How to Estimate HELOC Payments with a Calculator

Table of Contents

Estimating your HELOC payments accurately is crucial for effective financial planning. At HELOC360, we understand the importance of having reliable tools at your disposal.

A HELOC payments calculator can be an invaluable resource in this process. In this post, we'll guide you through the key factors affecting HELOC payments and show you how to use these calculators effectively.

How HELOC Payment Structures Work

Variable vs. Fixed Interest Rates

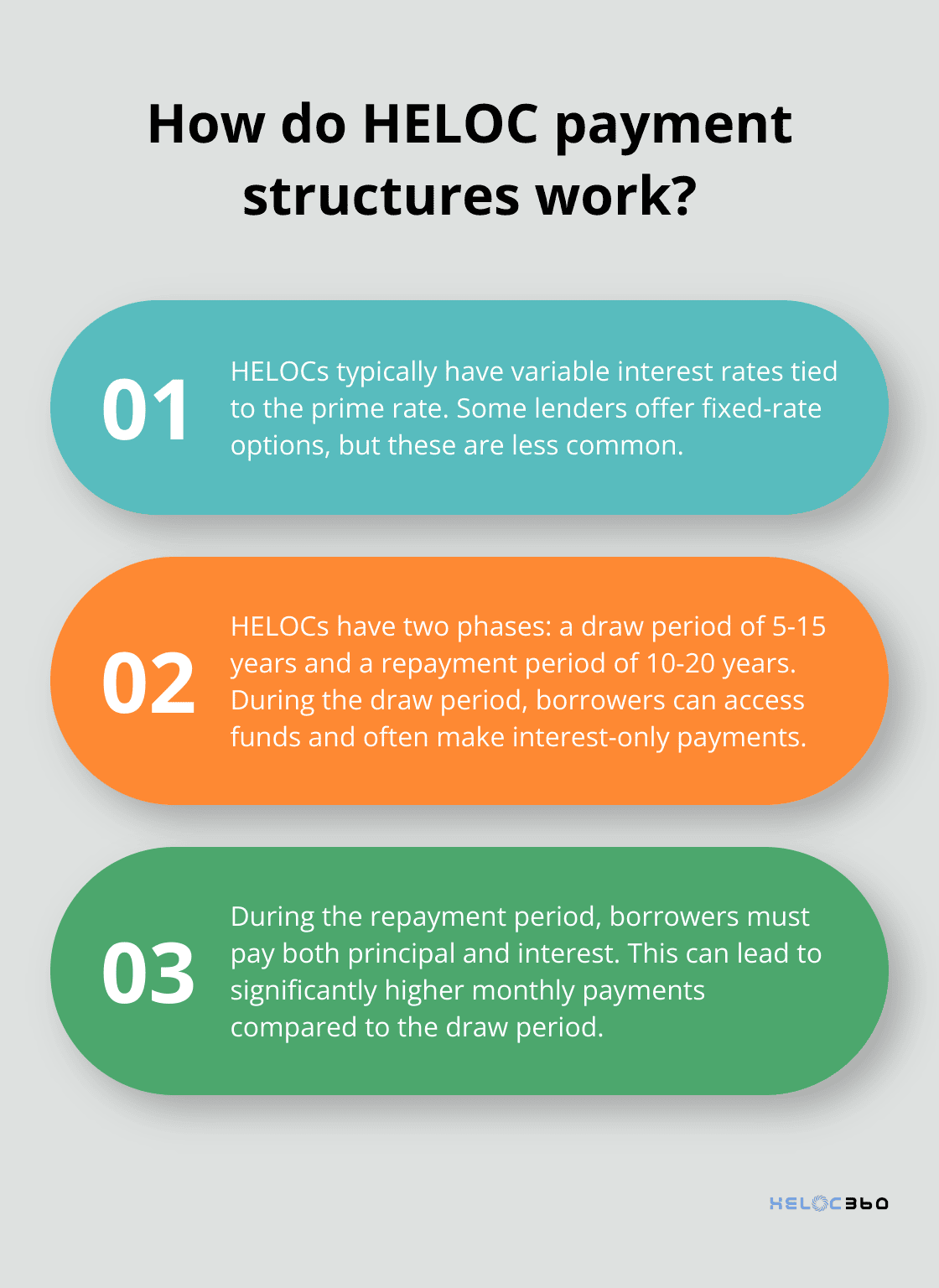

Most HELOCs feature variable interest rates. These rates change based on the prime rate, which the Federal Reserve's decisions influence. For example, if the prime rate increases, your HELOC rate will likely increase as well. This variability can significantly impact your monthly payments.

