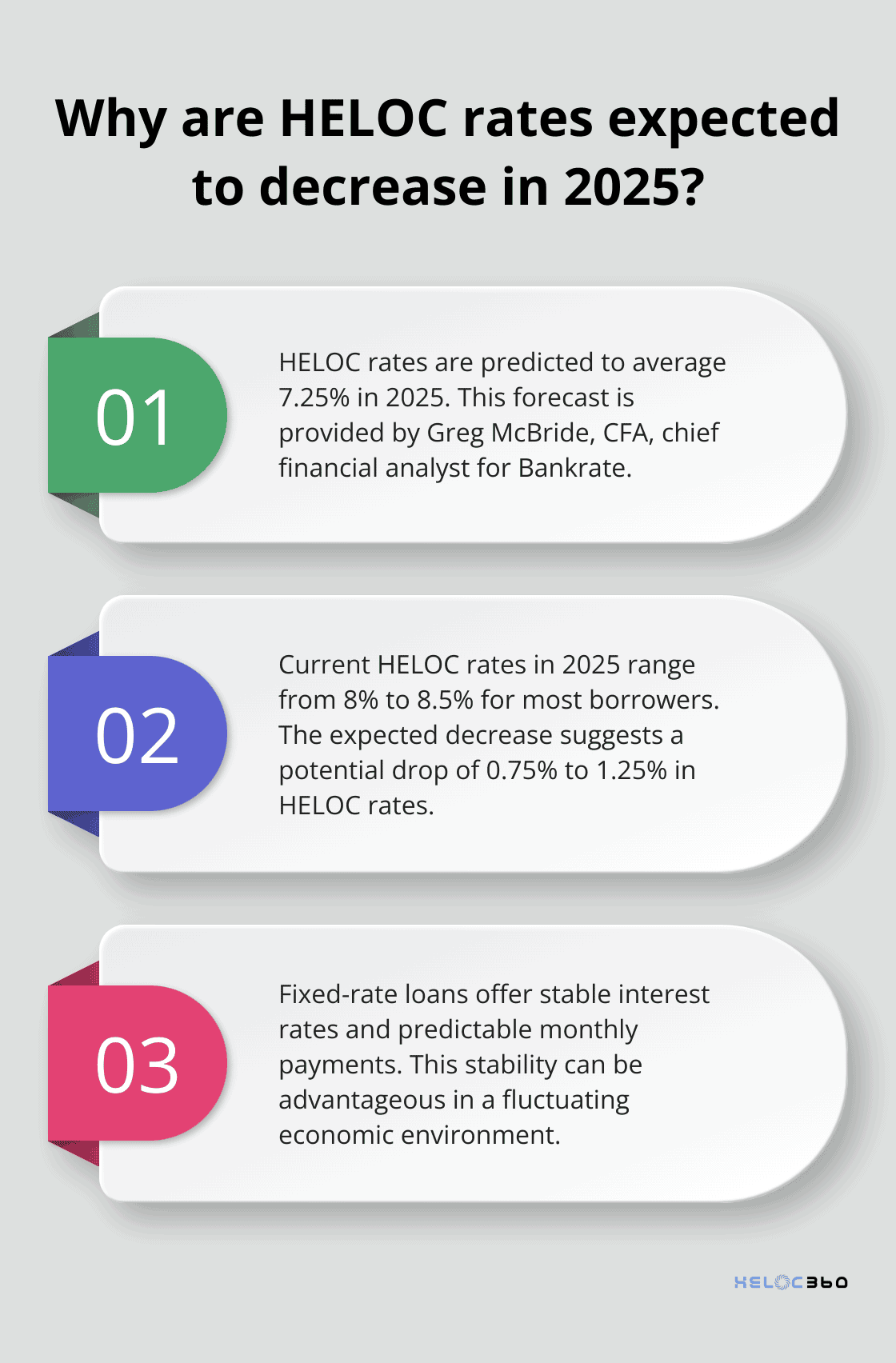

A Home Equity Line of Credit (HELOC) offers homeowners flexible access to funds based on their home's equity. HELOCs typically come with variable interest rates, which means your payments can fluctuate based on market conditions. This can benefit you when rates are low but also expose you to potential increases in your monthly payments if rates rise. The average HELOC rate in 2025 tends to hover around 8% to 8.5% for most borrowers. However, Greg McBride, CFA, chief financial analyst for Bankrate, predicts HELOC rates will average 7.25% in 2025.

