Using a HELOC for Debt Consolidation: Pros and Cons

Table of Contents

Are you struggling with multiple debts and looking for a way to simplify your financial life? A HELOC for debt consolidation might be the solution you're seeking.

At HELOC360, we've seen many homeowners use this strategy to manage their finances more effectively. However, it's crucial to understand both the benefits and potential risks before making a decision.

In this post, we'll explore the pros and cons of using a Home Equity Line of Credit for debt consolidation, helping you make an informed choice about your financial future.

What's a HELOC and How Can It Help with Debt?

Understanding Home Equity Lines of Credit (HELOCs)

A Home Equity Line of Credit (HELOC) allows homeowners to borrow against the equity they've built in their property. It functions similarly to a credit card, but with your home's value as collateral. Many homeowners use HELOCs as an effective tool to manage their debt.

The Mechanics of a HELOC

When you obtain a HELOC, lenders approve you for a maximum credit limit based on your home's value and your outstanding mortgage balance. You can draw from this credit line as needed, paying interest only on the amount you use. This flexibility makes HELOCs an attractive option for various financial needs (including debt consolidation).

Debt Consolidation with a HELOC

Using a HELOC for debt consolidation involves paying off multiple high-interest debts, such as credit cards or personal loans, with the funds from your HELOC. The objective is to replace these debts with a single, lower-interest payment. According to recent data, HELOCs currently average 8.26% interest, which is the lowest level in almost two years.

The HELOC Application Process

To start, you'll need to apply for a HELOC through a lender. Once approved, you'll use the funds to pay off your existing debts. It's important to create a solid repayment plan to avoid falling back into debt.