Some lenders offer fixed-rate options for HELOCs, but these are less common. Fixed-rate HELOCs provide more predictable payments but often come with higher initial rates compared to variable-rate options.

The Two Phases of a HELOC

HELOCs operate in two distinct phases: the draw period and the repayment period. The draw period usually lasts 5 to 15 years, during which you can borrow from your credit line as needed. Many lenders only require interest payments during this time, which can keep your monthly costs low.

The repayment period follows, typically lasting 10 to 20 years. During this phase, you can no longer borrow from the credit line and must repay both principal and interest. This shift can lead to a significant increase in your monthly payments.

Payment Options During the HELOC Lifecycle

During the draw period, you often have the choice between making interest-only payments or paying both principal and interest. Interest-only payments can be tempting due to their lower cost, but they don't reduce your principal balance.

Once the repayment period begins, you'll need to make full principal and interest payments. These payments are usually calculated to fully amortize the loan over the repayment period. For instance, if you borrowed $50,000 during the draw period and your repayment period is 15 years, your monthly payments would be structured to pay off the entire $50,000 plus interest over those 15 years.

Impact on Financial Planning

Understanding these payment structures is essential for effective financial planning. You can better prepare for future financial obligations and make informed decisions about using your HELOC when you grasp how your payments may change over time.

For example, if you opt for interest-only payments during the draw period, you should plan for the increased payments during the repayment period. This might involve setting aside extra funds or considering refinancing options before the repayment period begins.

Choosing the Right HELOC Structure

When selecting a HELOC, consider your long-term financial goals and current situation. If you value predictability, a fixed-rate HELOC (although less common) might be the better choice. On the other hand, if you're comfortable with some uncertainty and want to take advantage of potentially lower rates, a variable-rate HELOC could be more suitable.

It's also worth noting that some lenders offer hybrid options, allowing you to lock in a fixed rate on a portion of your balance while keeping the rest variable. This flexibility can be particularly useful if you want to hedge against rate increases on a specific amount (e.g., for a planned home renovation project).

Now that we've covered the basics of HELOC payment structures, let's explore the key factors that affect your HELOC payments and how they can impact your overall costs.

What Influences Your HELOC Payments?

