Are you looking to leverage your investment property’s equity? A HELOC for investment property could be the financial tool you need.

At HELOC360, we’ve seen many investors use HELOCs to fund property improvements, expand their portfolios, or cover unexpected expenses.

This guide will walk you through the ins and outs of using a HELOC on your investment property in 2025.

What Is a HELOC for Investment Property?

Understanding HELOCs for Investment Properties

A Home Equity Line of Credit (HELOC) for investment property is a financial tool that allows real estate investors to access the equity they’ve built in their rental or income-generating properties. This strategy has gained popularity among investors who want to fund property improvements, expand their portfolios, or cover unexpected expenses.

How HELOCs Work for Investment Properties

When you open a HELOC on your investment property, you set up a revolving line of credit secured by the equity in that property. Unlike traditional loans that provide a lump sum, a HELOC allows you to draw funds as needed during the draw period (typically 5 to 10 years). You pay interest only on the amount you borrow, which provides flexibility for investors with varying cash flow needs.

Key Differences from Primary Residence HELOCs

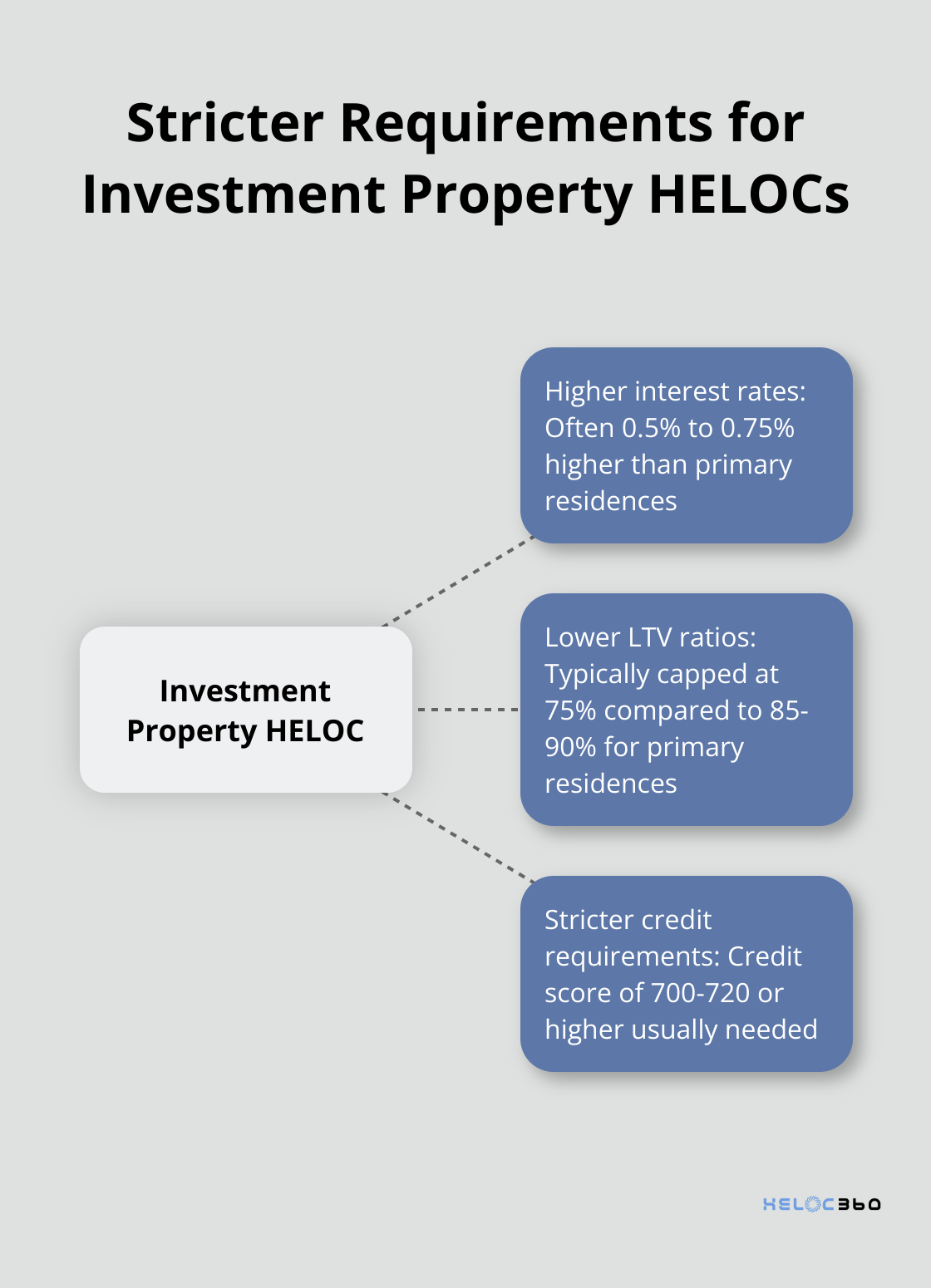

HELOCs for investment properties come with stricter requirements compared to those for primary residences. Lenders consider investment properties higher risk, which results in:

- Higher interest rates: Rates are often 0.5% to 0.75% higher than those for primary residences.

- Lower loan-to-value (LTV) ratios: While primary residences might allow up to 85% or 90% LTV, investment properties are often capped at 75%.