Fixed-rate loans provide stability. Your interest rate remains constant throughout the loan term, offering predictable monthly payments. This appeals to many, especially in a rising rate environment or for those who prefer consistent budgeting.

Reasons to Consider Conversion

Converting your HELOC to a fixed-rate loan can attract homeowners for several reasons:

- Protection from future rate hikes: HELOCs have variable rates. In a rising-interest rate environment, that means you'll pay more monthly. This unpredictability could become tough to manage.

- Simplified financial planning: A fixed rate allows you to know exactly how much to budget for loan payments each month, eliminating the uncertainty of variable rates.

- Peace of mind: Fixed rates provide stability in an unpredictable economic climate.

Timing Your Conversion

The timing of your HELOC conversion plays a critical role in its success. Consider these factors:

- Draw period status: If you're still in the draw period and need to borrow more funds, you might want to wait. However, if you've borrowed the amount you need and worry about rising rates, now could be the right time to convert.

- Lender policies: Some lenders only allow fixed-rate conversions during the HELOC's draw period. Understanding your HELOC's terms and your lender's policies is essential.

- Market conditions: Keep an eye on economic indicators and interest rate trends. If rates are expected to rise significantly, converting sooner rather than later might be advantageous.

Evaluating Your Financial Situation

Before deciding to convert, take a close look at your financial situation:

- Current interest rate: Compare your current HELOC rate to available fixed rates. If the difference is minimal, the benefits of conversion might not outweigh the costs.

- Remaining loan term: Consider how long you plan to keep the loan. If you're close to paying it off, conversion might not be worth the effort.

- Future financial goals: Think about your long-term financial objectives. Will a fixed-rate loan align better with these goals?

As you weigh these factors, remember that every financial situation is unique. What works for one homeowner might not be the best choice for another. The next section will guide you through the conversion process, helping you understand the steps involved and what to expect.

