Discover Home Equity Line of Credit: A Comprehensive Guide

Table of Contents

Home equity lines of credit (HELOCs) offer homeowners a flexible way to tap into their property’s value. If you’re looking to discover home equity line of credit, it’s important to understand both their potential and the risks they carry, as these financial tools require careful consideration.

At HELOC360, we’ve created this guide to walk you through how HELOCs work, their benefits and drawbacks, and what you need to qualify for one.

What Is a HELOC?

Definition and Basic Concept

A Home Equity Line of Credit (HELOC) is a financial tool that allows homeowners to borrow against the equity they've built in their property. Unlike traditional loans, HELOCs provide a revolving line of credit (similar to a credit card), but with your home as collateral.

How HELOCs Work

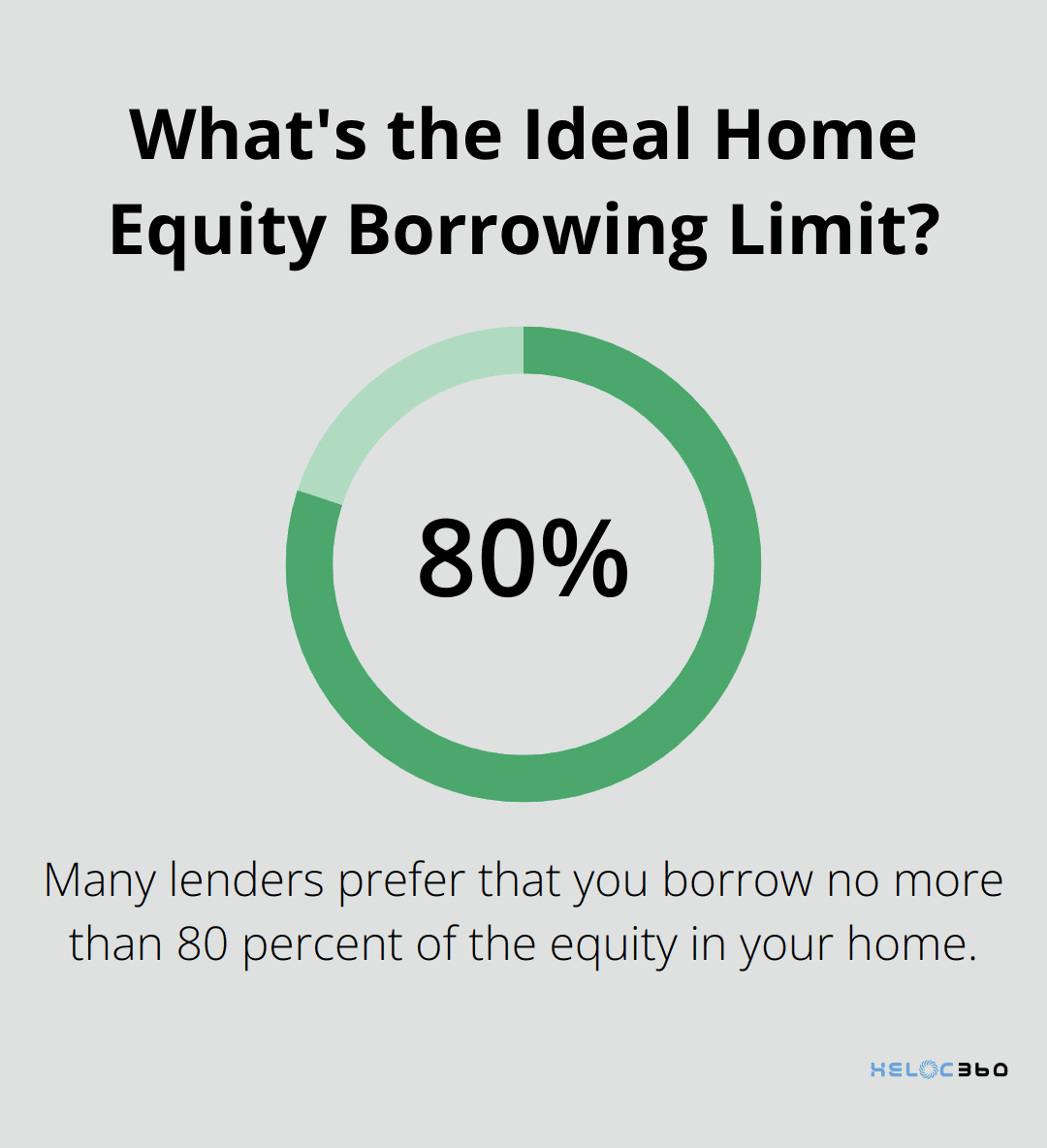

When you open a HELOC, you receive a credit limit based on your home's value and your existing mortgage balance. Many lenders prefer that you borrow no more than 80 percent of the equity in your home.

For example:

- Home value: $300,000

- Mortgage balance: $200,000

- Potential HELOC: $40,000 (80% of $300,000 = $240,000, minus $200,000)

Key Features of HELOCs

HELOCs typically have two phases:

- Draw Period: Lasts 5-10 years. You can borrow funds as needed and make interest-only payments.

- Repayment Period: You can no longer borrow and must repay both principal and interest.

