HELOC vs Home Equity Loan Which Fits Your Needs?

Table of Contents

Choosing between a HELOC and a home equity loan can be a pivotal decision for homeowners looking to tap into their property's value. These two financial tools offer distinct advantages and drawbacks, making a HELOC comparison essential for informed decision-making.

At HELOC360, we understand the importance of selecting the right option for your unique financial situation. This guide will break down the key features of HELOCs and home equity loans, helping you determine which one aligns best with your needs and goals.

What Is a HELOC?

Definition and Key Features

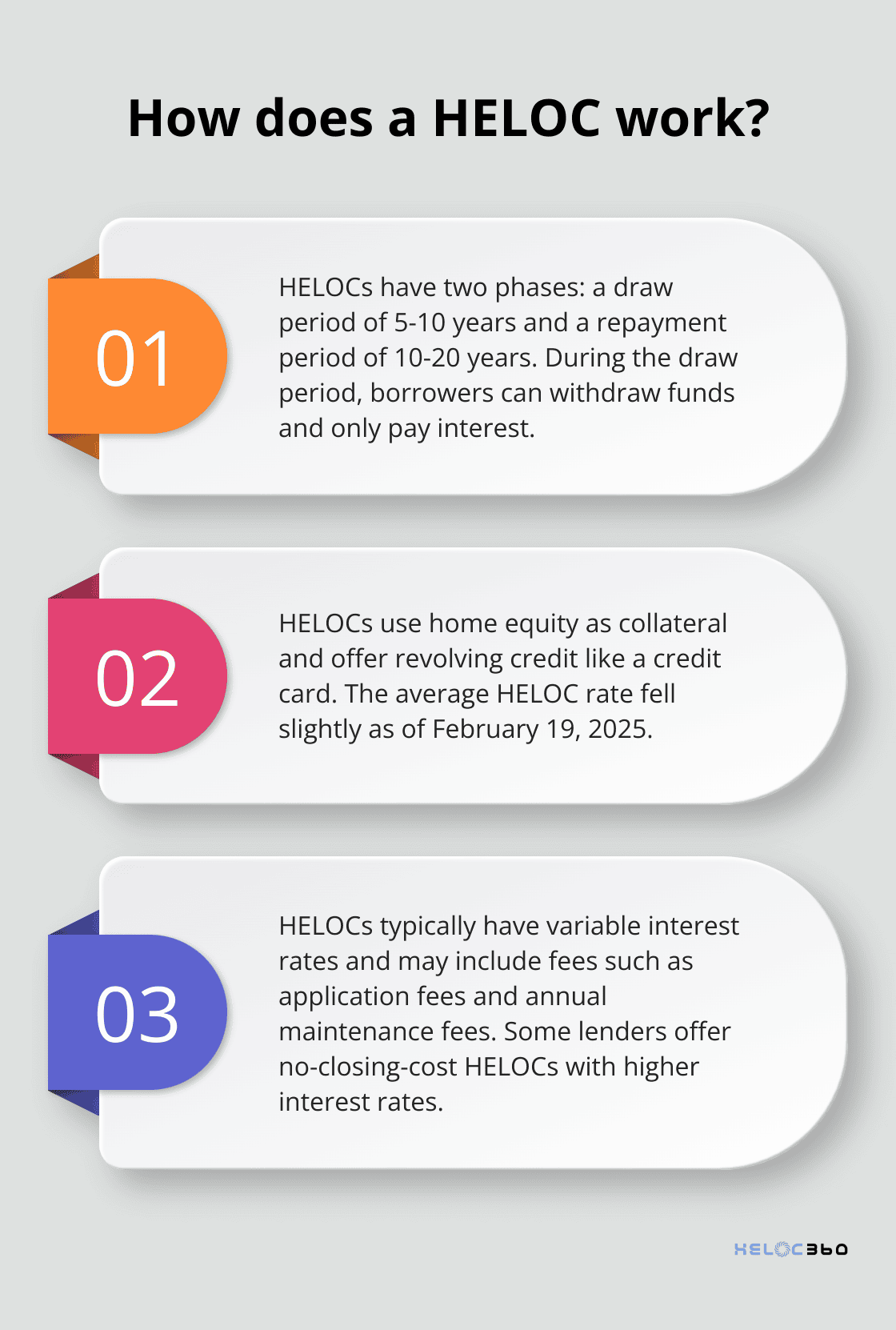

A Home Equity Line of Credit (HELOC) offers homeowners a way to access cash based on their equity. This financial tool provides a revolving credit line, similar to a credit card, but uses your home as collateral. HELOCs stand out for their adaptability, allowing borrowers to access funds as needed within a predetermined limit.

The Two-Phase Structure

HELOCs operate in two distinct phases:

- Draw Period: This initial phase (typically 5 to 10 years) allows borrowers to withdraw funds up to their credit limit. During this time, you only pay interest on the amount borrowed, not the entire credit line.

- Repayment Period: Following the draw period, borrowers enter the repayment phase (often 10 to 20 years). At this point, you can no longer borrow from the credit line and must repay both principal and interest.

This structure makes HELOCs particularly suitable for ongoing expenses or projects with uncertain costs.

Interest Rates and Associated Fees

HELOCs typically come with variable interest rates, which can cause payment fluctuations over time. As of February 19, 2025, the average HELOC rate fell slightly. However, rates can vary significantly between lenders, so it's important to compare options.

When considering a HELOC, be aware of potential fees, which may include:

- Application fees

- Annual maintenance fees

- Closing costs