How to Convert Your HELOC

Checking Your Eligibility

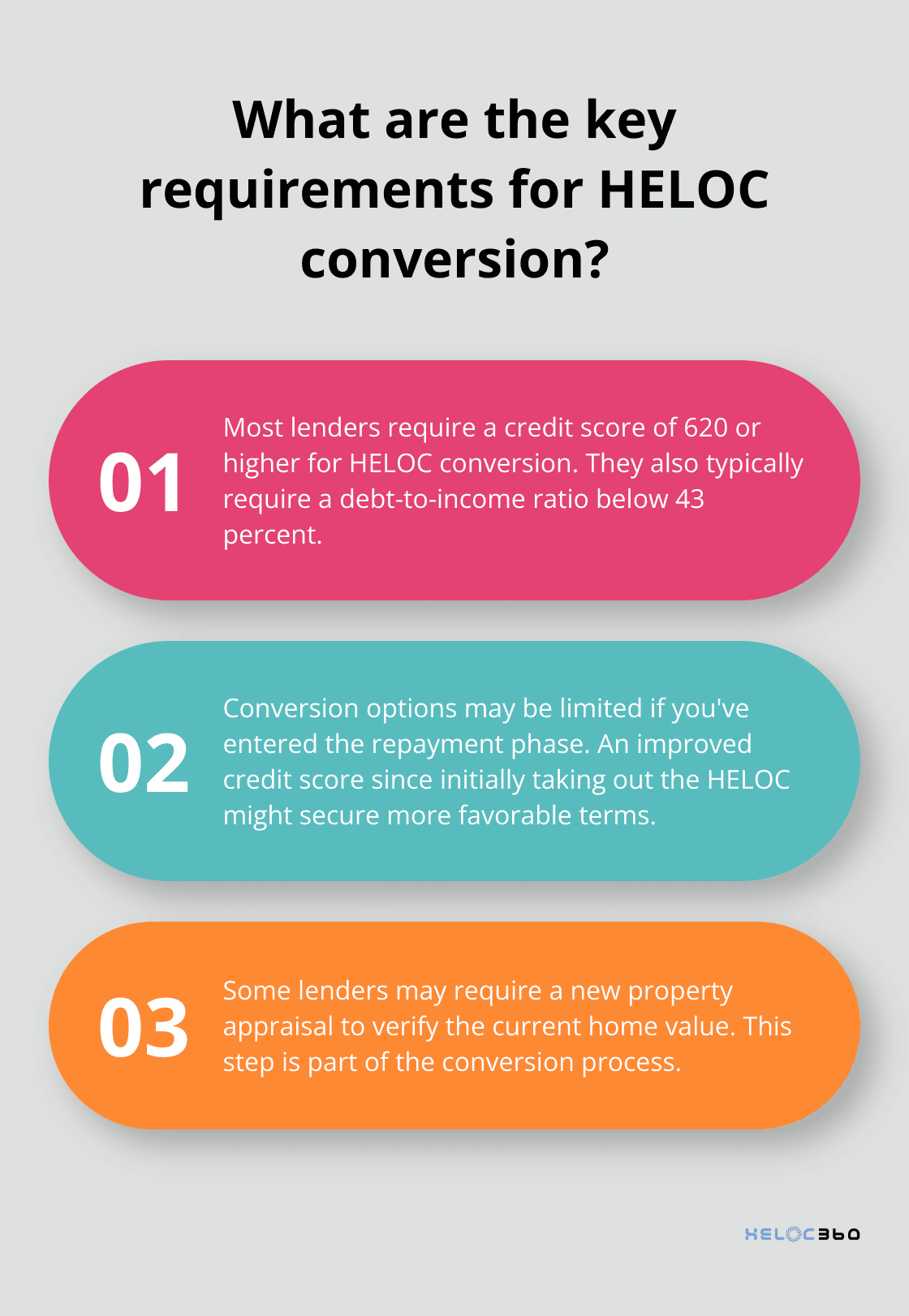

Before you start the conversion process, confirm your eligibility. Most lenders require a credit score of 620 or higher and a debt-to-income (DTI) ratio below 43 percent. Your options for conversion might be limited if you've entered the repayment phase. If your score has improved since you initially took out your HELOC, you might secure more favorable terms.

Steps in the Conversion Process

- Contact your current lender: Start by reaching out to your existing HELOC provider. They may offer fixed-rate conversion options that could save you time and money on fees.

- Review your current HELOC terms: Understand your existing interest rate, remaining balance, and any potential prepayment penalties.

- Get quotes from multiple lenders: Don't limit yourself to your current provider. Shop around for the best rates and terms. (HELOC360 can connect you with a network of lenders to compare offers easily.)

- Submit an application: Once you've chosen a lender, complete an application. Prepare recent financial documents, including pay stubs, tax returns, and bank statements.

- Property appraisal: Some lenders may require a new appraisal of your home to verify its current value.

- Closing: If approved, attend a closing to sign the new loan documents. This process finalizes the conversion of your variable-rate HELOC to a fixed-rate loan.

Timing Your Conversion Wisely

Timing can significantly impact the benefits of your HELOC conversion. According to Greg McBride, chief financial analyst at Bankrate, HELOC rates are expected to average 7.25% in 2025 (the lowest since 2022). This trend suggests that now might be an opportune time to lock in a fixed rate.