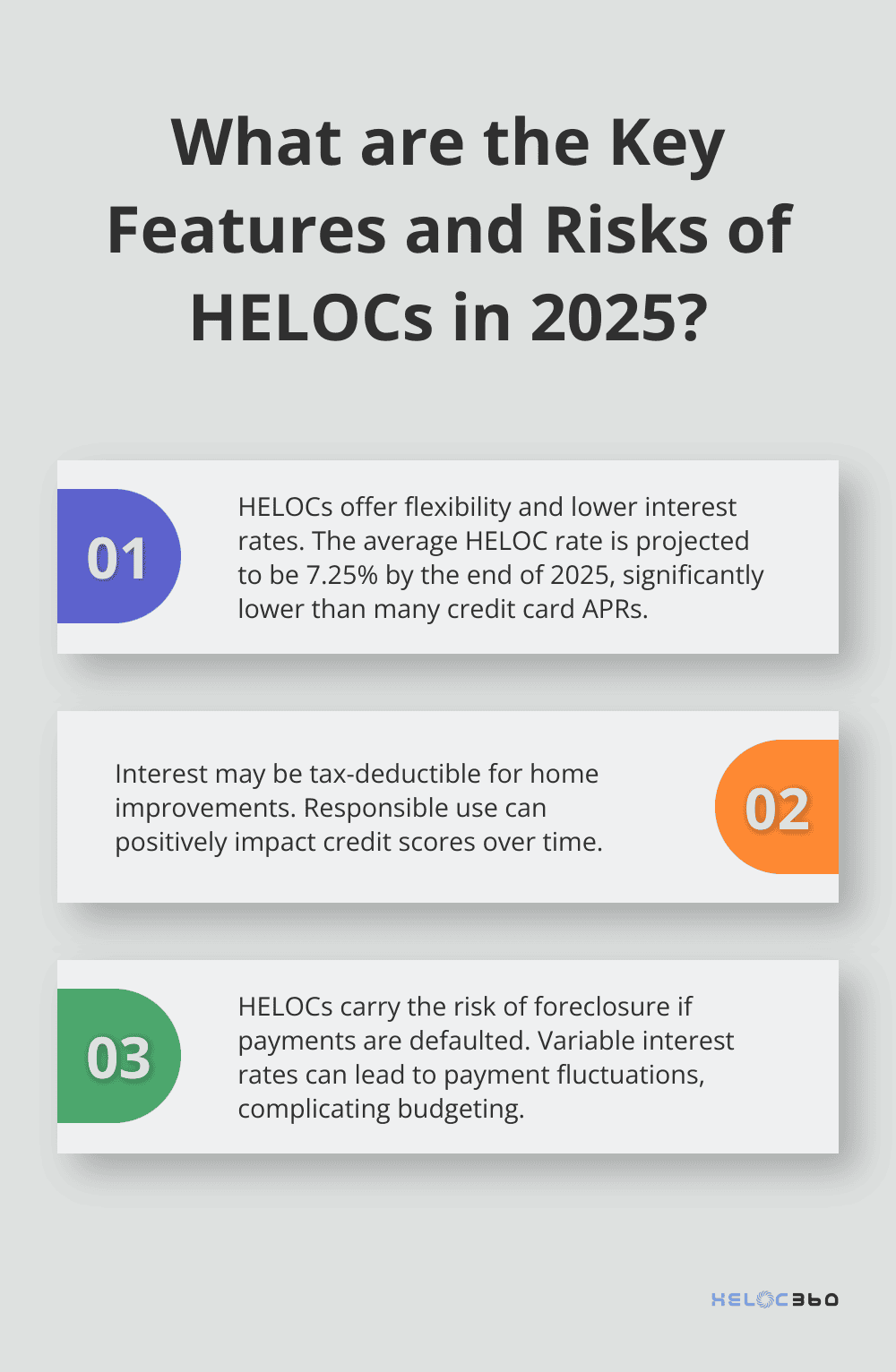

A unique aspect of HELOCs is their variable interest rates, often tied to the prime rate. This means your payments can fluctuate over time. Greg McBride, CFA, Bankrate's chief financial analyst, forecasts that the average HELOC rate will be 7.25 percent by the end of 2025, a low not seen since 2022.

HELOCs vs. Other Loans

HELOCs differ from traditional loans in several ways:

- Collateral: HELOCs use your home as collateral, resulting in lower interest rates compared to personal loans or credit cards. However, this puts your home at risk if you default on payments.

- Flexibility: Unlike home equity loans (which provide a lump sum upfront), HELOCs offer more flexibility. You only pay interest on the amount you actually borrow, not the entire credit line.

Considerations Before Choosing a HELOC

While HELOCs can be a powerful financial tool, they're not suitable for everyone. It's essential to evaluate your financial situation and goals before deciding on a HELOC. Factors to consider include:

- Your ability to repay the loan

- The stability of your income

- Your long-term financial plans

- The current real estate market conditions

To navigate these considerations and explore your options, platforms like HELOC360 can connect you with lenders that best suit your needs. These tools can help you make an informed decision about whether a HELOC aligns with your financial objectives.

Is a HELOC Right for You?

Flexibility and Lower Interest Rates

