Demystifying HELOC Eligibility Requirements

Table of Contents

Navigating HELOC eligibility can be confusing for many homeowners. At HELOC360, we often hear questions about credit scores, home equity, and income requirements.

This guide breaks down the key factors lenders consider when approving a Home Equity Line of Credit. We'll explore credit thresholds, loan-to-value ratios, and debt-to-income considerations to help you understand if you might qualify.

What Credit Score Do You Need for a HELOC?

Your credit score significantly influences your ability to secure a Home Equity Line of Credit (HELOC). Let's explore the specific credit requirements and their impact on your HELOC prospects.

Minimum Credit Score Thresholds

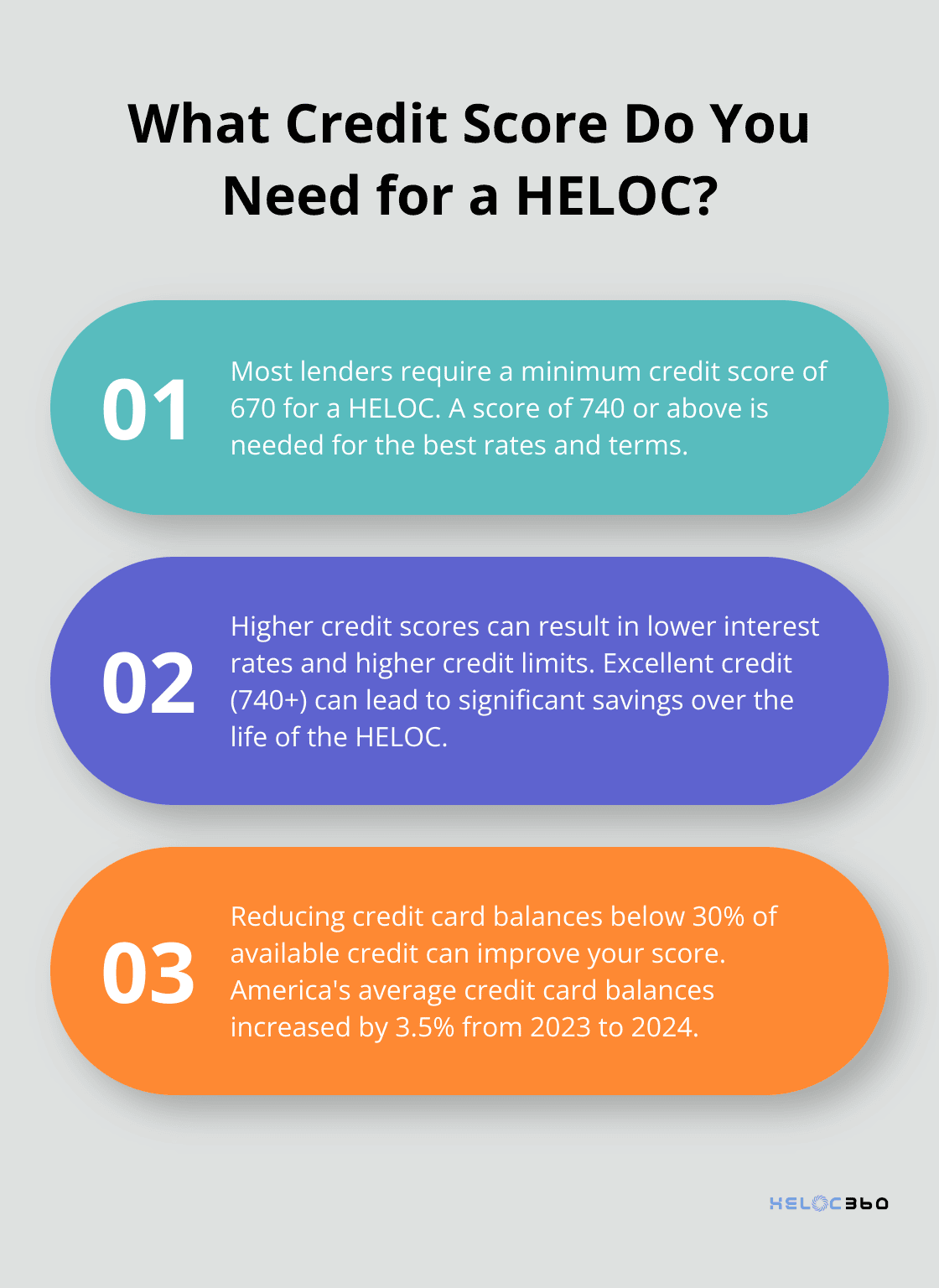

Most lenders require a minimum credit score of 670 to qualify for a HELOC. This serves as the baseline for many lenders. To obtain the best rates and terms, you should try to achieve a score of 740 or above.