- Stricter credit requirements: A credit score of 700-720 or higher is typically needed (compared to 650-680 for primary residences).

Eligibility Requirements for Investment Property HELOCs

To qualify for a HELOC on your investment property in 2025, you must meet several criteria:

- Equity: Most lenders require at least 20-25% equity in the property after the HELOC.

- Debt-to-Income (DTI) Ratio: Try to maintain a DTI of 43% to 50% or lower (including the potential HELOC payment).

- Cash Reserves: Have at least six months of mortgage payments in reserve.

- Rental Income: Provide proof of consistent rental income (typically through tax returns or lease agreements).

- Property Type: Single-family homes and small multi-unit properties (2-4 units) are more likely to qualify than larger complexes.

These requirements can vary by lender, so it’s important to shop around. The next section will explore the benefits of using a HELOC on your investment property, helping you decide if this financial tool aligns with your investment strategy.

Why Use a HELOC for Your Investment Property?

Flexibility for Property Improvements

A Home Equity Line of Credit (HELOC) on your investment property offers unparalleled flexibility for property enhancements. Unlike traditional loans, you can withdraw funds as needed, which makes it ideal for ongoing renovation projects. You could use your HELOC to upgrade kitchens and bathrooms (which typically yield the highest return on investment). The National Association of Realtors reports on the impact of remodeling projects, including why homeowners choose to remodel and the increased happiness in the home once a project is completed.