However, it's not just about current rates. Consider your personal financial timeline as well. If you plan to sell your home soon, the costs associated with conversion might outweigh the benefits. On the other hand, if you're settling in for the long haul and want to protect against potential rate increases, converting sooner could be advantageous.

Some lenders impose limits on the amounts that can be converted to fixed-rate loans. If you have a large HELOC balance, you might need to convert it in portions over time. This strategy allows you to take advantage of potentially lower rates in the future while still securing a fixed rate for a portion of your balance now.

As you weigh the pros and cons of converting your HELOC, it's important to understand the potential advantages and drawbacks. Let's explore these factors in more detail to help you make an informed decision.

Is Converting Your HELOC Worth It?

Stability in an Uncertain Market

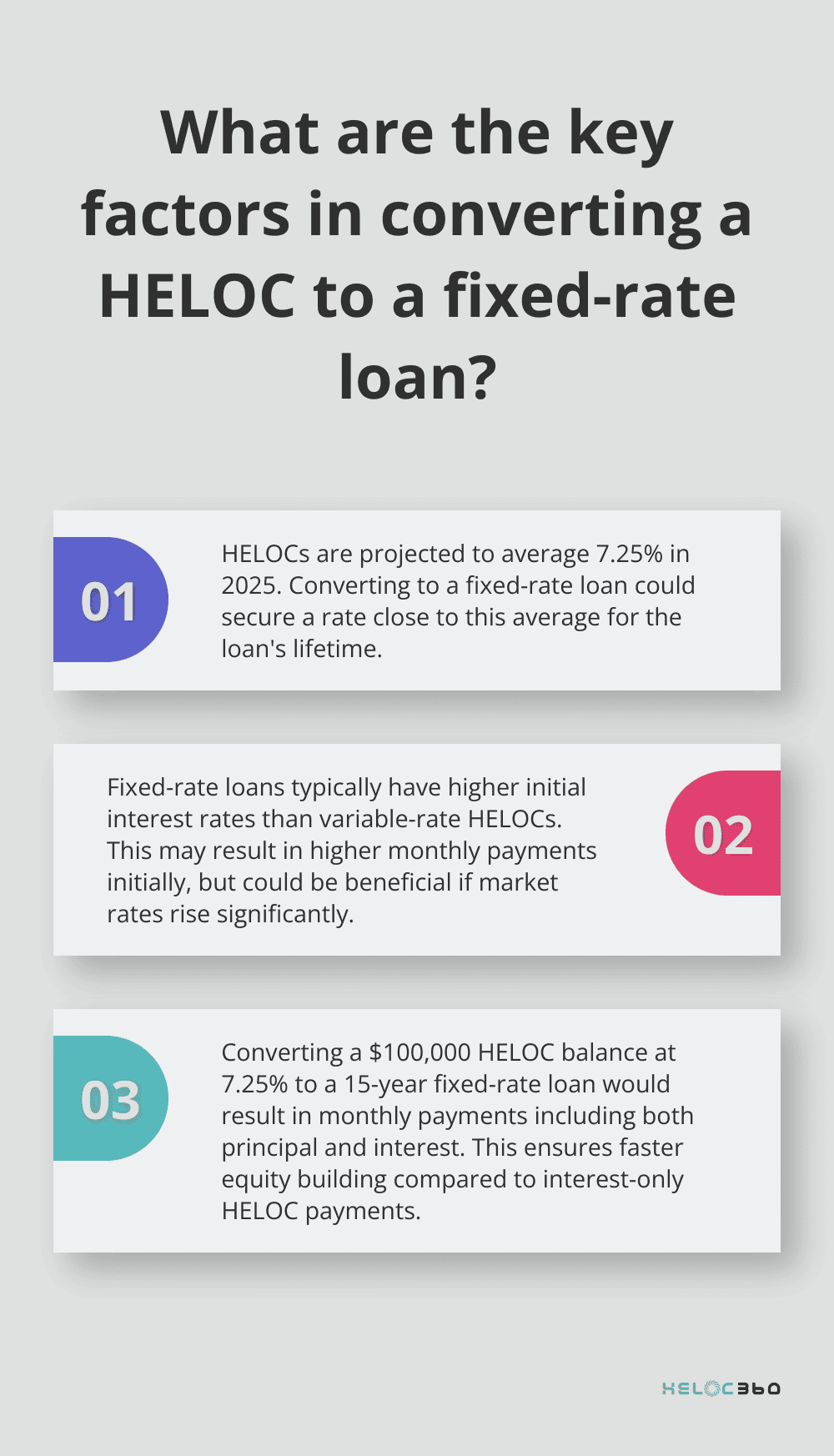

One of the primary advantages of switching to a fixed-rate loan is the predictability it offers. With interest rates expected to fluctuate, locking in a rate now could protect you from potential increases in the future. Greg McBride, chief financial analyst at Bankrate, projects HELOC rates to average 7.25% in 2025. A conversion could potentially secure a rate close to this average for the life of your loan.

The Cost of Certainty

While stability attracts many borrowers, it often comes with a price tag. Fixed-rate loans typically have higher initial interest rates compared to variable-rate HELOCs. This means you might start off with higher monthly payments than you currently make. However, if market rates rise significantly, your fixed rate could end up lower than what you'd pay with a variable rate HELOC in the long run.

Impact on Your Monthly Budget

Converting to a fixed-rate loan will likely change your monthly payments. In most cases, you'll start paying both principal and interest immediately, rather than just interest during the HELOC's draw period. This can result in higher monthly payments, but it also means you build equity faster.

For example, converting a $100,000 HELOC balance at 7.25% interest to a 15-year fixed-rate loan would result in monthly payments that include both principal and interest. This amount would exceed interest-only payments on a HELOC, but it ensures you pay down the principal from the start.

Long-Term Financial Planning

