Master These HELOC Strategies for Financial Success [2025]

Table of Contents

Home Equity Lines of Credit (HELOCs) are powerful financial tools that can transform your financial future. In 2025, mastering HELOC strategies is more important than ever for homeowners looking to leverage their property's value.

At HELOC360, we've seen firsthand how smart HELOC usage can lead to debt consolidation, home improvements, and even investment opportunities. This guide will walk you through the essentials of HELOCs and provide practical strategies for financial success in today's market.

What Are HELOCs and How Do They Work in 2025?

The Basics of Home Equity Lines of Credit

Home Equity Lines of Credit (HELOCs) allow homeowners to borrow, spend, and repay as they go, using their home as collateral. A HELOC is a line of credit that lets you withdraw funds when you need, borrowing against the equity in your home. Unlike traditional loans, HELOCs offer a revolving line of credit that homeowners can access as needed during a set draw period.

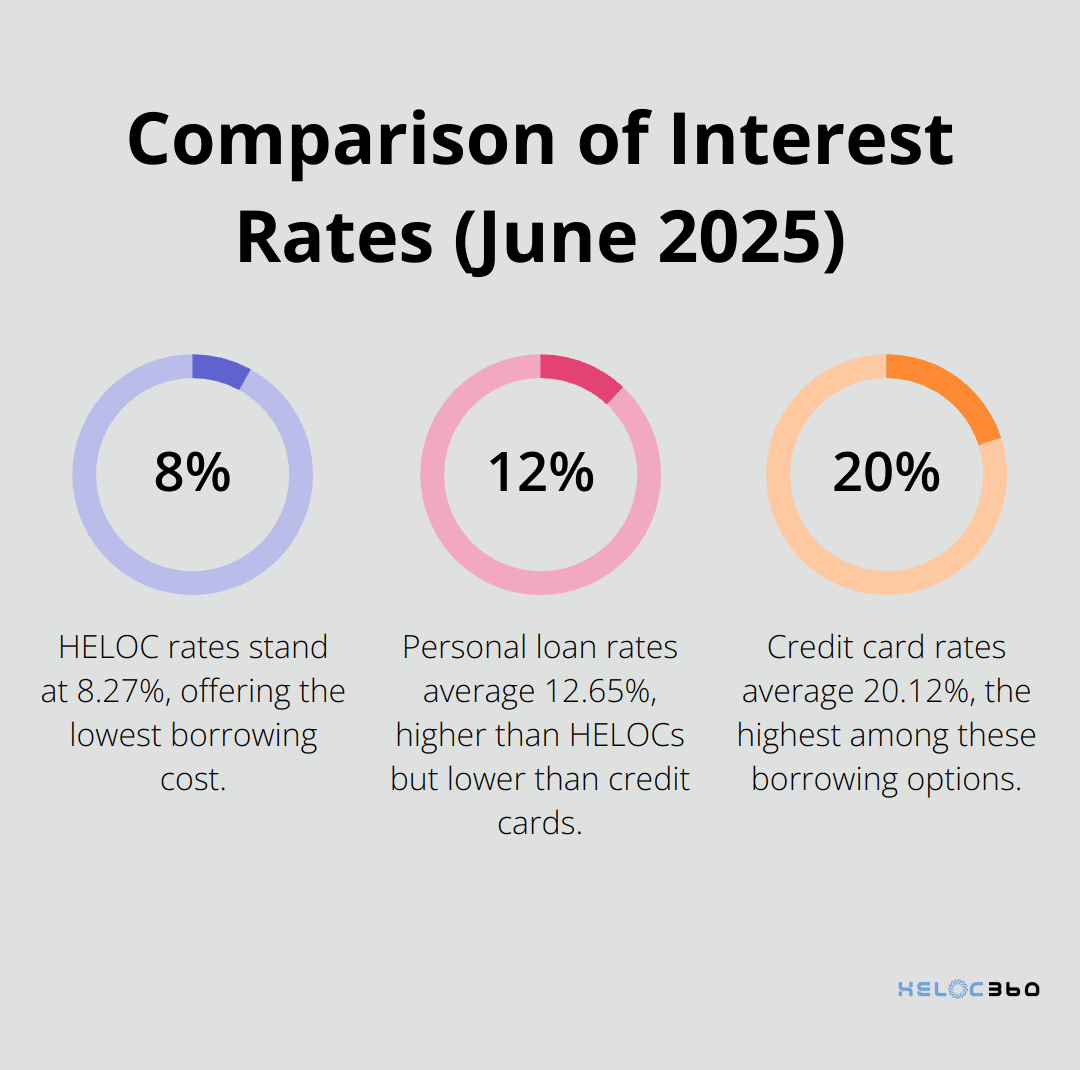

As of June 18, 2025, HELOC interest rates stand at 8.27%, according to Bankrate's latest survey of the nation's largest home equity lenders. This rate is significantly lower than the average personal loan rate (12.65%) and the average credit card rate (20.12%). However, HELOC rates are variable and tied to the prime rate, which can fluctuate based on Federal Reserve policies.

Qualification Requirements for HELOCs

To qualify for a HELOC, lenders typically require a credit score of 620 or higher. However, to secure the most competitive rates, a score of 740 or above is often necessary. Additionally, most lenders look for a combined loan-to-value (CLTV) ratio below 85%. This means that the total of your mortgage balance and desired HELOC amount should not exceed 85% of your home's current market value.

The application process for a HELOC has become more streamlined in recent years. Many lenders now offer online applications that homeowners can complete in under an hour. However, you'll still need to provide documentation such as proof of income, tax returns, and information about your existing mortgage.