Lower Interest Rates and Tax Benefits

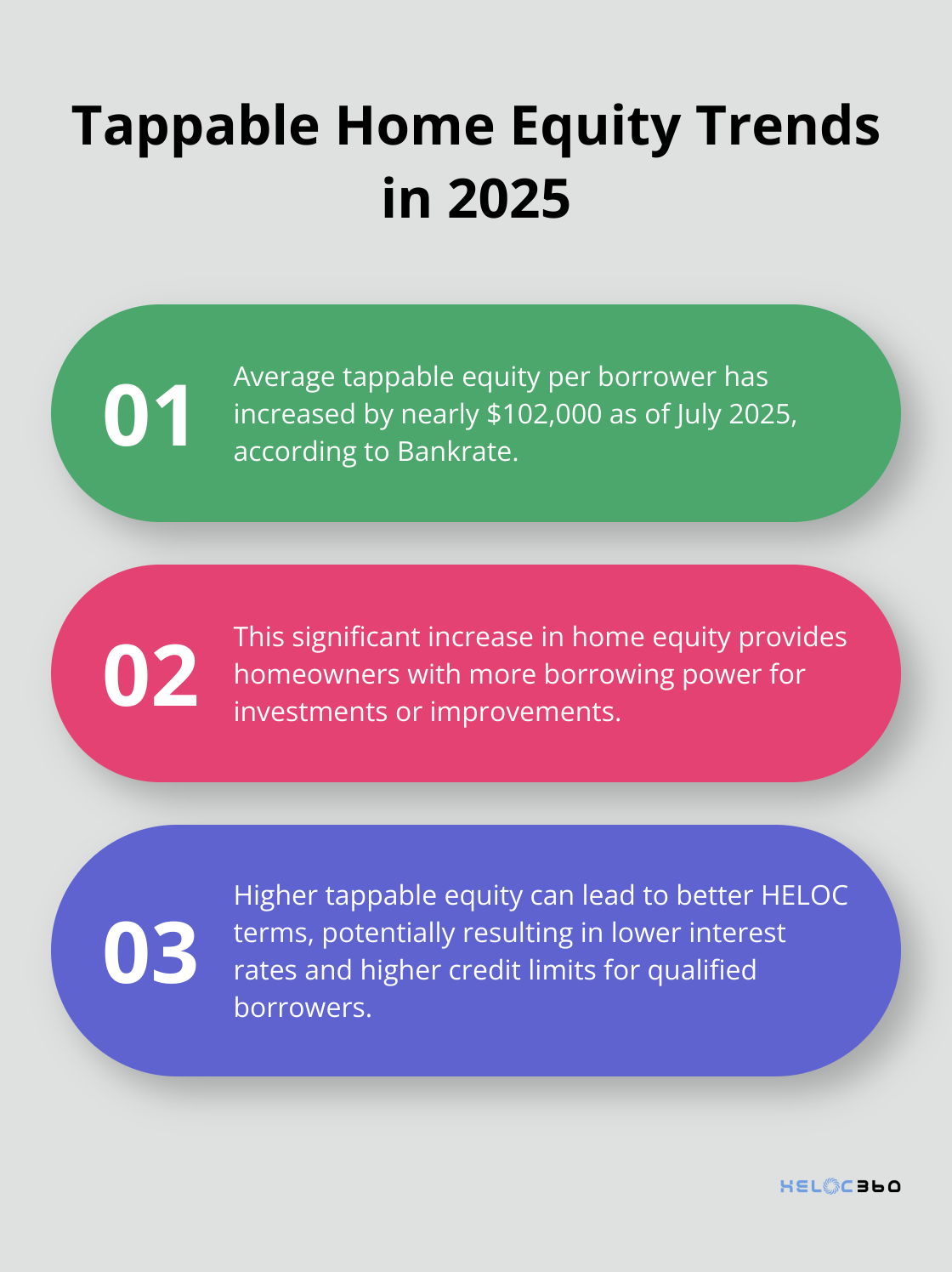

HELOCs often come with lower interest rates compared to other financing options like personal loans or credit cards. According to Bankrate, the average tappable equity per borrower has increased by nearly $102,000 as of July 2025. This difference can result in significant savings over time, especially for larger projects or purchases.

Moreover, the interest you pay on a HELOC used for property improvements may qualify for tax deductions. As of 2025, the IRS allows deductions for interest paid on home equity loans or lines of credit used to buy, build, or substantially improve the property that secures the loan. Always consult with a tax professional to understand the current regulations and how they apply to your situation.

Expanding Your Real Estate Portfolio

A HELOC can serve as a powerful tool for growing your real estate investments. You can access funds for down payments on additional properties by tapping into your existing property’s equity. This strategy, often called the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat), allows investors to scale their portfolios without tying up large amounts of cash in each property.

Some investors have successfully used this method to double or even triple their property holdings within a few years. However, you should approach this strategy with caution and a solid understanding of the real estate market in your target areas.