Your decision to convert should align with your long-term financial goals. If you plan to stay in your home for many years and want to avoid the uncertainty of variable rates, conversion could prove a smart move. However, if you consider selling your home in the near future, the costs associated with conversion might outweigh the benefits.

It's important to factor in any fees associated with conversion. Some lenders charge origination fees or closing costs (which can add up to several thousand dollars). Ask potential lenders about these fees and factor them into your decision-making process.

Comparing Your Options

To make an informed decision, compare offers from multiple lenders. Look at the interest rates, loan terms, and associated fees. Consider how each option fits into your overall financial picture. Some online platforms can help you compare offers side-by-side, making it easier to find a solution that fits your financial needs.

Final Thoughts

Converting your HELOC to a fixed-rate loan requires careful consideration of your financial situation and goals. The timing of your HELOC conversion plays a crucial role in its success, with rates expected to average 7.25% in 2025. Fixed-rate loans offer stability but often come with higher initial interest rates, which means you might start with higher monthly payments.

Your decision should align with your long-term financial plans and consider factors such as how long you plan to stay in your home. We at HELOC360 understand that navigating these decisions can be complex, which is why we're here to help. Our platform simplifies the process of exploring your home equity options, including HELOC conversions.

We provide expert guidance and connect you with lenders that fit your unique needs. Visit HELOC360 to learn more about how we can help you make the most of your home's value and achieve your financial goals. Your individual circumstances will ultimately determine whether a HELOC conversion is the right choice for you.

Related Articles

Funding College with a HELOC Is It the Right Choice?

Explore if using a HELOC for college tuition is wise. Learn the benefits, risks, and real-world examples in this insightful guide.

When's the Perfect Time to Apply for a HELOC?

Find the ideal HELOC timing. Explore key factors affecting when to apply for a HELOC and secure the best rates for your financial goals now.

What is a Home Equity Line of Credit Loan?

Discover what a home equity line of credit loan is and how it can improve your finances. Get tips for effective HELOC management.