Some lenders offer no-closing-cost HELOCs, but these often feature higher interest rates to offset the waived fees.

Practical Tips for HELOC Usage

To optimize your HELOC experience:

- Use funds for value-adding home improvements (renovations that increase your home's value can be a smart investment).

- Create a solid repayment strategy (plan how you'll manage payments, especially when the repayment period begins).

- Stay informed about interest rate trends (this helps you anticipate changes in your payments).

- Look for rate caps (some HELOCs offer these to protect against dramatic interest rate increases).

Navigating HELOC Complexities

Understanding the intricacies of HELOCs can be challenging. Platforms like HELOC360 help homeowners navigate these complexities, ensuring a comprehensive understanding of this financing option. Such services connect borrowers with lenders offering competitive rates and terms, tailored to specific financial situations.

As we move forward, let's explore another popular home equity borrowing option: the home equity loan. This alternative offers a different structure and set of benefits, which may better suit certain financial goals and preferences.

What Are Home Equity Loans?

Definition and Structure

Home equity loans allow homeowners to borrow against their property's value, providing a lump sum of money with fixed terms. These loans deliver a one-time payout, which makes them suitable for large, one-off expenses.

How Home Equity Loans Work

When you take out a home equity loan, you receive the entire loan amount upfront. This structure benefits homeowners who have a clear understanding of their financial needs. For example, if you plan a major home renovation with a set budget, a home equity loan can provide the exact amount you require.

Repayment terms for home equity loans typically range from 5 to 30 years. Throughout this period, you make fixed monthly payments that include both principal and interest. This predictability can significantly advantage your budgeting efforts.