Competitive Edge in the Market

Using a HELOC can give you a competitive edge in the real estate market. With readily available funds, you can act quickly when investment opportunities arise. This advantage becomes particularly valuable in hot markets where properties sell fast. You can make cash offers or close deals more quickly, which often appeals to sellers and can lead to better purchase terms.

Emergency Fund for Unexpected Expenses

Investment properties can come with unexpected expenses, from emergency repairs to sudden vacancies. A HELOC can serve as a financial safety net, providing peace of mind and helping you maintain your property’s value and income potential. This buffer can prove invaluable in protecting your investment and ensuring its long-term profitability.

While a HELOC offers significant benefits, it also comes with potential risks. In the next section, we’ll explore key considerations to keep in mind before leveraging your investment property with a HELOC.

Key Considerations Before Getting a HELOC on Your Investment Property

Impact on Your Financial Health

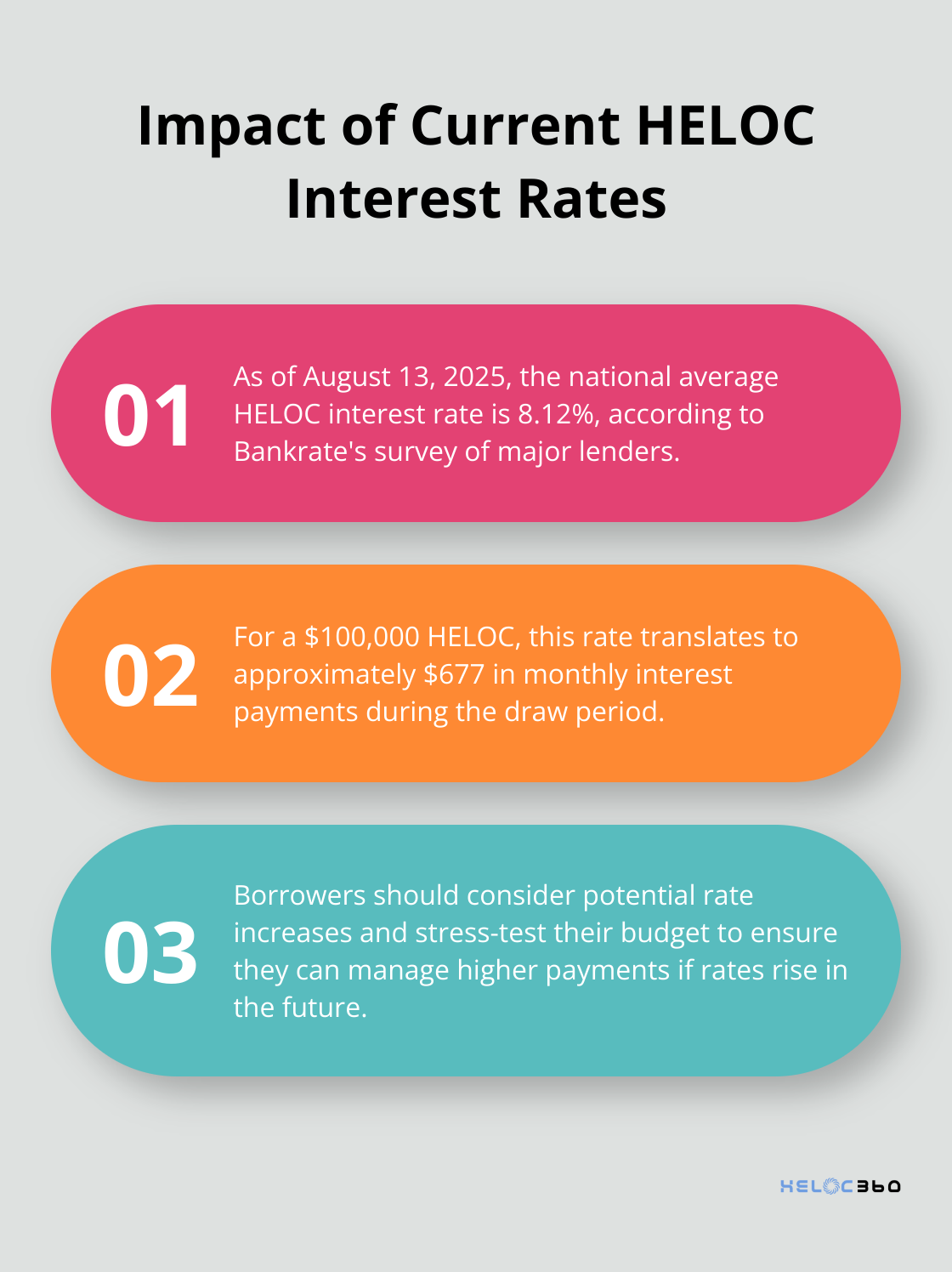

A Home Equity Line of Credit (HELOC) can significantly affect your cash flow and debt-to-income (DTI) ratio. You’ll pay interest only on the borrowed amount during the draw period, but these payments can still impact your monthly budget. The national average HELOC interest rate is 8.12% as of August 13, 2025, according to Bankrate’s latest survey of the nation’s largest home equity lenders. For a $100,000 HELOC, this translates to $677 in monthly interest payments alone.

Your DTI ratio will increase, potentially affecting your ability to secure future loans. Lenders typically prefer a DTI ratio below 43%. To calculate your new DTI, add your potential HELOC payment to your existing monthly debts and divide by your monthly income.

Collateral Risk Assessment

Using your investment property as collateral means you could lose the property if you default on the HELOC. This risk becomes particularly significant if you use the HELOC for purposes unrelated to the property itself. According to a recent report, 21,782 U.S. properties started the foreclosure process in June 2025, down 10 percent from the previous month but up 17 percent from June 2024.

Market Volatility Navigation

Real estate markets can be unpredictable. The past five years have seen both dramatic increases and sudden drops in property values. The S&P CoreLogic Case-Shiller National Home Price Index was at 331.10700 as of May 2025. However, local markets can vary widely.