Credit Score: Your Financial Report Card

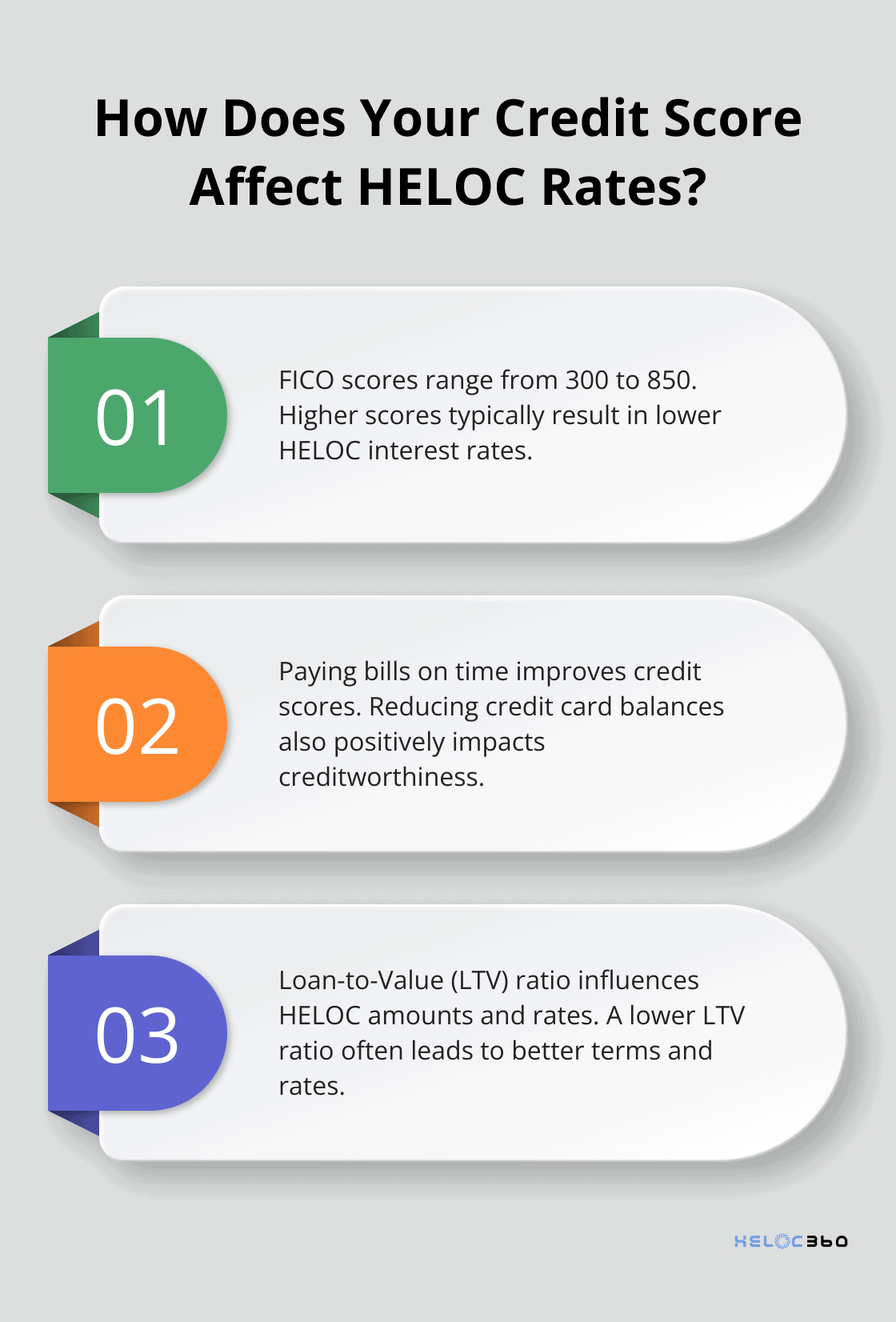

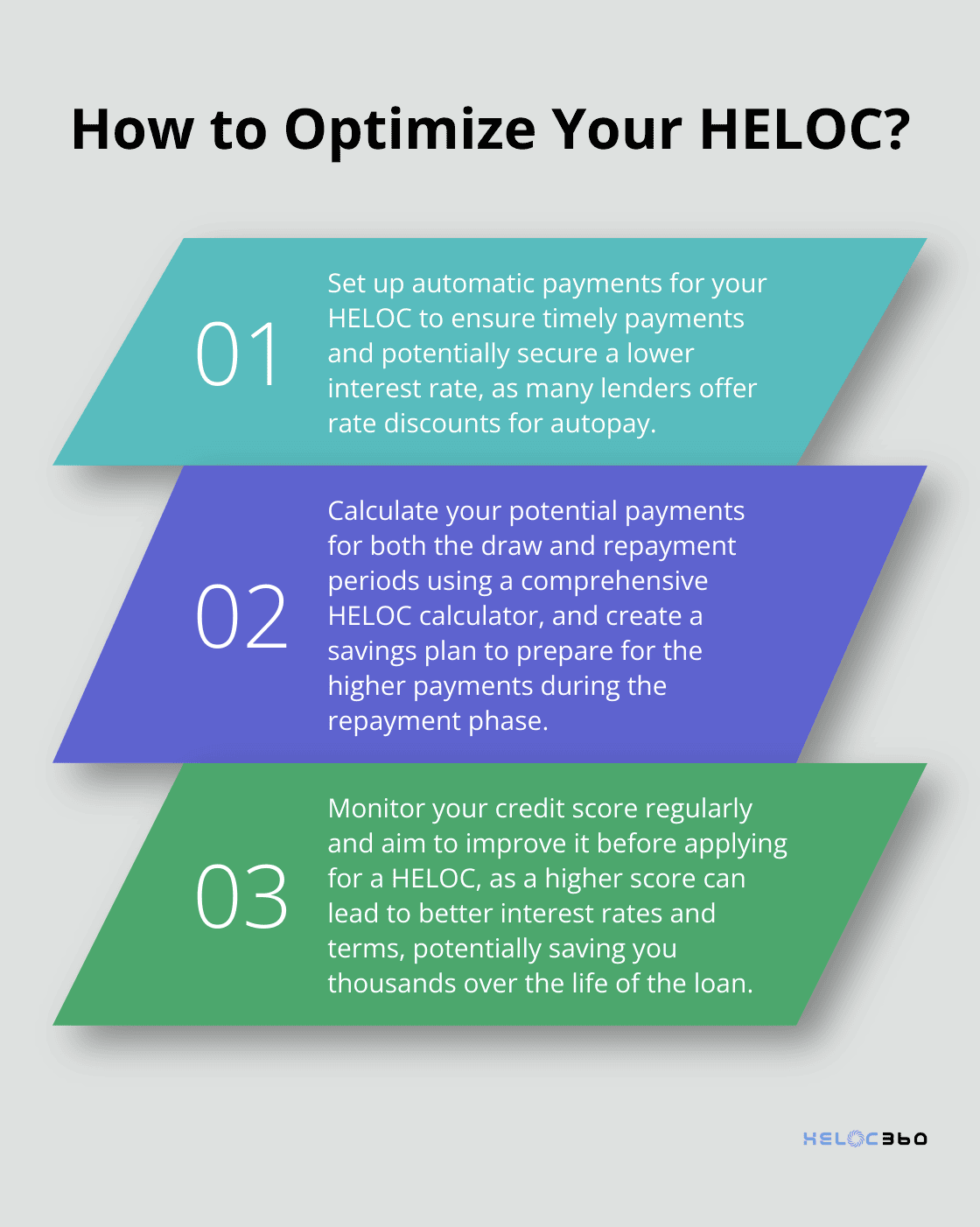

Your credit score impacts the interest rate you'll receive on your HELOC. FICO scores range from 300 to 850, with higher scores indicating better creditworthiness. A borrower with a higher score might secure a HELOC with a lower interest rate compared to someone with a lower score.

To improve your chances of getting a lower rate:

- Pay bills on time

- Reduce credit card balances

- Avoid applying for new credit before seeking a HELOC

These actions can potentially save you money over the life of your HELOC.

Loan-to-Value Ratio: Borrowing Capacity

The loan-to-value (LTV) ratio determines your HELOC amount and interest rate. A high LTV ratio can indicate that the loan amount is a higher percentage of the home's value, which makes the loan risker for the lender.

A lower LTV ratio often results in better rates and terms. If you're close to the LTV limit, try to increase your home's value or pay down your existing mortgage to improve your position.

Market Interest Rates: Economic Backdrop

Current market conditions play a significant role in HELOC rates. HELOCs typically tie to the prime rate, which the Federal Reserve's decisions influence. As of January 2025, the prime rate is expected to be around 7% if current forecasts remain accurate.

Monitor economic indicators and Federal Reserve announcements. If rates are expected to rise, it might be wise to lock in a rate sooner. Conversely, if rates are predicted to fall, waiting could benefit you.

Income and Debt-to-Income Ratio

Your income and debt-to-income (DTI) ratio affect your HELOC eligibility and terms. Lenders typically prefer a DTI ratio below 43% (including your potential HELOC payment). A higher income and lower DTI ratio can lead to more favorable terms and higher borrowing limits.

To improve your DTI:

- Pay off existing debts

- Increase your income (e.g., through a side job or promotion)

- Avoid taking on new debts before applying for a HELOC

Property Type and Location

The type and location of your property influence your HELOC terms. Single-family homes in desirable areas often receive better rates and higher borrowing limits compared to condos or properties in less stable markets.