Interest Rates and Associated Costs

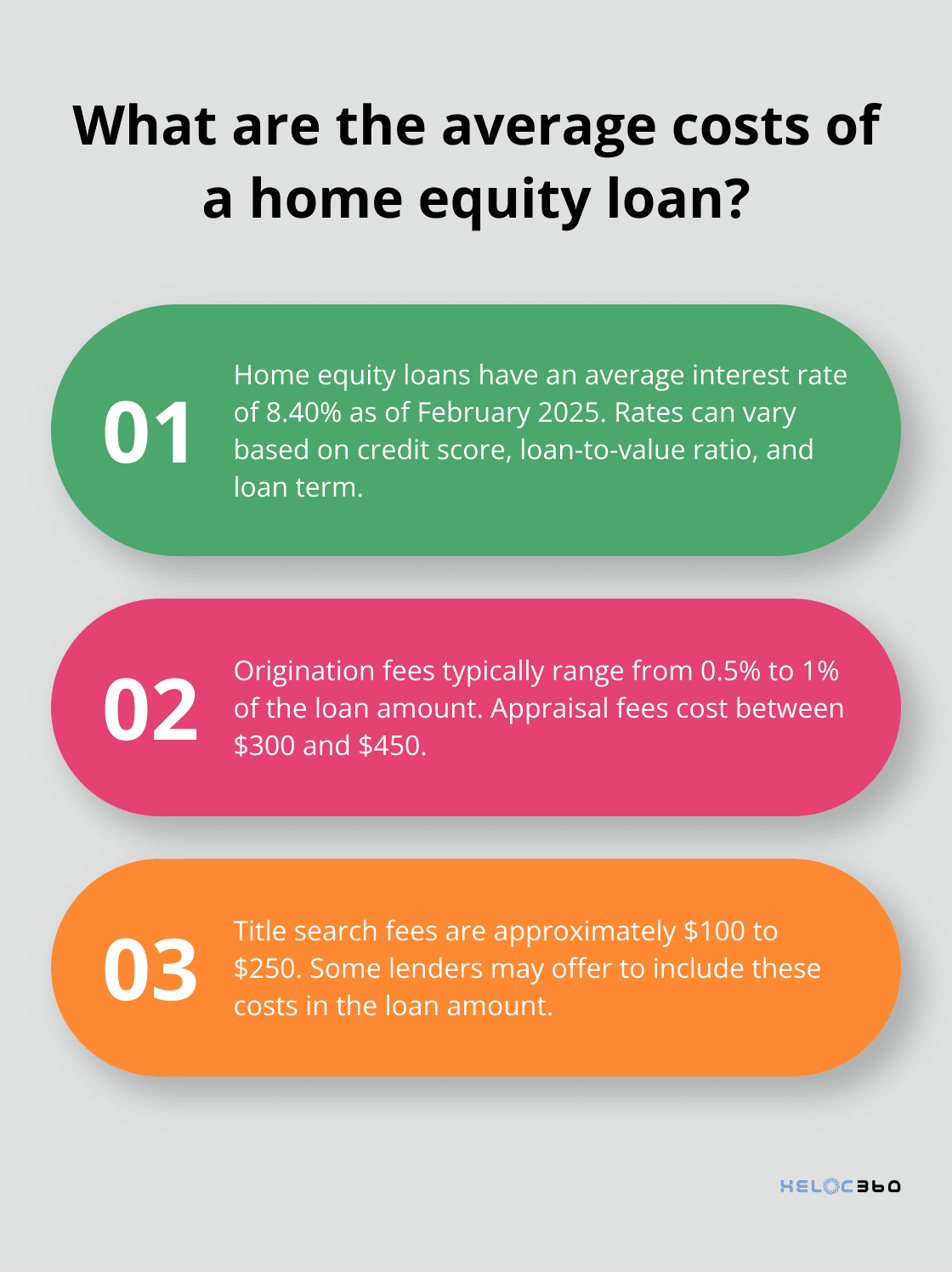

As of February 2025, the average interest rate for home equity loans stands at 8.40%. However, rates can vary based on factors such as credit score, loan-to-value ratio, and loan term.

Home equity loans generally come with fixed interest rates, which protect borrowers from market fluctuations. This stability can particularly appeal in a rising rate environment.