Tapping into Your Home's Equity

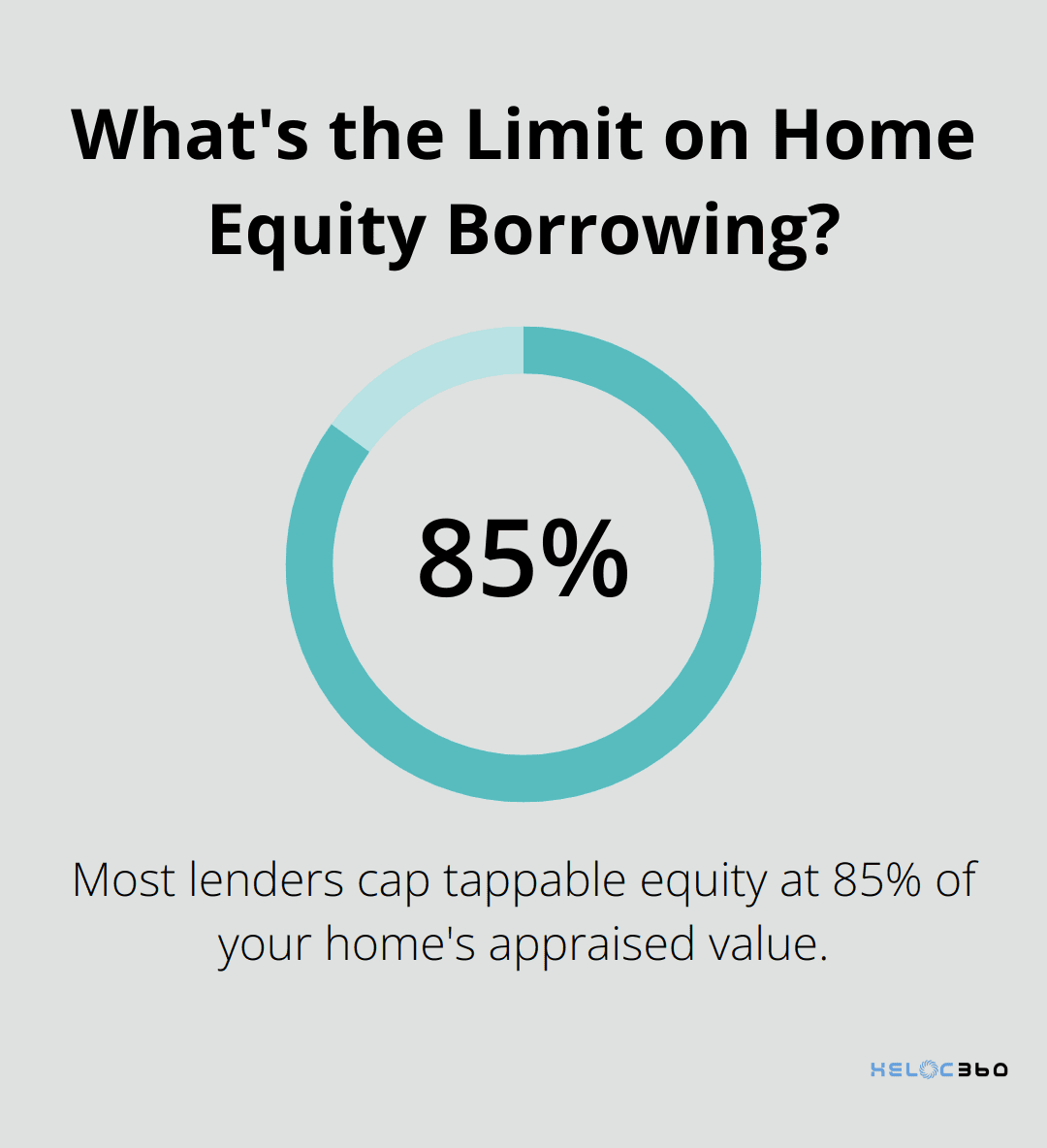

Most lenders cap tappable equity at 85% of your home's appraised value. For example, if your home is worth $300,000 and you owe $150,000 on your mortgage, you could potentially access up to $105,000 in equity (85% of $300,000 minus $150,000).

While a HELOC can be a powerful tool for debt consolidation, it's not without risks. Your home serves as collateral, so it's vital to approach this strategy with a well-thought-out financial plan. As we move forward, we'll explore the advantages of using a HELOC for debt consolidation, helping you make an informed decision that aligns with your financial goals.