Impact of Credit Scores on HELOC Terms

Your credit score doesn't just determine eligibility; it substantially affects the terms of your HELOC. A higher score can result in:

- Lower interest rates

- Higher credit limits

- More flexible repayment terms

Borrowers with excellent credit (scores of 740+) might secure better interest rates than those with lower credit scores. This difference can amount to thousands of dollars saved over the life of your HELOC.

Quick Wins to Improve Your Credit Score

If your credit score needs improvement before applying for a HELOC, consider these actionable steps:

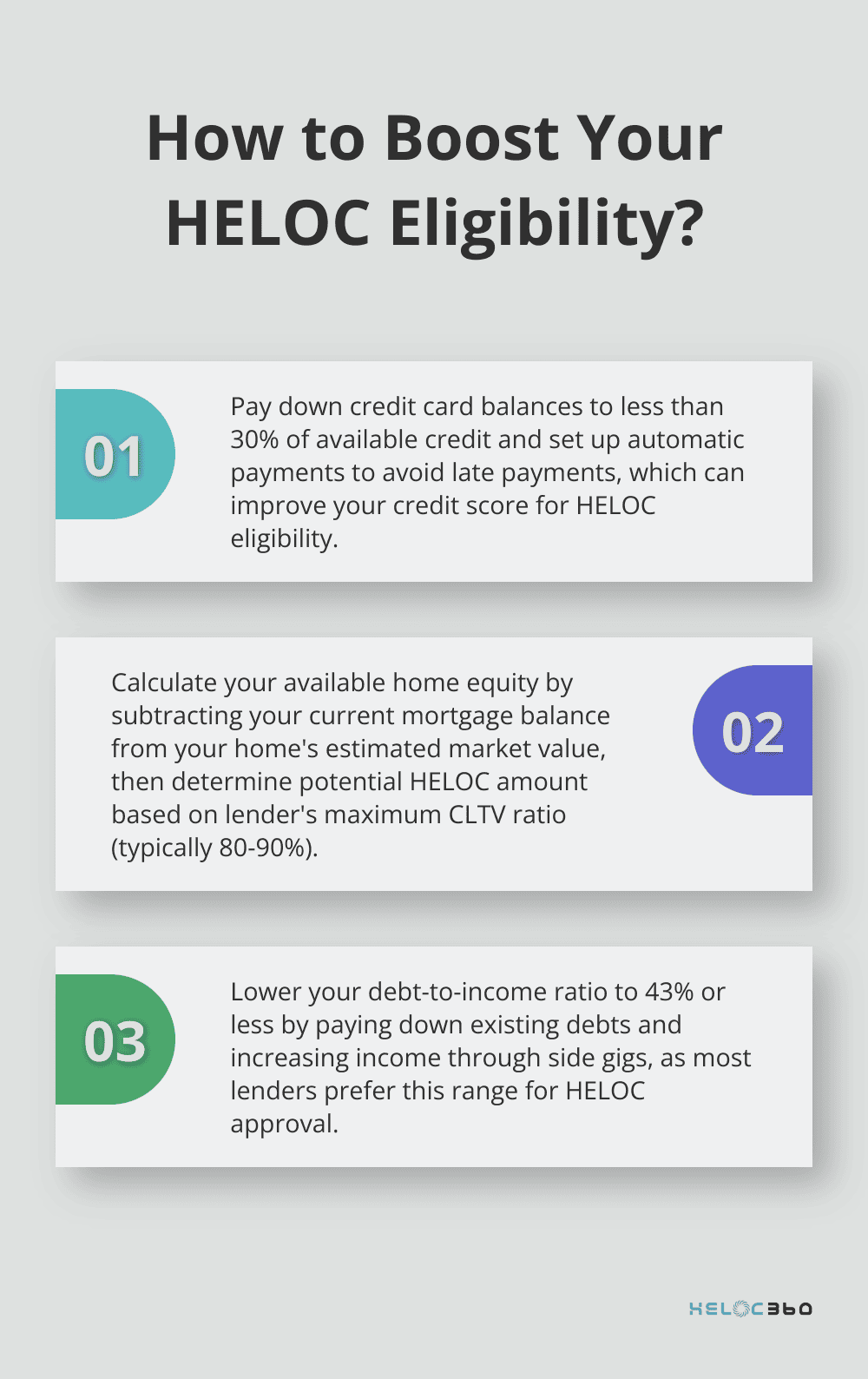

- Reduce credit card balances: Try to use less than 30% of your available credit.

