Understanding the Hidden Risks of HELOCs

Table of Contents

Home Equity Lines of Credit (HELOCs) offer homeowners a flexible way to access funds, but they come with hidden risks that many borrowers overlook.

At HELOC360, we believe it's crucial to understand these potential pitfalls before tapping into your home's equity.

This post will explore the major HELOC risks, including variable interest rates, overborrowing, and the possibility of foreclosure.

Are Variable HELOC Rates a Risk?

The Volatility of HELOC Rates

Variable interest rates define Home Equity Lines of Credit (HELOCs), but they present a double-edged sword for borrowers. These rates often start lower than fixed-rate options, but they can fluctuate dramatically over time, potentially causing financial strain.

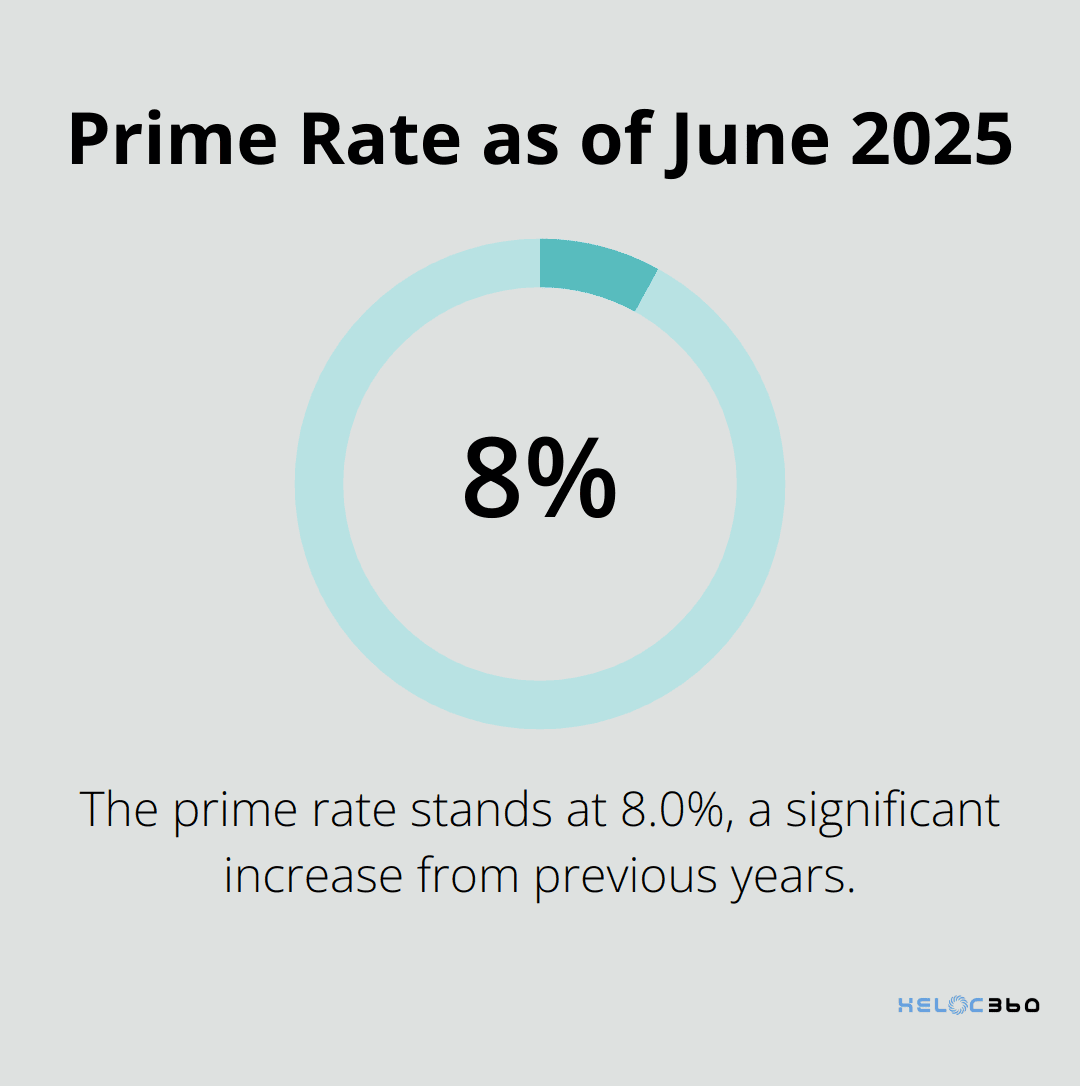

HELOC rates typically link to the prime rate, which the Federal Reserve's monetary policy influences. As of June 2025, the prime rate stands at 8.0% (a significant increase from previous years). This increase means HELOC borrowers face higher interest costs than they might have anticipated when they first opened their lines of credit.