Leveraging Your HELOC Effectively

One of the key advantages of HELOCs is their flexibility. You only pay interest on the amount you actually borrow, not the entire credit line. This makes HELOCs particularly useful for ongoing expenses like home renovations or education costs.

It's crucial to have a solid repayment plan in place. After the draw period (typically 10 years), the repayment period begins. During this time, you can no longer borrow and must repay the principal along with interest. This can lead to significantly higher monthly payments if you're not prepared.

Strategic Uses of HELOCs

Many homeowners use HELOCs to consolidate high-interest debt, fund home improvements that increase property value, or invest in income-generating properties. The key is to have a clear strategy and understand the terms of your HELOC before borrowing.

For example, using a HELOC to pay off high-interest debt or fund big-ticket expenses like home upgrades can be a smart financial move. HELOCs often offer lower interest rates than credit cards, unsecured personal loans and other alternatives. Similarly, funding a kitchen renovation with a HELOC could increase your home's value, potentially offsetting the cost of the loan.

As we move into the next section, we'll explore specific strategies for using HELOCs to achieve financial growth and success in 2025. These techniques will help you maximize the potential of your home equity while minimizing risks.

How HELOCs Can Boost Your Financial Growth

Debt Consolidation with HELOCs

Home Equity Lines of Credit (HELOCs) offer a powerful strategy for debt consolidation in 2025. The flexibility of a HELOC may make it easier to use to tackle credit-card debt compared with a home-equity loan.

Consider this scenario: A $20,000 credit card debt at 20.12% interest results in $4,024 in interest over one year. By using a HELOC at 8.27% to pay off this debt, you reduce your interest to $1,654 - a saving of $2,370 in just one year.

To maximize the benefits of debt consolidation with a HELOC, set up automatic payments. This approach helps you avoid the temptation of making only minimum payments, which can lead to long-term debt accumulation.

