How Does a HELOC Impact Your Credit Score?

Table of Contents

At HELOC360, we often get questions about how a Home Equity Line of Credit (HELOC) affects credit scores. It's a common concern for homeowners considering this financial tool.

Understanding the relationship between HELOCs and credit scores is essential for making informed decisions about your home's equity. This post will explore the short-term and long-term impacts of a HELOC on your credit score, helping you navigate this important aspect of home financing.

What's a HELOC and Why Does Your Credit Score Matter?

Understanding Home Equity Lines of Credit (HELOCs)

A Home Equity Line of Credit (HELOC) is a line of credit based on your home's equity. The more equity (value) you've built up in the home, the more money you can access via a HELOC. It functions as a revolving credit line, similar to a credit card, but uses your home as collateral. Homeowners can borrow, repay, and borrow again up to their credit limit during the draw period (typically 5-10 years).

The Anatomy of Credit Scores

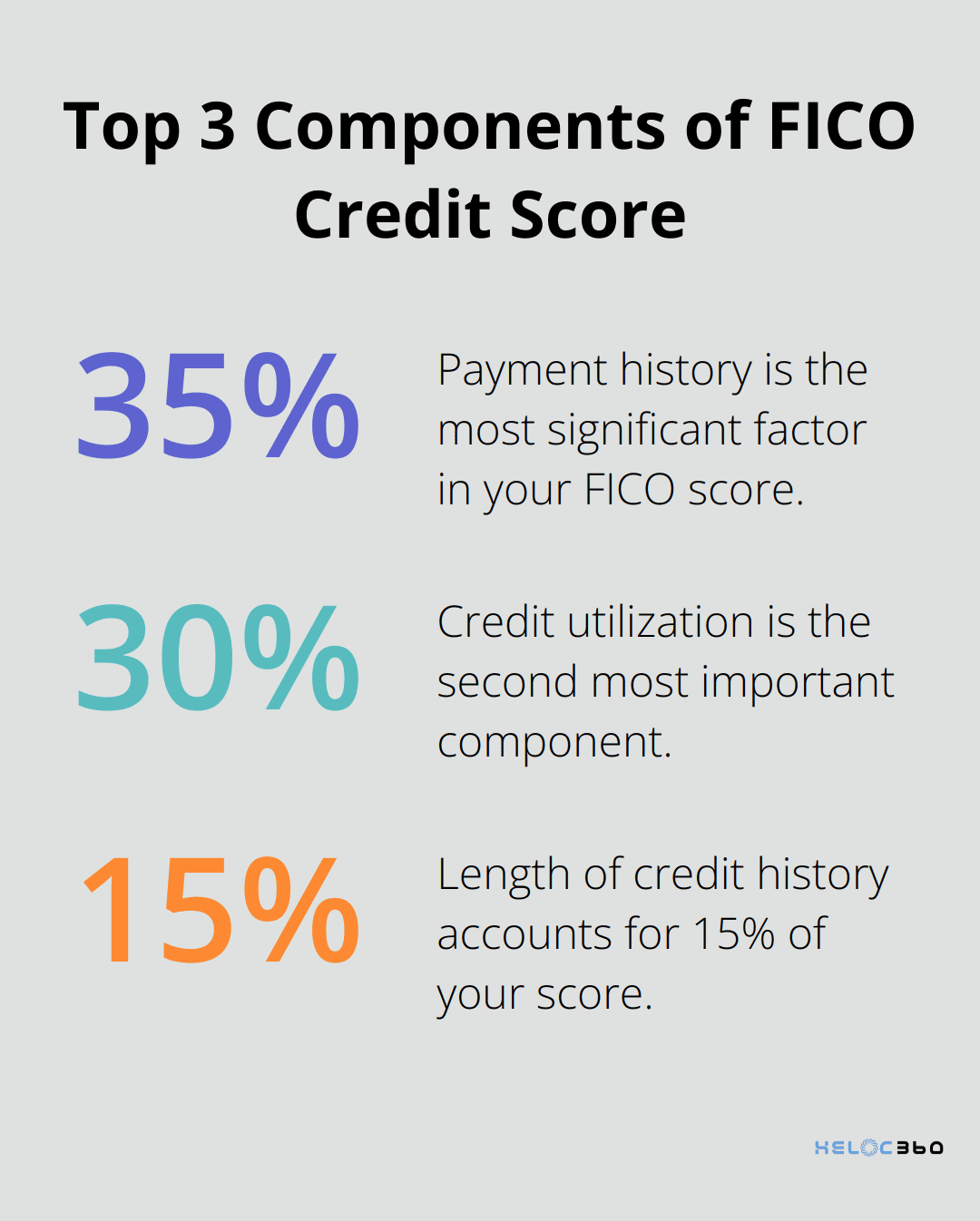

Credit scores numerically represent your creditworthiness, ranging from 300 to 850. Complex algorithms calculate these scores using various factors from your credit report. The most significant components include:

- Payment history (35% of your FICO score)

- Credit utilization (30%)

- Length of credit history (15%)

- Credit mix (10%)

- New credit inquiries (10%)

These percentages highlight what lenders value most. Consistent on-time payments and low credit utilization stand out as the two most impactful ways to maintain a healthy credit score. Generally, keeping credit utilization below 10% (and consistently paying bills on time) can help you build and maintain a good FICO® Score.