When you consider a home equity loan, prepare for various costs:

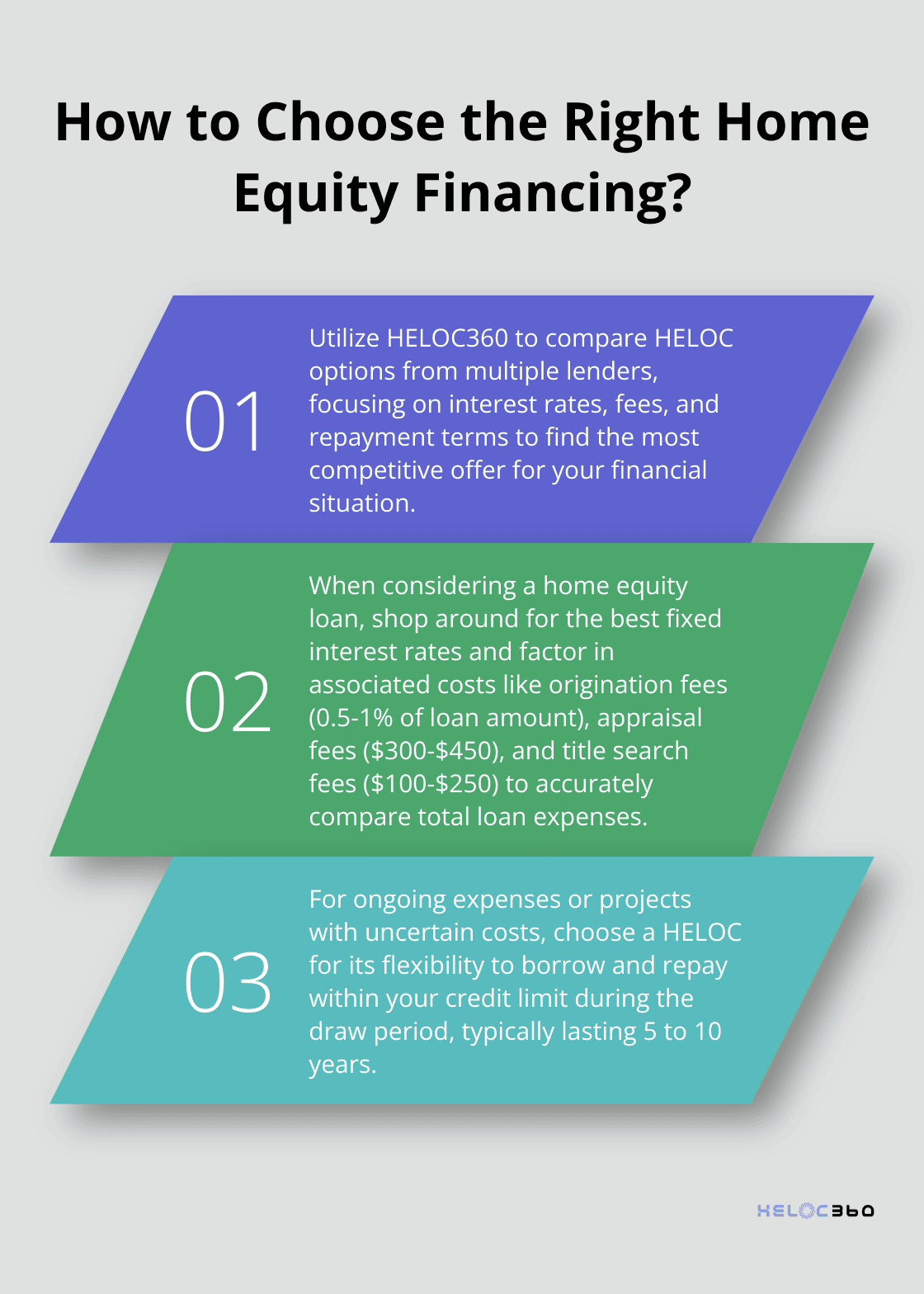

- Origination fees (0.5-1% of loan amount)

- Appraisal fees ($300–$450)

- Title search fees (approximately $100-$250)

Some lenders may offer to roll these costs into the loan, but this increases the overall amount you'll repay.

Strategies to Maximize Your Home Equity Loan

To make the most of a home equity loan:

- Shop around for the best rates. Don't settle for the first offer you receive.

- Consider the loan's purpose carefully. Using the funds for home improvements that increase your property's value can result in a smart financial move.

- Be mindful of your debt-to-income ratio. Taking on too much debt can strain your finances and potentially impact your ability to qualify for future loans.