Home Value Boost Through Strategic Improvements

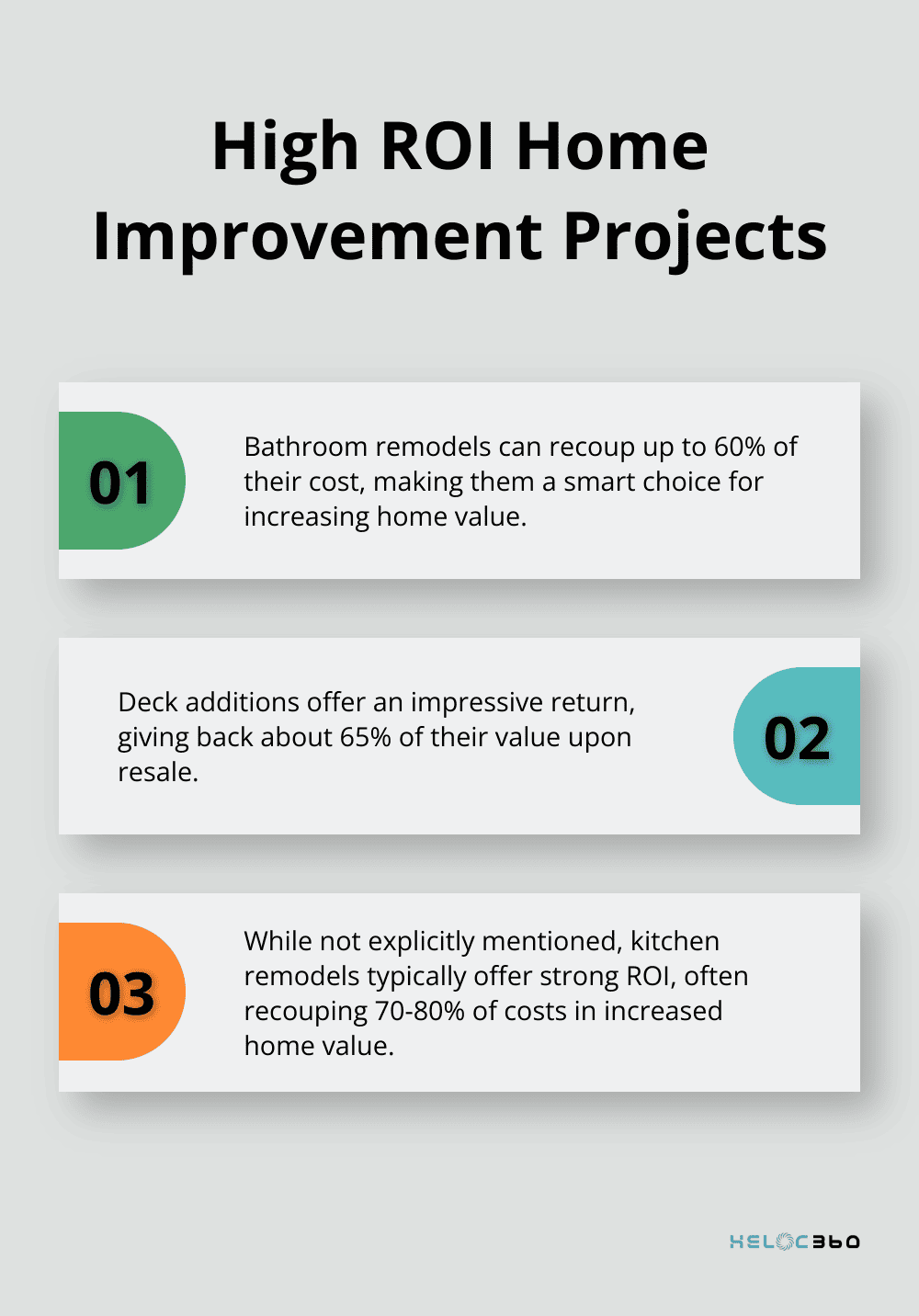

Using your HELOC for home improvements can increase your property's value, potentially creating a return on investment. The 2024 Cost vs. Value Report compares average costs for 23 remodeling projects with the value those projects retain at resale in 150 U.S. markets.

When planning renovations, focus on projects with high ROI:

- Bathroom remodels (recoup up to 60% of cost)

- Deck additions (return about 65% of value)

These improvements not only enhance your living space but also build additional equity in your home.