Home Equity Lines of Credit (HELOCs) offer unique advantages for homeowners. Their flexibility stands out as a primary benefit. You borrow only what you need, when you need it. This feature proves particularly useful for ongoing projects or unexpected expenses. HELOCs also typically offer lower interest rates compared to credit cards or personal loans. As of January 2025, the average HELOC rate is projected to hit 7.25% by the end of the year, which is significantly lower than many credit card APRs.

Tax Deductibility

HELOCs may provide tax benefits. If you use the funds for home improvements, you might deduct the interest from your taxes. However, you should consult with a tax professional to understand the specifics of your situation. The potential for tax deductions adds another layer of financial advantage to HELOCs.

Credit Score Impact

Responsible use of a HELOC can positively impact your credit score. Timely payments and maintaining a low credit utilization ratio demonstrate financial responsibility to credit bureaus. This responsible behavior can lead to improved credit scores over time.

Risks and Considerations

Despite their benefits, HELOCs come with risks. The most significant risk involves the potential for foreclosure if you default on payments, as your home serves as collateral. Additionally, the variable interest rates of HELOCs can lead to payment fluctuations, which complicates budgeting. In 2024, the Federal Reserve's rate hikes significantly impacted HELOC payments, with the monthly payment needed to withdraw $50,000 via a HELOC more than doubling. This trend underscores the importance of a solid repayment plan and understanding how rate changes could affect your finances.