The Impact on Your Wallet

Rising rates can substantially impact monthly payments. For example, a $100,000 HELOC balance with an interest rate that increases from 5% to 7% could see monthly payments jump by over $160. This increase can challenge borrowers who have drawn large amounts from their HELOC or live on fixed incomes.

Strategies to Protect Yourself

You can mitigate the risk of variable rates through several methods:

- Consider rate caps: Some HELOCs offer rate caps that limit how much your rate can increase over the loan's life. While these may come with slightly higher starting rates, they can provide peace of mind.

- Pay more than the minimum: Paying more than the required minimum reduces your principal faster, minimizing the impact of rate increases.

- Convert to a fixed rate: Many lenders allow you to convert all or part of your HELOC balance to a fixed-rate loan. This conversion can prove smart if you anticipate rates will continue to rise.

- Use a HELOC strategically: Instead of keeping a large balance on your HELOC long-term, use it for short-term needs and pay it off quickly to minimize exposure to rate fluctuations.

The Importance of Staying Informed

Tracking economic indicators and Federal Reserve announcements helps you anticipate potential rate changes. Financial news sources and your lender can provide valuable resources for staying informed about market trends that may affect your HELOC rate.

As we move forward, it's important to consider another significant risk associated with HELOCs: the temptation to overborrow. This risk can compound the challenges posed by variable interest rates, potentially leading to long-term financial consequences.