- Understand the tax implications. While interest on home equity loans used for home improvements may qualify for tax deductions, consult with a tax professional to understand your specific situation.

Navigating the Home Equity Loan Landscape

The home equity loan market offers various options, each with its own set of terms and conditions. To navigate this landscape effectively, you need to understand how these loans compare to other financing options (such as HELOCs). In the next section, we'll explore the key differences between home equity loans and HELOCs, helping you determine which option aligns best with your financial goals.

Which Option Fits Your Financial Needs

Flexibility and Access to Funds

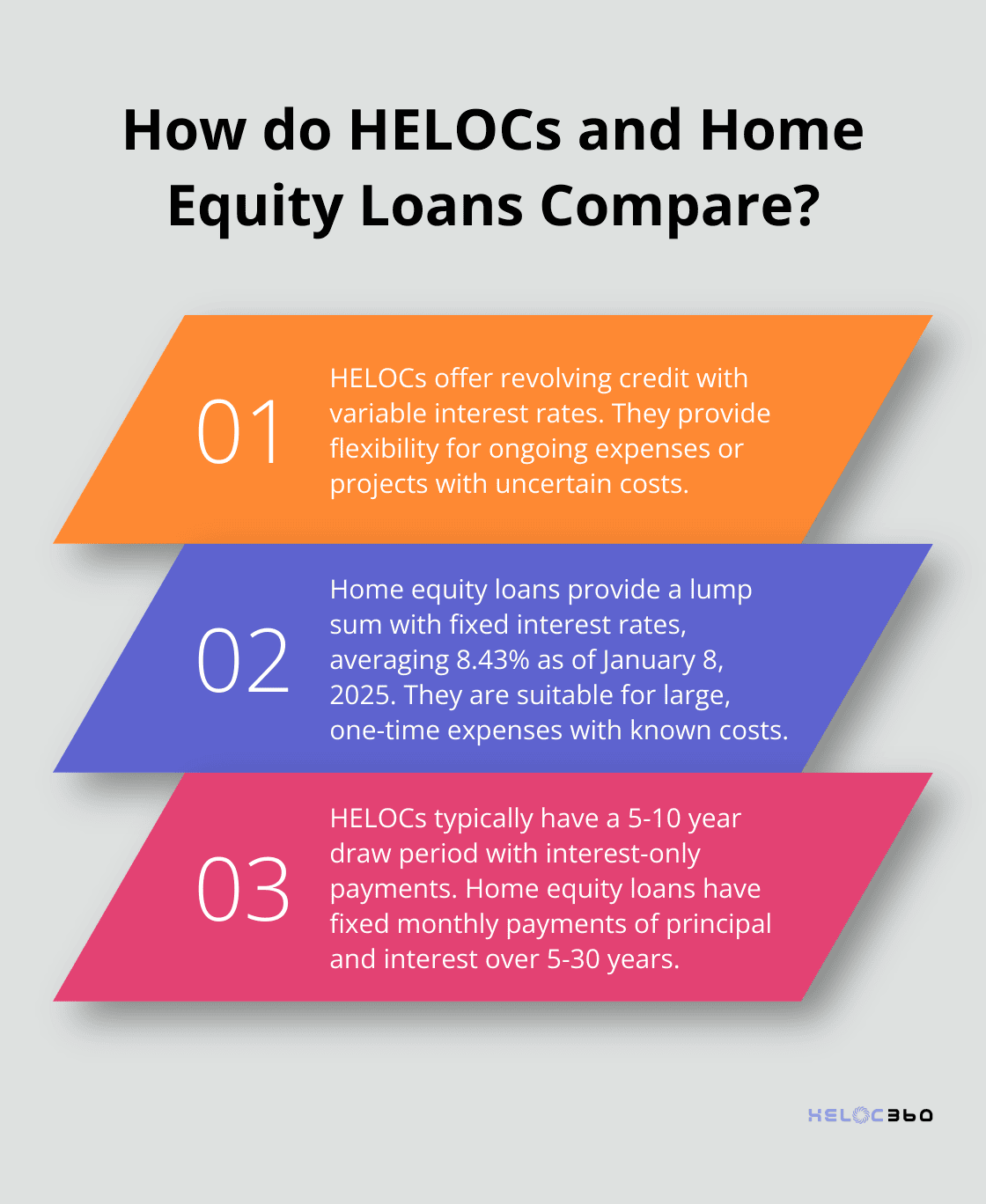

HELOCs offer more flexibility with their revolving credit structure. You can borrow, repay, and borrow again within your credit limit during the draw period. This makes HELOCs suitable for ongoing expenses or projects with uncertain costs. For example, if you plan a series of home improvements over time, a HELOC allows you to access funds as needed.

Home equity loans provide a lump sum upfront. This structure suits large, one-time expenses where you know the exact amount required. If you want to consolidate high-interest debt or fund a major home renovation with a set budget, a home equity loan might be the better choice.

Interest Rates and Payment Stability

HELOCs typically come with variable interest rates, which can fluctuate based on market conditions. This variability can lead to changing monthly payments, which some borrowers might find challenging to manage.

Home equity loans usually offer fixed interest rates, currently averaging 8.43% (as of January 8, 2025). This stability in interest rates translates to consistent monthly payments throughout the loan term, making budgeting more straightforward.

Repayment Terms and Structure

The repayment structure of HELOCs and home equity loans differs significantly. HELOCs often start with an interest-only payment period during the draw phase (typically lasting 5 to 10 years). After this, you enter the repayment phase where you pay both principal and interest.

Home equity loans have a more straightforward repayment structure. You start paying both principal and interest immediately, with fixed monthly payments over the loan term (usually ranging from 5 to 30 years).

Borrowers who prefer predictable payments often lean towards home equity loans, while those who value flexibility and potentially lower initial payments might opt for HELOCs.

Tax Considerations and Credit Impact