Comparison with Other Financing Options

When evaluating HELOCs against other financing options, consider your specific needs. If you require a large lump sum for a one-time expense, a home equity loan might suit you better. However, if you're unsure of the total amount you'll need or prefer more flexibility, a HELOC could serve as the optimal choice.

As you weigh these factors, you might find value in platforms that provide expert guidance and connect you with suitable lenders (such as HELOC360). These resources can help ensure you make an informed choice that aligns with your financial goals. The decision to pursue a HELOC requires careful consideration of your financial situation, goals, and risk tolerance.

How to Get Approved for a HELOC

Eligibility Requirements

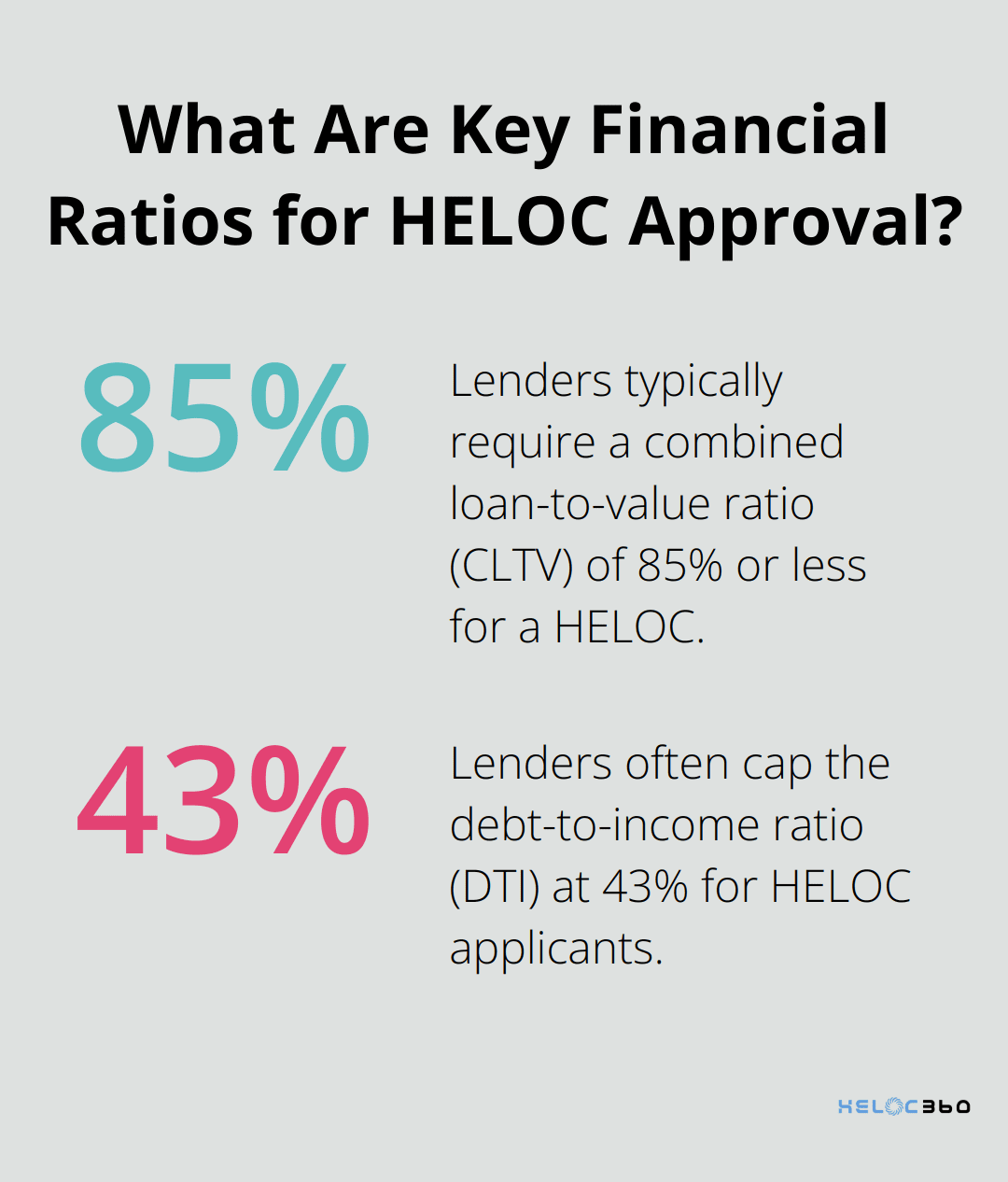

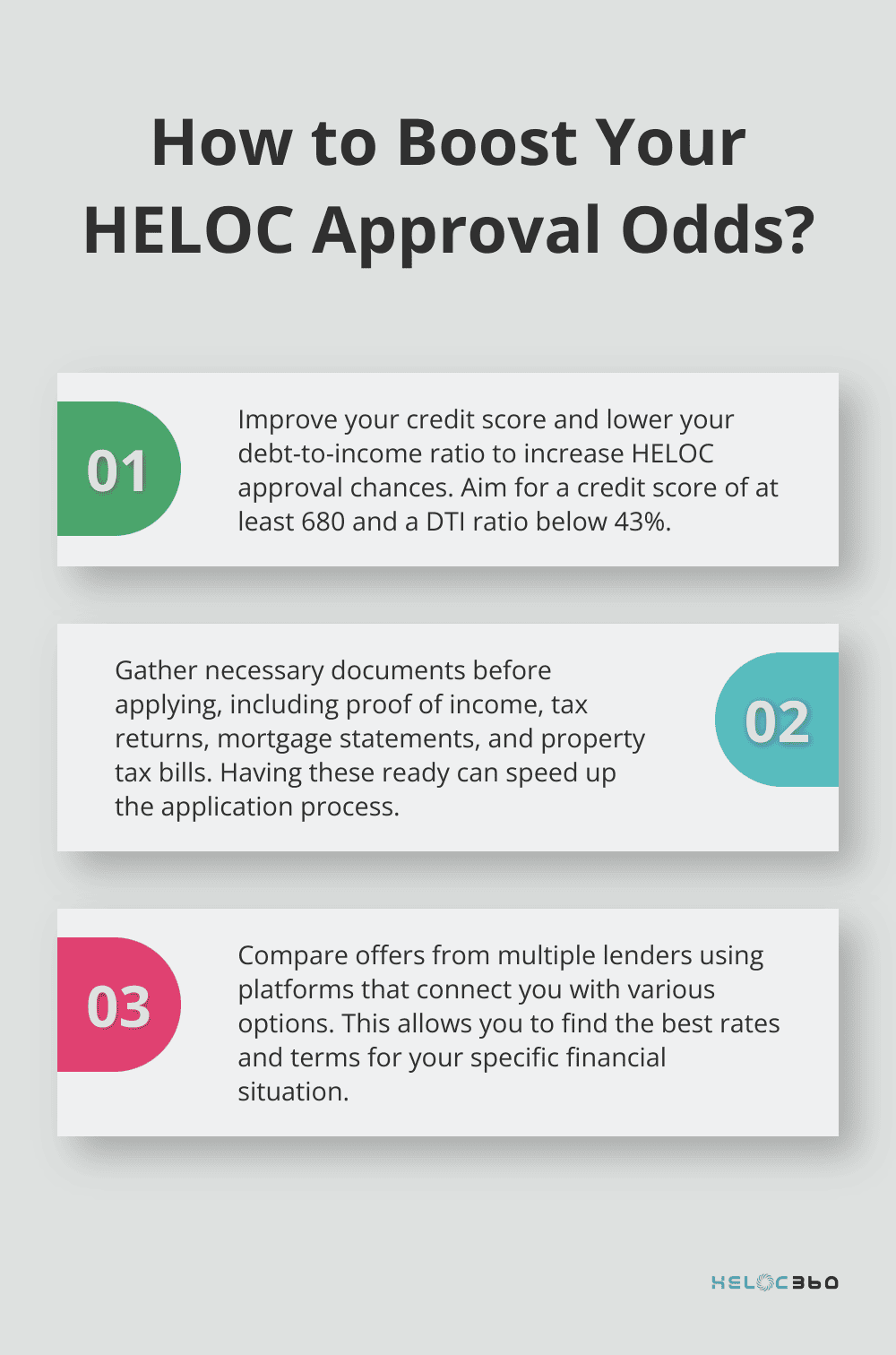

To qualify for a Home Equity Line of Credit (HELOC), you need to meet specific criteria. Most lenders require a credit score of at least 620, with many preferring scores of 680 or higher. The Federal Trade Commission states that lenders typically require a combined loan-to-value ratio (CLTV) of 85% or less. This means your existing mortgage balance plus the desired HELOC amount should not exceed 85% of your home's current market value.

Your debt-to-income ratio (DTI) also plays a significant role. Lenders often cap this at 43%, meaning your monthly debt payments (including your potential HELOC) should not exceed 43% of your gross monthly income. Some lenders may have stricter requirements, so you should try to achieve a lower DTI if possible.

Application Process