- Implement automatic payments: Avoid late payments that can harm your score.

- Maintain old credit accounts: Credit history length matters.

- Minimize new credit applications: Each hard inquiry can temporarily lower your score.

An Experian analysis found that America's average credit card balances increased by 3.5% from 2023 to 2024. Reducing these balances could potentially improve your credit score.

The Role of Credit Monitoring

Regular credit monitoring can help you track your progress and identify areas for improvement. Many free and paid services offer credit score updates and personalized recommendations for boosting your score.

Beyond Credit Scores: Other Factors in HELOC Approval

While your credit score plays a vital role, it's not the only factor lenders consider. In the next section, we'll examine another crucial element: your home equity and loan-to-value ratio. These factors work together to paint a complete picture of your financial health and HELOC eligibility.

How Much Home Equity Do You Need for a HELOC?

Understanding Home Equity

Home equity represents the portion of your property that you truly own. You calculate it by subtracting your outstanding mortgage balance from your home's current market value. This equity plays a significant role in determining your eligibility for a Home Equity Line of Credit (HELOC).

Loan-to-Value Ratio Explained

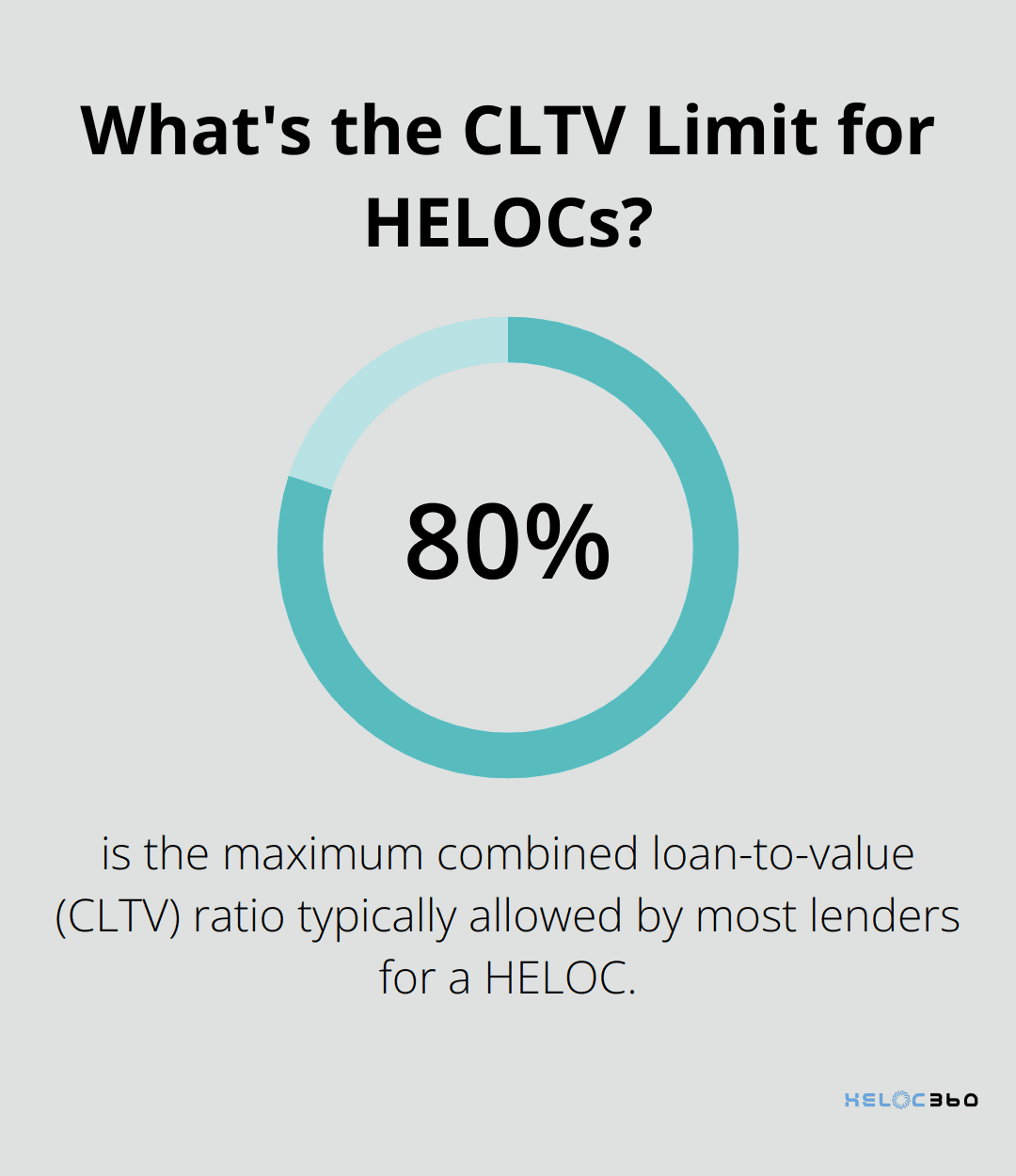

Lenders use the loan-to-value (LTV) ratio to assess HELOC eligibility. This ratio compares your loan amount to your home's appraised value. For HELOCs, lenders typically focus on the combined loan-to-value (CLTV) ratio, which is the ratio of all loans on a property to the property's value. Lenders use it to determine risk of default.

Most lenders require homeowners to maintain at least 20% equity in their homes after taking out a HELOC. This requirement translates to a maximum CLTV ratio of 80%. Some lenders may allow a CLTV up to 85% or 90%, but these higher ratios often come with stricter credit requirements and potentially higher interest rates.

How to Calculate Your Available Home Equity

To determine your available equity:

- Estimate your home's current market value (use online estimators or consult a real estate agent).

- Subtract your current mortgage balance from this value.