Why Overborrowing Poses a Major HELOC Risk

The Allure of Accessible Home Equity

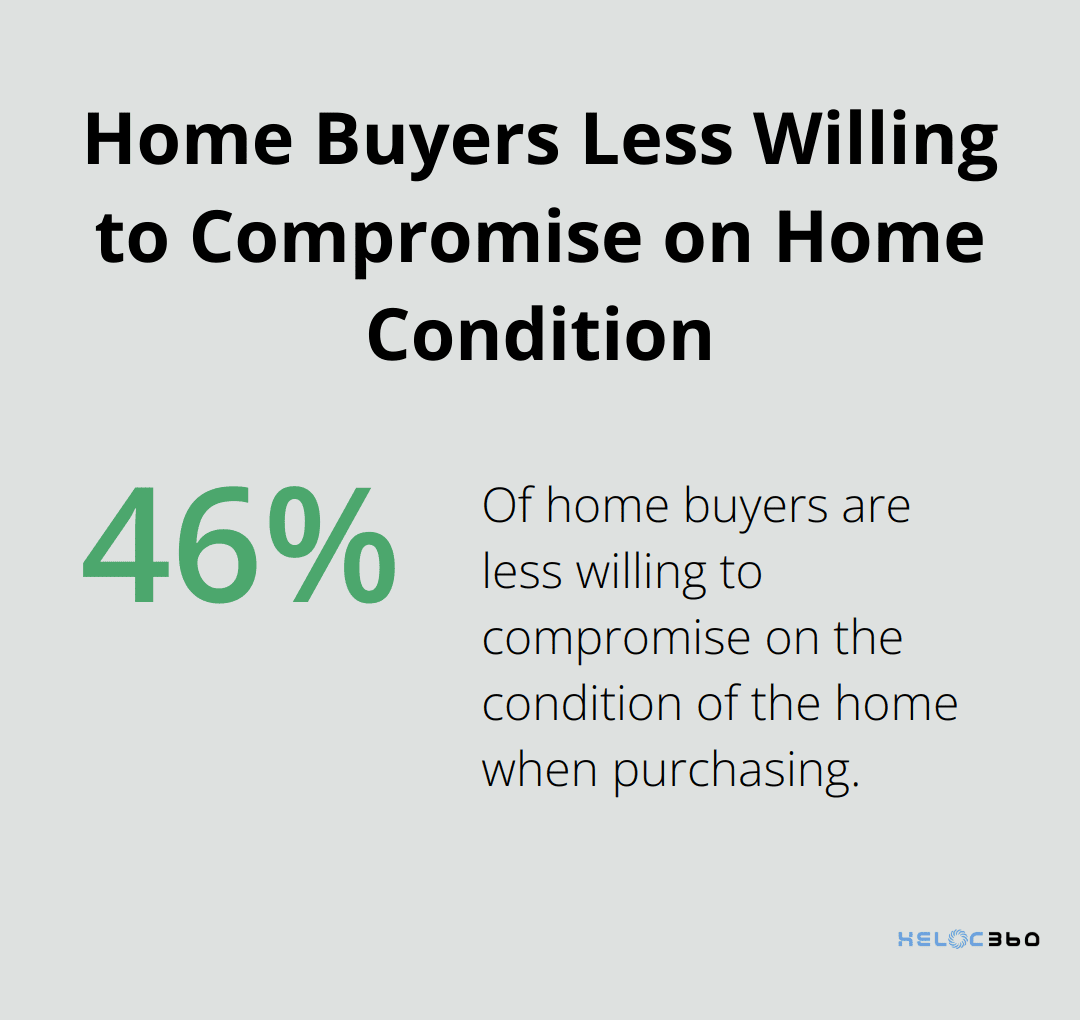

Home Equity Lines of Credit (HELOCs) offer homeowners easy access to funds, but this accessibility can lead to overborrowing. A recent survey by the National Association of Realtors reveals that 46% of home buyers are less willing to compromise on the condition of the home when purchasing. While this can be a valid use of funds, the temptation to borrow for non-essential expenses often proves too strong to resist.

The Pitfalls of Non-Essential Spending

Using a HELOC for non-essential expenses like vacations or new cars might seem harmless, but it comes with significant risks. These purchases typically don't increase your home's value, meaning you trade long-term wealth for short-term gratification.

Financial advisor Jane Doe from XYZ Financial Services cautions, "The biggest danger associated with a HELOC is the possibility of losing your home to foreclosure if you fail to meet your obligation to the debt."

Long-Term Consequences of High HELOC Balances

Maintaining high HELOC balances can have severe long-term consequences:

- Reduced Financial Flexibility: A maxed-out HELOC leaves no safety net for true emergencies.

- Increased Debt-to-Income Ratio: This can make it harder to qualify for other loans or credit in the future.

- Risk of Underwater Mortgage: Homeowners can get an underwater mortgage when home values drop and the amount of their mortgage is higher than their home's current value.

- Higher Interest Costs: The more you borrow, the more interest you'll pay over time (especially with variable rates).

Strategies to Avoid the Overborrowing Trap

To use your HELOC responsibly, follow these guidelines:

- Create a Solid Borrowing Plan: Before tapping into your HELOC, have a clear purpose and repayment strategy.

- Prioritize Value-Adding Expenses: Focus on uses that can increase your home's value or improve your financial situation.

- Avoid Lifestyle Inflation: Don't use your HELOC to finance a lifestyle beyond your means.

- Set Borrowing Limits: Establish a personal cap on how much you'll borrow (regardless of your total available credit).

- Conduct Regular Financial Check-ins: Periodically review your HELOC usage to ensure it aligns with your long-term financial goals.

The risk of overborrowing often intertwines with another significant HELOC danger: the potential for foreclosure. Understanding how these risks connect can help you make more informed decisions about using your home equity.

Can a HELOC Lead to Foreclosure?

The Collateral Nature of HELOCs

Home Equity Lines of Credit (HELOCs) offer financial flexibility, but they also carry a significant risk: the potential loss of your home. When you take out a HELOC, you use your home as collateral. This means that if you fail to make payments, the lender has the right to foreclose on your property. The Consumer Financial Protection Bureau states that foreclosures can begin after 120 days of missed payments. This timeline emphasizes the importance of staying current on your HELOC obligations.

High-Risk Scenarios

Several situations can increase your risk of HELOC-related foreclosure:

- Job Loss or Income Reduction: Unexpected unemployment or a significant pay cut can make it challenging to meet HELOC payments.

- Medical Emergencies: Healthcare debt is one of the leading causes of personal bankruptcy in the United States. These unexpected health crises can drain finances and make it difficult to keep up with HELOC payments.

- Market Downturns: If property values decline, you might end up owing more than your home is worth. This situation (known as being "underwater") can make it impossible to refinance or sell the property to pay off the HELOC.