A decline in property values could result in owing more than your property is worth. This situation (known as being “underwater” on your loan) can limit your financial options and make it difficult to sell or refinance the property.

Interest Rate Change Planning

HELOCs typically have variable interest rates, which means your payments can fluctuate. The Federal Reserve’s actions directly impact these rates. In 2024, three rate hikes occurred, each increasing HELOC rates by about 0.25%. It’s essential to factor in potential rate increases when budgeting for your HELOC payments.

Try to stress-test your budget. Calculate what your payments would be if rates increased by 1%, 2%, or even 3%. This exercise can help you determine if you’re comfortable with the potential financial impact.

Alternative Financing Options

Before you commit to a HELOC, explore other financing options. Cash-out refinancing or a fixed-rate home equity loan might be more suitable depending on your needs. Each option has its pros and cons, and the best choice depends on your specific financial situation and goals.

Final Thoughts

HELOCs for investment properties offer a powerful financial tool for real estate investors. The flexibility to access funds, potentially lower interest rates, and possible tax benefits make HELOCs attractive for property improvements and portfolio expansion. However, investors must weigh the impact on cash flow, collateral risks, and market fluctuations before deciding to use a HELOC on their investment property.

Thorough financial planning is essential before pursuing a HELOC for your investment property. Assess your current financial situation, future income projections, and risk tolerance. Consider how changes in interest rates or property values might affect your ability to repay the HELOC.

HELOC360 offers comprehensive support for investors seeking guidance on HELOCs for investment properties. Our platform helps you understand your options, connect with suitable lenders, and make informed decisions about leveraging your investment property’s equity. We strive to empower you in achieving your real estate investment objectives through expert insights and streamlined processes.

Our advise is based on experience in the mortgage industry and we are dedicated to helping you achieve your goal of owning a home. We may receive compensation from partner banks when you view mortgage rates listed on our website.