For example: Home value: $400,000 Mortgage balance: $250,000 Total equity: $150,000 ($400,000 - $250,000)

Assuming a maximum CLTV of 80%: Maximum total debt allowed: $320,000 ($400,000 x 80%) Potential HELOC amount: $70,000 ($320,000 - $250,000)

Home Value Fluctuations and Their Impact

Home values can change over time. The National Association of Realtors reported that the median existing single-family home price was $402,500 in February, up 3.7% from February 2024. This increase has allowed many homeowners to access more equity.

However, if home values decline, your LTV ratio could increase. This change might affect your ability to borrow or lead to a reduction in your credit line. Lenders remain cautious about allowing borrowers to tap into too much of their equity for this reason.

Strategies to Improve Your LTV Ratio

If your current LTV ratio doesn't meet HELOC approval standards, consider these options:

- Pay down your mortgage: Extra payments towards your principal will increase your equity.

- Wait for appreciation: In many markets, home values tend to increase over time, naturally improving your LTV ratio.

- Make home improvements: Strategic renovations can increase your home's value, potentially improving your LTV ratio.

Your income and debt-to-income ratio also play significant roles in HELOC eligibility. The next section will explore these factors to provide a complete picture of what lenders consider in the approval process.

Can You Afford a HELOC?

Income Stability Requirements

Lenders scrutinize your income stability when you apply for a Home Equity Line of Credit (HELOC). You must show evidence of consistent income demonstrating your ability to repay borrowed funds. Common documents required include:

- Current pay stubs and W-2 forms

- Tax returns for the last two years

- Proof of additional income sources (e.g., rental income, investments)

Self-employed individuals or those with variable incomes might need to provide more documentation, such as profit and loss statements or bank records.

Calculating Your Debt-to-Income Ratio

Your debt-to-income (DTI) ratio plays a critical role in HELOC approval. This percentage represents the portion of your monthly income that goes towards debt payments. To calculate your DTI:

- Add up all monthly debt payments (mortgage, car loans, credit cards, etc.)