Both HELOCs and home equity loans can have tax implications. Interest paid on these loans may be tax-deductible if you use the funds for home improvements. However, the Tax Cuts and Jobs Act of 2017 placed limitations on this deduction. The deduction can be claimed only for the interest paid on mortgage debt up to $750,000 if the loan was taken out after Dec. 15, 2017, or $375,000 for married couples filing separately. You should consult with a tax professional to understand how these loans might affect your specific tax situation.

Regarding credit impact, both options can affect your credit score similarly. Opening either a HELOC or a home equity loan results in a hard inquiry on your credit report. Additionally, both are secured by your home, meaning failure to repay could put your property at risk.

The choice between a HELOC and a home equity loan depends on your financial goals, comfort with variable rates, and need for flexibility. HELOC360 can help you navigate these options, ensuring you make an informed decision that aligns with your unique financial situation.

Final Thoughts

Your choice between a HELOC and a home equity loan depends on your financial goals and preferences. HELOCs provide flexibility for ongoing expenses, while home equity loans suit large, one-time costs. Your comfort with variable rates, need for payment stability, and long-term financial plans should guide your decision.

Home equity financing can be complex, but tools like HELOC360 simplify the process. HELOC360 offers expert guidance and connects you with suitable lenders. This platform helps homeowners make informed decisions about leveraging their home equity for renovations, debt consolidation, or financial flexibility.

A thorough HELOC comparison will help you find the best fit for your situation. Understanding each option's nuances and using resources like HELOC360 can support your financial goals. You can confidently choose the path that maximizes your home's value and aligns with your needs.

Related Articles

Funding College with a HELOC Is It the Right Choice?

Explore if using a HELOC for college tuition is wise. Learn the benefits, risks, and real-world examples in this insightful guide.

When's the Perfect Time to Apply for a HELOC?

Find the ideal HELOC timing. Explore key factors affecting when to apply for a HELOC and secure the best rates for your financial goals now.

What is a Home Equity Line of Credit Loan?

Discover what a home equity line of credit loan is and how it can improve your finances. Get tips for effective HELOC management.