Investment Opportunities with HELOCs

HELOCs can fund various investment opportunities. The stock market has shown an average annual return of 10% over the long term, potentially yielding returns that outpace the interest rate on your HELOC.

Real estate investments present another option. The National Association of Realtors reports that in 2025, the share of Gen Z buyers and sellers aged 18 to 25 made up just three percent of buyers and two percent of sellers.

However, investing with borrowed money carries risks. You should thoroughly research any investment opportunity and consider consulting with a financial advisor before proceeding. Your home serves as collateral for your HELOC, so investment losses could put your property at risk.

Maximizing HELOC Benefits

To maximize the benefits of your HELOC:

- Create a clear repayment plan

- Use funds for high-ROI projects or investments

- Monitor interest rates and market conditions

- Consult with financial professionals for personalized advice

While HELOCs offer numerous opportunities for financial growth, they also come with potential pitfalls. In the next section, we'll explore common HELOC mistakes and how to avoid them, ensuring you make the most of this powerful financial tool.

How to Avoid HELOC Pitfalls

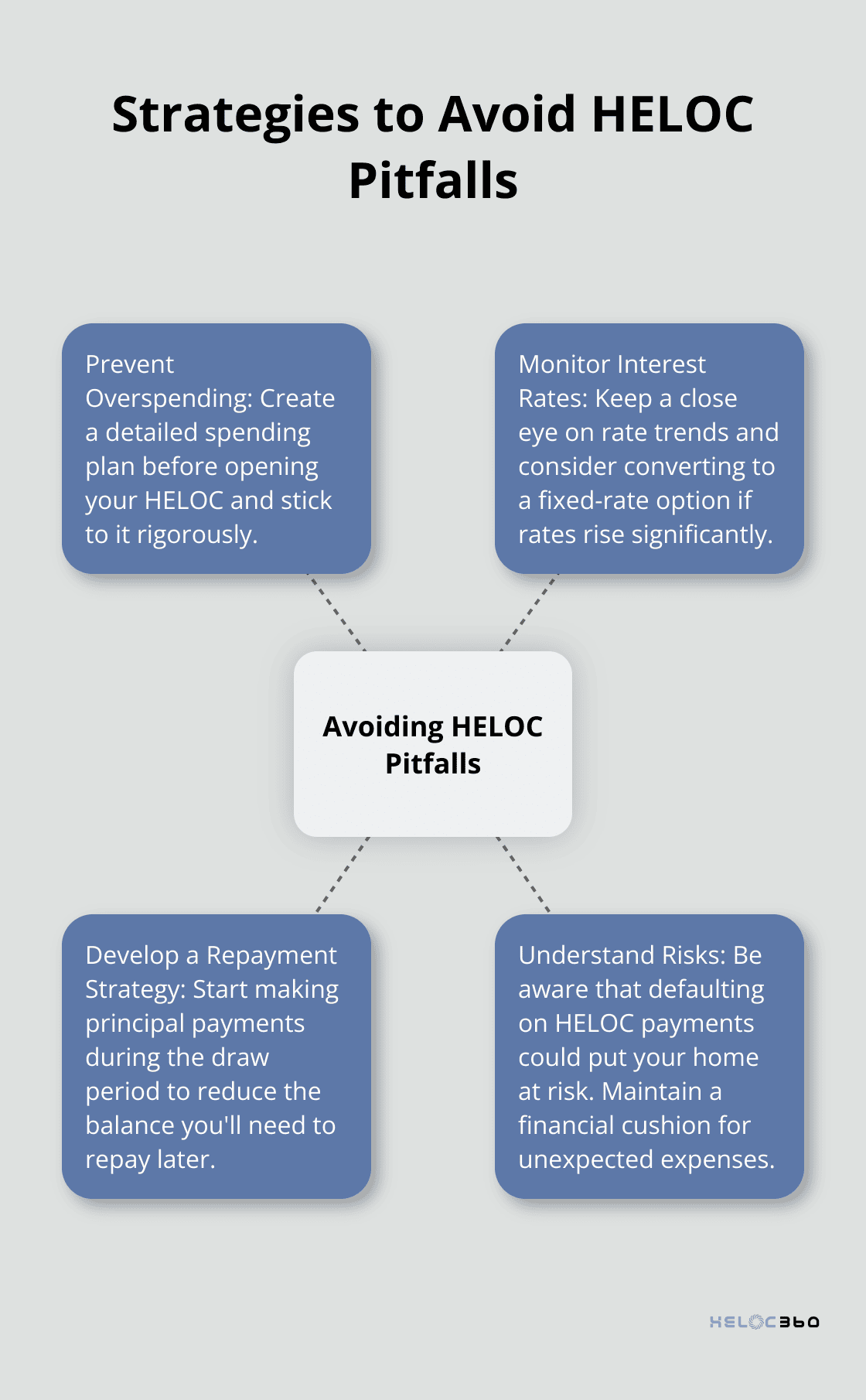

Prevent Overspending

HELOCs offer great financial opportunities, but they also come with risks. The ease of access to HELOC funds can lead to overspending. A study by the Federal Reserve Bank of Chicago found that for every $1 increase in home equity, homeowners borrowed 25 cents via home equity loans. This tendency to tap into home equity can quickly lead to financial strain.

To avoid this, create a detailed spending plan before you open your HELOC. Allocate funds to specific purposes and stick to your plan. If you plan to use the HELOC for home improvements, get quotes from contractors beforehand to ensure you borrow only what you need.

Monitor Interest Rates

HELOC interest rates are variable, which means they can fluctuate based on market conditions. Current refinance rates are lower than home equity loan interest rates, averaging 6.95% for a 30-year fixed refinance.

Keep a close eye on interest rate trends. The Federal Reserve's decisions can impact HELOC rates, so stay informed about their meetings and policy changes. Set up rate alerts with your lender or use financial news apps to stay updated.

If rates start to rise significantly, explore options to convert part or all of your HELOC balance to a fixed-rate option. Many lenders offer this feature, which can provide more stability in your repayment plan.