- Divide this total by your gross monthly income

- Multiply by 100 to get the percentage

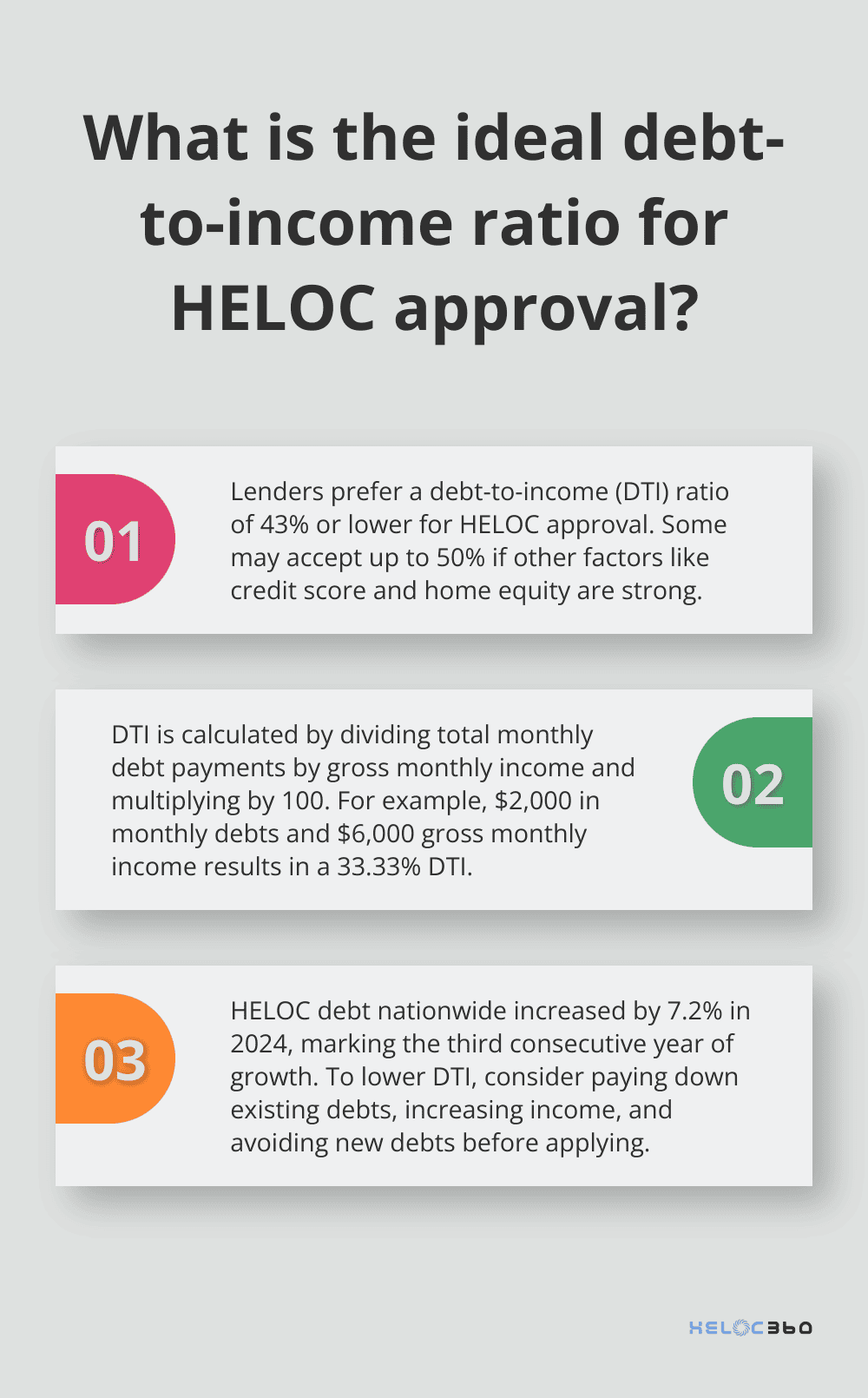

For example, if your monthly debts total $2,000 and your gross monthly income is $6,000, your DTI would be 33.33%.

Lender Preferences for DTI

Most lenders prefer a DTI of 43% or lower for HELOC approval. Some may accept up to 50% if other factors like credit score and home equity are strong.

HELOC debt nationwide increased by 7.2% in 2024, marking the third consecutive year that HELOC balances have grown after a decade of decline.

Strategies to Lower Your DTI

If your DTI exceeds the desired range, consider these steps:

- Pay down existing debts (especially high-interest credit cards)

- Increase your income through side gigs or asking for a raise

- Avoid new debts before applying for a HELOC

Improving your DTI not only increases your chances of HELOC approval but also enhances your overall financial health.

The Role of Credit Scores

While DTI is important, your credit score also significantly impacts HELOC approval. Typically, the higher your credit score is, the more likely you are to qualify for the best available interest rates and loan options.

Final Thoughts

HELOC eligibility requirements include credit scores, home equity, and income stability. A credit score of 670 or higher improves approval chances and secures better terms. Homeowners must maintain at least 20% equity and demonstrate a stable income with a debt-to-income ratio below 43%. These criteria unlock access to a flexible line of credit with potentially lower interest rates compared to other borrowing options.

HELOC eligibility offers numerous benefits for homeowners. It provides funds for home improvements, debt consolidation, or financial safety nets. Meeting these requirements positions borrowers as low-risk, potentially unlocking more favorable terms and higher credit limits. Homeowners who understand and meet these criteria can make informed decisions about using their home equity.

HELOC360 specializes in guiding homeowners through the HELOC application process. Our platform simplifies the journey, provides expert insights, and connects users with suitable lenders. We empower homeowners to make informed decisions about their home equity and achieve their financial goals. Homeowners should consider how a HELOC fits into their overall financial strategy before applying.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.