Factors that can affect your HELOC based on property:

- Local real estate market conditions

- Property type (single-family, multi-family, condo)

- Occupancy status (primary residence, second home, investment property)

Understanding these key factors empowers you to make informed decisions about your home equity borrowing strategy. In the next section, we'll explore how to use HELOC payment calculators to estimate your potential payments accurately.

How to Use HELOC Payment Calculators Effectively

Types of HELOC Calculators

HELOC payment calculators are powerful tools that help you estimate your monthly payments and interest rates. These calculators come in various forms, each designed to provide specific insights into your HELOC payments.

- Basic Payment Estimators: These provide a quick overview of potential monthly payments based on your loan amount, interest rate, and term.

- Draw vs. Repayment Period Calculators: These advanced tools allow you to input different payment scenarios for both the draw and repayment periods.

- Amortization Schedule Calculators: These detailed calculators show how your balance will decrease over time, helping you understand the long-term impact of your payments.

When selecting a calculator, consider your specific needs. If you're in the early stages of planning, a basic estimator might suffice. For more detailed financial planning, opt for a comprehensive calculator that factors in both draw and repayment periods.

Essential Information for Accurate Estimates

To get the most accurate results from a HELOC calculator, you'll need to gather some key information:

- Loan Amount: The total amount you plan to borrow or your credit limit.

- Interest Rate: Your current rate or an estimated rate based on your credit score and market conditions.