Why HELOCs Are a Smart Choice for Debt Consolidation

Slash Interest Rates

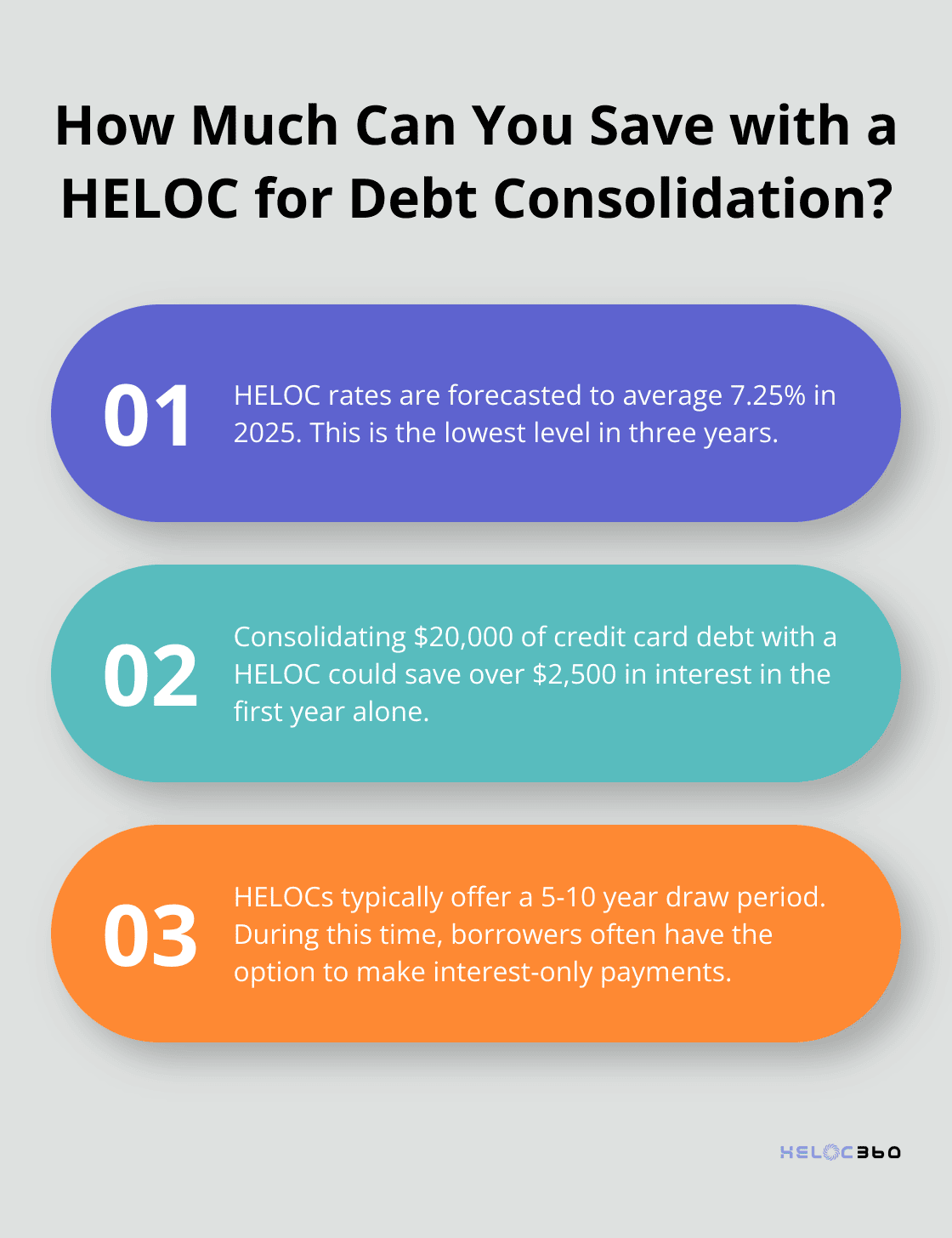

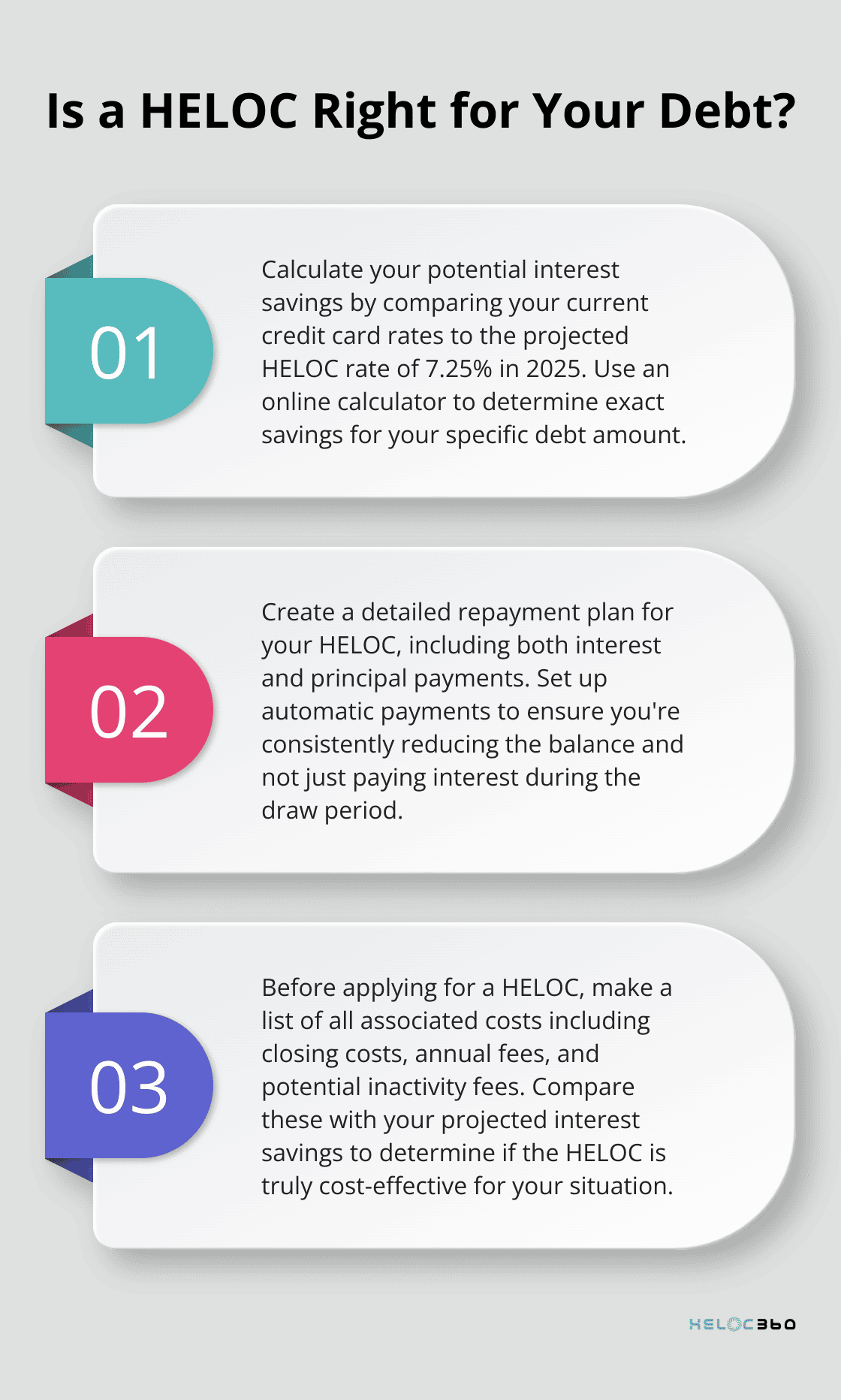

One of the most compelling reasons to use a HELOC for debt consolidation is the potential for massive interest savings. McBride forecasts that HELOC rates will continue to decline in 2025, averaging 7.25 percent, their lowest level in three years. This difference can translate into thousands of dollars saved over time. If you carry $20,000 in credit card debt, switching to a HELOC could save you over $2,500 in interest in just the first year.