The Importance of Credit Scores for Homeowners

For homeowners, a good credit score opens doors to numerous financial opportunities:

- Better HELOC terms: Higher credit scores often lead to lower interest rates, potentially saving thousands over the loan's life.

- Higher borrowing limits: Lenders typically approve larger credit lines for borrowers with excellent credit scores.

- Future refinancing options: A strong credit score proves essential for securing the best rates when refinancing your mortgage.

- Insurance premiums: Many insurance companies use credit-based insurance scores to determine premiums (a better credit score could mean lower homeowners insurance costs).

- Emergency financial cushion: Good credit scores provide more options for quick access to funds for unexpected home repairs or other emergencies.

Most lenders want to see a minimum credit score of 620 in order to qualify for a home equity loan or HELOC. However, a higher credit score can lead to better terms and rates.

The Interplay Between HELOCs and Credit Scores

When you apply for a HELOC, lenders perform a hard inquiry on your credit report. This inquiry can temporarily lower your score by a few points. However, the long-term effects of a HELOC on your credit score can be positive if managed responsibly.

Timely payments and maintaining a low balance relative to your credit limit demonstrate responsible credit use. This positive payment history can contribute to an improved credit score over time.

As we move forward, we'll explore the initial impact of opening a HELOC on your credit score, including the effects of hard inquiries and how new credit lines influence your overall credit profile.

How Opening a HELOC Impacts Your Credit Score

The Hard Inquiry Effect

When you apply for a Home Equity Line of Credit (HELOC), lenders perform a hard inquiry on your credit report. This inquiry allows them to assess your creditworthiness but also impacts your credit score. Multiple hard inquiries from loan applications can hurt your credit scores. However, the impact could depend on which loans you apply for.

If you're comparing HELOC offers, you'll benefit from the rate shopping window. Credit scoring models often treat multiple inquiries within a 14-45 day period as a single inquiry, allowing you to find the best rates without excessive damage to your score.