Develop a Repayment Strategy

Failure to plan for repayment is a critical mistake. HELOCs typically have a draw period of 10 years, followed by a repayment period of up to 20 years. When the repayment period begins, your monthly payments can increase substantially as you start paying back the principal.

To avoid payment shock, start making principal payments during the draw period if possible. This approach can reduce the balance you'll need to repay later. Also, consider setting up automatic payments to ensure you never miss a due date.

If you use your HELOC for investments, have a clear exit strategy. Know how and when you'll repay the borrowed funds, especially if your investment doesn't perform as expected.

Understand the Risks of Using Home Equity

While HELOCs can provide financial flexibility, they also put your home at risk. If you default on your HELOC payments, you could potentially lose your home. Try to maintain a financial cushion to cover unexpected expenses or income disruptions.

Also, be aware that if your home's value decreases, you could end up owing more than your home is worth (a situation known as being "underwater" on your mortgage). This can make it difficult to sell or refinance your home in the future.

Final Thoughts

HELOC strategies can significantly impact your financial success in 2025 and beyond. You can unlock the full potential of your home's equity through debt consolidation, home improvements, and strategic investments. However, you must approach HELOCs with caution and responsibility to avoid common pitfalls such as overspending and neglecting interest rate fluctuations.

A HELOC is a financial tool that can help you achieve your goals when used wisely. You should always consider the long-term implications of your decisions, whether you consolidate high-interest debt, fund value-boosting home improvements, or explore investment opportunities. Effective HELOC strategies involve careful planning, disciplined spending, and proactive management of your credit line.

For homeowners who want to navigate the complexities of HELOCs and maximize their home equity potential, HELOC360 offers comprehensive solutions. Our platform simplifies the process, provides expert guidance, and connects you with lenders that align with your unique financial situation and goals (subject to availability). We at HELOC360 strive to empower homeowners with the knowledge and tools they need to make informed decisions about their home equity.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.