The HELOC application process involves several steps. First, you need to gather the necessary documentation, including:

- Proof of income

- Tax returns

- Information about your existing mortgage

- Details about your property value

Many lenders now offer online applications, which streamline the initial submission process.

After you submit your application, the lender will review your credit history and may order a professional appraisal of your home. This step determines your home's current market value, which directly impacts how much you can borrow.

If the lender approves your application, you'll receive a disclosure of terms. This includes the interest rate, fees, and repayment structure. Take time to review these carefully before accepting the offer.

Improving Your Approval Chances

To increase your chances of approval, consider taking steps to improve your credit score in the months leading up to your application. Paying down existing debts can help lower your DTI ratio, making you a more attractive borrower.

It's also beneficial to compare offers from multiple lenders. Each lender has its own criteria and terms, and rates can vary significantly. Platforms that connect you with multiple lenders can simplify this process, allowing you to compare offers easily and find the best fit for your financial situation.

Documentation Checklist

When applying for a HELOC, you'll typically need to provide the following documents:

- Proof of income (pay stubs, W-2 forms)

- Tax returns (usually for the past two years)

- Bank statements

- Mortgage statements

- Property tax bills

- Homeowners insurance information

Having these documents ready can speed up the application process and demonstrate your financial preparedness to lenders. For self-employed homeowners, there are flexible options available that use bank deposits to qualify instead of traditional tax returns.

Final Thoughts

Home Equity Lines of Credit (HELOCs) empower homeowners to access their property's value. HELOCs offer flexibility, potentially lower interest rates, and tax benefits for home improvements. However, they also involve risks such as variable interest rates and foreclosure potential if payments are missed.

Homeowners must evaluate their financial situation, long-term goals, and risk tolerance before they discover home equity line of credit options. Credit score, debt-to-income ratio, and current home value play significant roles in HELOC eligibility. Responsible management and a solid repayment plan are essential for successful HELOC utilization.

The HELOC landscape can be complex, but HELOC360 simplifies the process. Our platform connects you with lenders that match your unique needs. We provide expert guidance and tailored solutions to help you make informed decisions about leveraging your home equity.

Related Articles

Funding College with a HELOC Is It the Right Choice?

Explore if using a HELOC for college tuition is wise. Learn the benefits, risks, and real-world examples in this insightful guide.

When's the Perfect Time to Apply for a HELOC?

Find the ideal HELOC timing. Explore key factors affecting when to apply for a HELOC and secure the best rates for your financial goals now.

What is a Home Equity Line of Credit Loan?

Discover what a home equity line of credit loan is and how it can improve your finances. Get tips for effective HELOC management.