Credit Utilization Changes

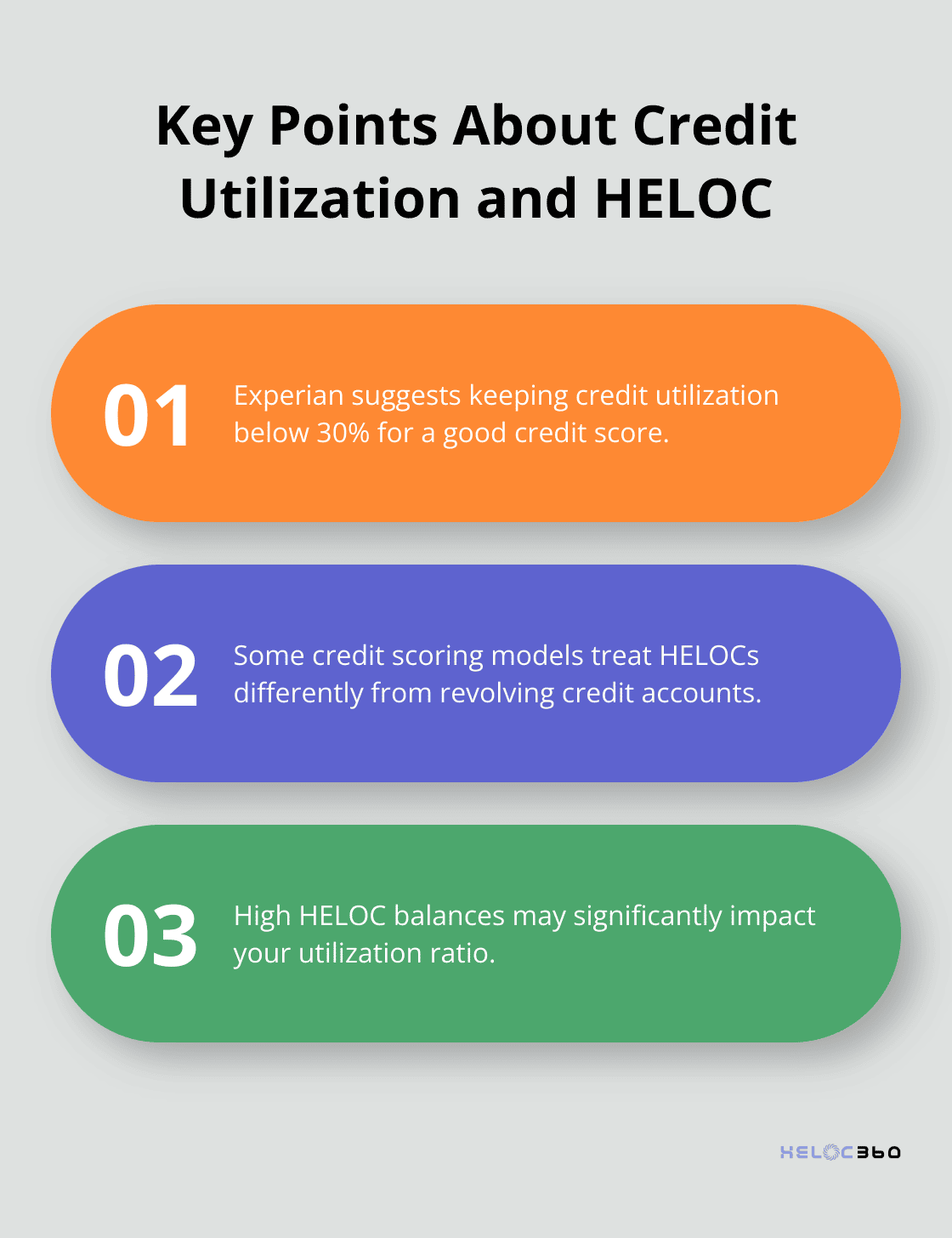

Your credit utilization ratio (which could affect around 20% to 30% of your credit score depending on the scoring model) will shift when you open a HELOC. Initially, your HELOC balance will likely be zero, which can positively affect your overall credit utilization. However, this ratio will change as soon as you start using your HELOC.

Experian suggests keeping your credit utilization below 30% to maintain a good credit score. It's important to note that some credit scoring models treat HELOCs differently from revolving credit accounts like credit cards. In some cases, HELOCs may not significantly impact your utilization ratio unless you carry a high balance.

New Credit and Account Age Considerations

A new HELOC appears as a new account on your credit report, which can temporarily lower your average account age. The length of credit history accounts for 15 percent of your FICO score and around 20 percent of your VantageScore credit score, so this effect can cause a slight dip in your credit score.

The new credit factor (10% of your FICO score) also considers recently opened accounts. Opening a HELOC signals that you're taking on new debt, which credit scoring models may view as a potential risk.

Short-Term vs. Long-Term Effects

While these factors can lead to a short-term decrease in your credit score, the impact is usually minimal and temporary. As you manage your HELOC responsibly over time (making timely payments and maintaining a low balance), you're likely to see your credit score recover and potentially improve.

Understanding these credit implications can help you make informed decisions about your HELOC. The next section will explore the long-term effects of a HELOC on your credit, including how responsible management can positively influence your credit profile over time.