Maximize Tax Advantages

The Tax Cuts and Jobs Act of 2017 limited some of the tax benefits associated with HELOCs, but potential tax advantages still exist. The interest on a home equity loan is tax-deductible, provided the funds were used to buy or build a home, or make improvements to one, as defined by the IRS. Consult with a tax professional to understand how this might apply to your specific situation and to stay updated on current tax laws.

Tailor Your Repayment Strategy

HELOCs offer unparalleled flexibility for repayment. During the draw period (which typically lasts 5-10 years), you often have the option to make interest-only payments. This can help if you experience a temporary financial squeeze. However, you should create a solid plan for paying down the principal to avoid a balloon payment at the end of the draw period.

Tap into Substantial Credit Limits

HELOCs generally provide access to larger amounts of credit compared to personal loans or credit cards. This can benefit you if you need to consolidate substantial debts. For instance, if your home is valued at $400,000 and you owe $250,000 on your mortgage, you could potentially access up to $90,000 in equity (assuming an 85% loan-to-value ratio). This larger credit line allows you to consolidate multiple high-interest debts into a single, more manageable payment.

Navigate Potential Risks

While HELOCs offer significant advantages, they also come with risks. Your home serves as collateral, which means you could lose it if you default on payments. Additionally, HELOCs have variable interest rates that can change for borrowers each month. It's essential to approach this strategy with a clear understanding of your financial situation and a solid plan for repayment.

As you weigh the benefits and potential risks of using a HELOC for debt consolidation, it's important to consider the potential drawbacks in more detail. Let's explore some of the challenges you might face when using this financial tool.

What Are the Hidden Risks of HELOC Debt Consolidation?

The Foreclosure Factor

When you use a HELOC, you put your home on the line. If you default on payments, you risk losing your house to foreclosure. This is a serious consideration, especially if you consolidate unsecured debts like credit card balances. RealtyTrac reports that foreclosure filings totaled 130,786 last month. While this number may seem relatively low, it highlights the real risk involved in using your home as collateral.

The Interest Rate Rollercoaster

HELOCs typically come with variable interest rates, which fluctuate based on market conditions. While rates are currently favorable, they can increase over time, potentially making your monthly payments less affordable. The Federal Reserve projects potential rate hikes in the coming years, which could directly impact HELOC rates. You must factor in this uncertainty when you plan your long-term financial strategy.

The Spending Trap

One often overlooked risk of using a HELOC for debt consolidation is the temptation to overspend. With access to a large line of credit, some homeowners accumulate new debt alongside their consolidated balance. A report from the Federal Reserve Bank of New York found that balances on home equity lines of credit (HELOC) rose by $7 billion, marking the tenth consecutive quarterly increase after 2022Q1, with a total of $387 billion in outstanding balances. To avoid this trap, you must address the root causes of your debt and develop a solid financial plan.