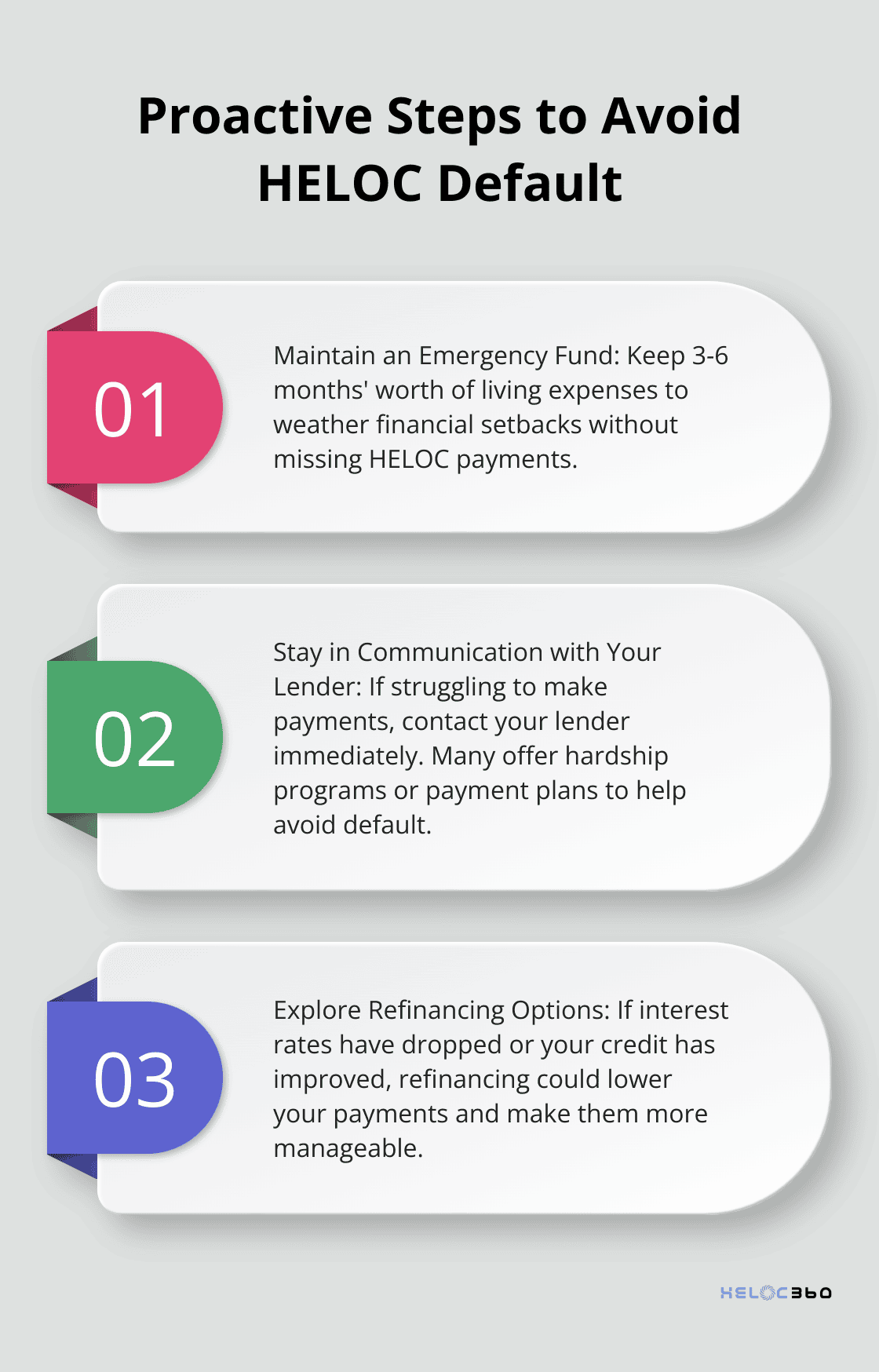

Proactive Steps to Avoid Default

The Importance of Responsible HELOC Management

Your home is more than just a financial asset - it's your sanctuary. Protect it by using your HELOC responsibly and staying vigilant about your financial health. Understanding the risks associated with HELOCs and taking proactive steps to manage your debt will significantly reduce the chances of facing foreclosure.

Final Thoughts

Home Equity Lines of Credit (HELOCs) offer homeowners a powerful financial tool, but they come with significant risks that demand careful consideration. We've explored the volatility of variable interest rates, the dangers of overborrowing, and the potential for foreclosure if payments are not maintained. Responsible borrowing is essential when it comes to HELOCs, which means having a clear purpose for the funds and a solid repayment plan.

At HELOC360, we understand these challenges and want to help homeowners navigate the complexities of home equity borrowing. Our platform empowers you with knowledge and connects you with lenders that align with your unique financial goals. We simplify the HELOC process to help you make informed decisions about leveraging your home's equity while minimizing potential risks.

Your home is not just a financial asset - it's your sanctuary. You can harness the power of your home's equity while safeguarding your financial future by approaching HELOCs with caution and staying informed about market conditions. With the right approach and tools, you can turn the equity in your home into a springboard for achieving your financial aspirations, all while managing the inherent HELOC risks responsibly.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.