How a HELOC Affects Your Credit Long-Term

The Impact of Payment History

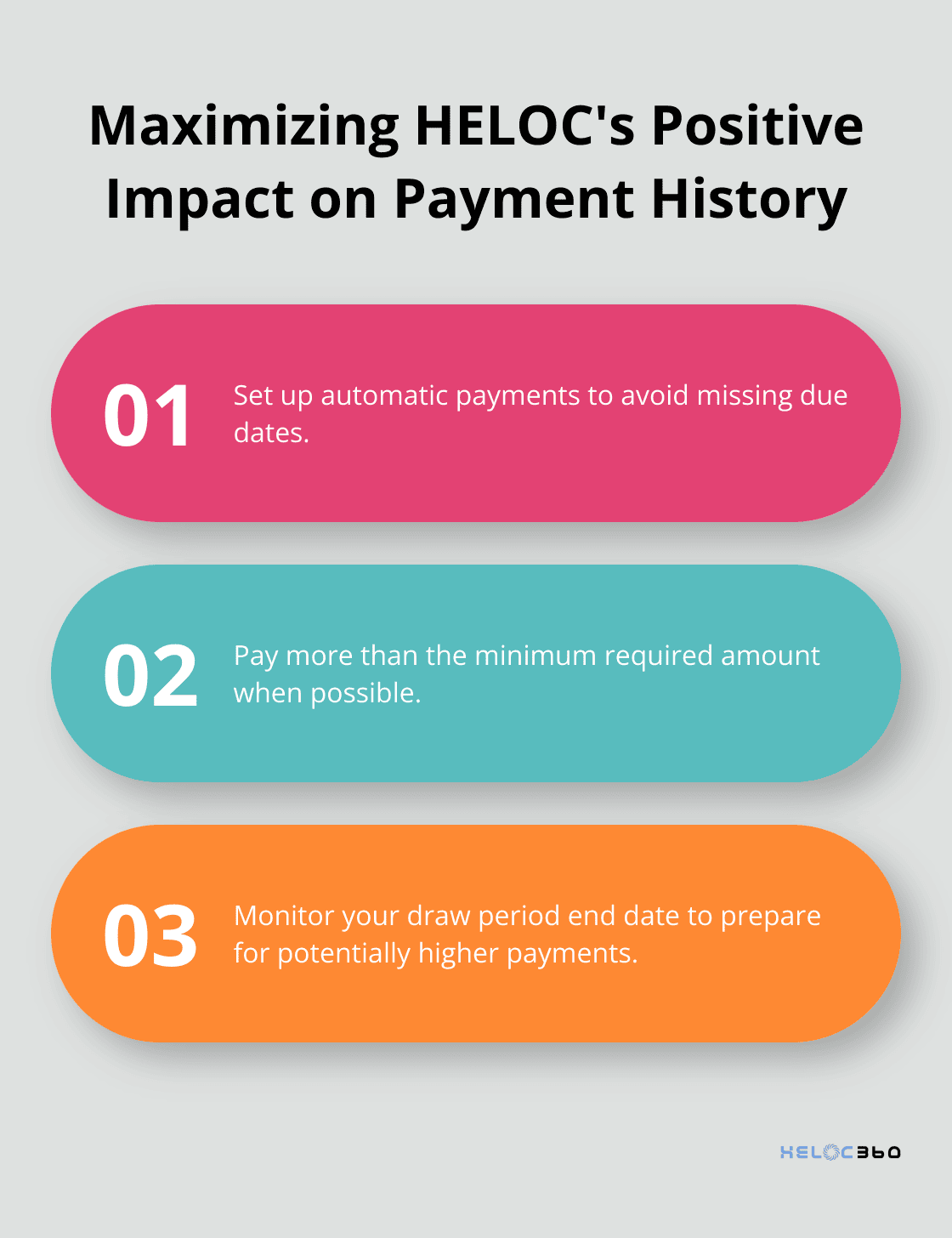

Your payment history constitutes 35% of your FICO score, making it the most influential factor in credit score calculations. Consistent, on-time payments on your HELOC can significantly boost your credit score over time.

To maximize the positive impact of your HELOC on your payment history:

- Set up automatic payments to avoid missing due dates.

- Pay more than the minimum required amount when possible.

- Monitor your draw period end date to prepare for potentially higher payments during the repayment period.

Credit Mix Diversification

Credit scoring models favor a diverse mix of credit types, including revolving accounts and installment loans. A HELOC adds to this diversity, potentially improving your credit mix (which accounts for about 10% of your FICO score).

Responsible management of different credit types, including a HELOC, demonstrates to lenders that you can handle various financial obligations.

Credit Utilization Management

Your credit utilization ratio measures how much of your available credit you're using and plays a key role in your credit score. While HELOCs sometimes receive different treatment than credit cards in utilization calculations, maintaining a low balance relative to your credit limit remains beneficial.

To optimize your HELOC's impact on credit utilization:

- Try to keep your HELOC balance below 30% of your credit limit.

- Consider making small, regular payments instead of waiting for the monthly due date.

- If you use your HELOC for debt consolidation, avoid maxing out the line to maintain a healthy utilization ratio.

Long-Term Credit Score Improvement Potential

A responsibly managed HELOC can lead to credit score improvements over time. However, it's important to note that applying for a HELOC may cause a slight drop in your credit score.

It's important to note that a HELOC is secured by your home. Failure to make payments not only damages your credit score but also puts your home at risk of foreclosure. Always borrow within your means and create a clear repayment plan.

Consistent, on-time payments, low balance maintenance, and use of your HELOC as part of a diverse credit portfolio can enhance your credit profile in the long run. Responsible HELOC management is the key to reaping these long-term credit benefits.

Final Thoughts

A Home Equity Line of Credit (HELOC) can affect your credit score in various ways. The initial hard inquiry and new account opening might cause a small decrease in your score. However, responsible HELOC management can lead to positive impacts on your credit profile over time.

Your HELOC score (the credit score lenders use to evaluate your HELOC application) depends on factors like timely payments and low utilization. At HELOC360, we help homeowners understand these credit implications and make the most of their home equity. We connect you with lenders that match your specific needs, simplifying the process and supporting your financial goals.

A HELOC can serve as a powerful financial tool when managed correctly. It can open doors to renovations, debt consolidation, or increased financial flexibility while maintaining a healthy credit profile. With the right approach and support, you can leverage your home's equity to create new opportunities.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.