The Hidden Costs

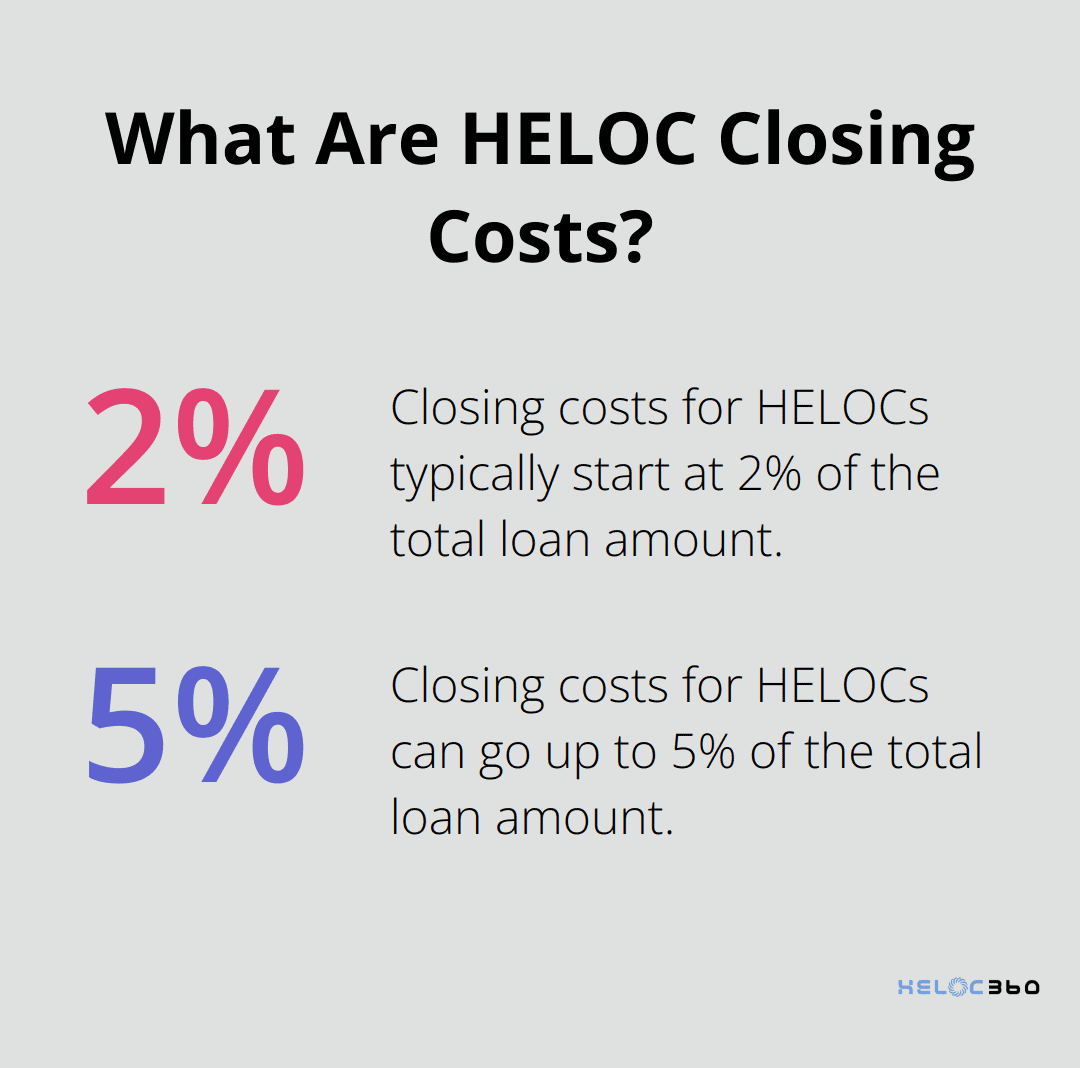

While HELOCs often boast lower interest rates than credit cards, they come with their own set of costs. Closing costs typically range from 2% to 5% of the total loan amount. For a $100,000 HELOC, that's $2,000 to $5,000 in upfront expenses. Additionally, some lenders charge annual fees or inactivity fees. These costs can eat into the potential savings from debt consolidation, so you should calculate the total cost of borrowing before you proceed.

The Equity Erosion Risk

Using a HELOC for debt consolidation can reduce your home equity. This reduction might limit your future borrowing options or affect your ability to sell your home profitably. You should consider your long-term financial goals and how a HELOC might impact your overall financial picture (including your retirement plans and potential need for future home equity loans).

Final Thoughts

A HELOC for debt consolidation offers potential benefits like lower interest rates and flexible repayment options. However, it also comes with risks such as foreclosure and variable rates. You must carefully assess your financial situation and create a solid repayment plan before using this strategy.

Financial planning plays a vital role when considering a HELOC for debt consolidation. You should evaluate your current debts, understand your income and expenses, and create a realistic budget. It's also important to address the root causes of your debt to prevent future financial troubles.

At HELOC360, we provide homeowners with tools and knowledge to make informed decisions about their financial future. Our platform connects you with lenders that fit your unique needs, helping you unlock the full potential of your home equity. Take time to weigh your options and consider the long-term implications before proceeding with a HELOC for debt consolidation.

Related Articles

When Is the Right Time to Consider a HELOC?

Optimize your HELOC timing to enhance your financial position. Learn key market trends and personal indicators for securing a Home Equity Line of Credit.

Equity Line vs Equity Loan: Making the Right Choice

Explore the key differences between equity line vs equity loan and find the best fit for your financial needs by comparing flexibility, rates, and benefits.

Is a HELOC the Secret to Smart Debt Consolidation?

Explore how HELOC consolidation can simplify your finances and reduce debt. Learn practical tips and trends in smart debt management.