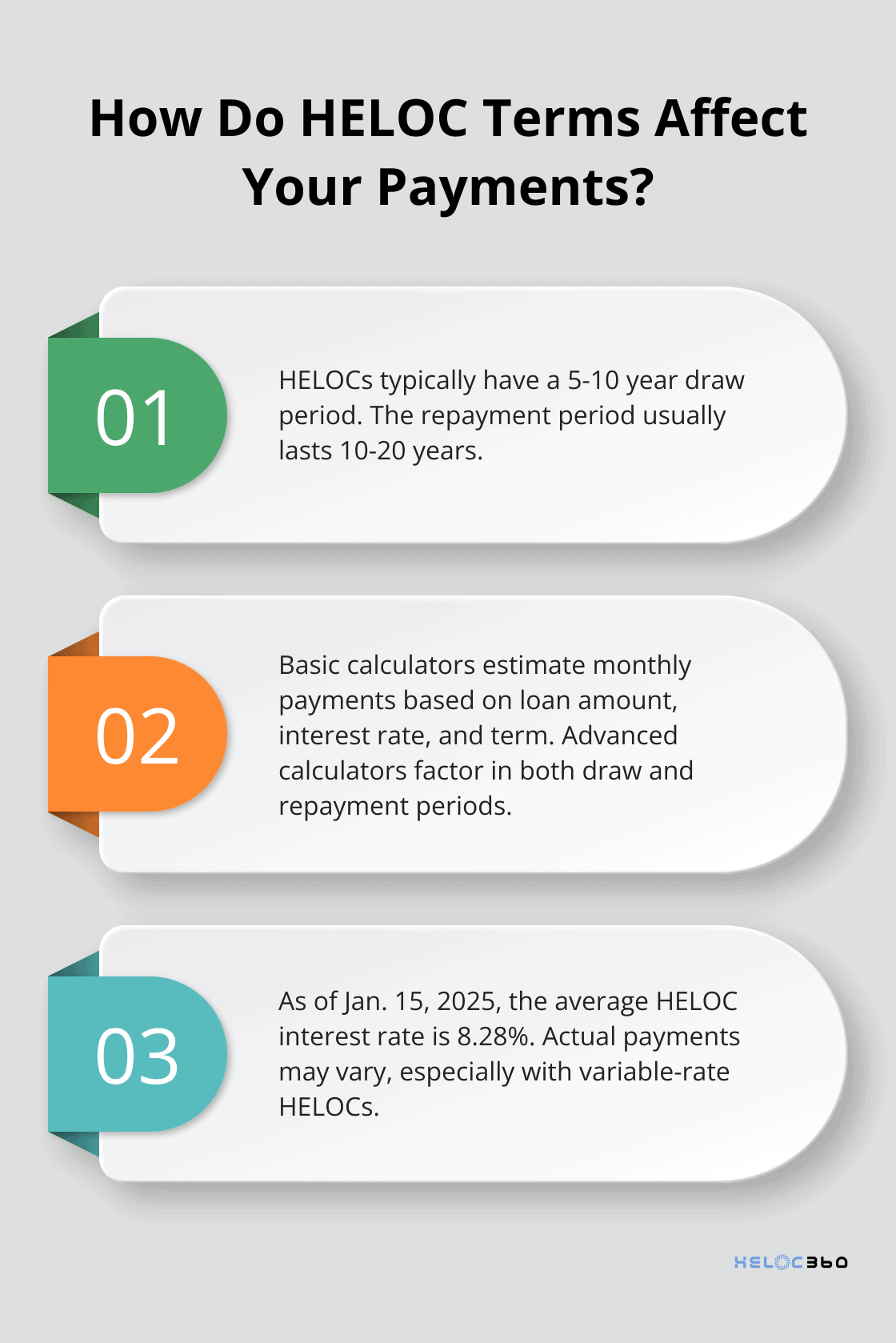

- Draw Period Length: Typically 5-10 years, but can vary by lender.

- Repayment Period Length: Usually 10-20 years.

- Payment Type During Draw Period: Interest-only or principal and interest.

It's important to use realistic figures. If you overestimate your borrowing needs or underestimate interest rates, you'll end up with inaccurate projections. If you're unsure about certain values, it's better to use slightly higher estimates for interest rates and loan amounts (this errs on the side of caution).

Interpreting Calculator Results

Once you've input your information, the calculator will provide you with estimated payments. Here's how to interpret these results:

- Monthly Payments: Look at how these differ between the draw and repayment periods. The jump in payment amount when entering the repayment period can be substantial.

- Total Interest Paid: This figure can be eye-opening. Compare how much interest you'll pay with different payment strategies (e.g., interest-only vs. principal and interest during the draw period).

- Payoff Date: This shows when you'll be debt-free if you stick to the calculated payment schedule.

Use these results to assess the affordability of the HELOC. If the payments during the repayment period seem high, consider adjusting your borrowing amount or exploring options for a longer repayment term.

These calculators provide estimates based on current information. Actual payments may vary, especially with variable-rate HELOCs. As of Jan. 15, 2025, the current average HELOC interest rate is 8.28 percent. It's wise to recalculate periodically, particularly if market conditions change significantly.

HELOC payment calculators are invaluable tools for financial planning, but they're just one part of the equation. Combine these estimates with a thorough review of your overall financial situation and goals to make the most informed decision about your HELOC.

Final Thoughts

Accurate HELOC payment estimation forms the foundation of sound financial planning. A HELOC payments calculator helps you explore various scenarios and compare options during draw and repayment periods. This tool provides a clear picture of your long-term financial commitments, allowing you to stay on top of your HELOC strategy and make adjustments as needed.

We at HELOC360 understand the complexities of navigating home equity. Our platform simplifies the process and provides the resources you need to unlock your home's full potential. We offer comprehensive HELOC solutions designed for major renovations, debt consolidation, or financial flexibility.

Our expertise and tools (including advanced HELOC payment calculators) can help you confidently explore your options. You can find the right HELOC solution for your unique needs with our guidance through every step. Visit our comprehensive HELOC solutions to learn how we can support you in turning your home equity into a powerful asset for achieving your financial goals.

Related Articles

Boost Your Chances of HELOC Approval Today

Boost HELOC approval chances with expert tips, insights, and strategies. Secure the funds you need by knowing what lenders look for today.

Why HELOC Insurance Matters for Homeowners

Explore why HELOC insurance is essential for protecting your home's equity and securing financial stability for homeowners.

Hidden HELOC Closing Costs to Watch Out For

Uncover potential HELOC closing costs that might surprise you. Learn how to navigate fees and save money before signing on the dotted line.