Best HELOC Rates Today [Daily Updates]

![Best HELOC Rates Today [Daily Updates]](/_next/image?url=https%3A%2F%2Fcdn.sanity.io%2Fimages%2F2a445j5i%2Fproduction%2F1849ded7af792ffcb6078bd330318598d7c38b78-1024x585.jpg%3Fauto%3Dformat&w=3840&q=75)

Table of Contents

At HELOC360, we understand the importance of finding the best HELOC rates in today's dynamic market.

Our daily updates provide you with the most current information on national averages and top lender offers.

In this post, we'll explore the factors influencing HELOC rates and share practical tips to help you secure the most competitive terms.

Whether you're a homeowner or investor, stay informed to make the best financial decisions for your unique situation.

What Are Today's Best HELOC Rates?

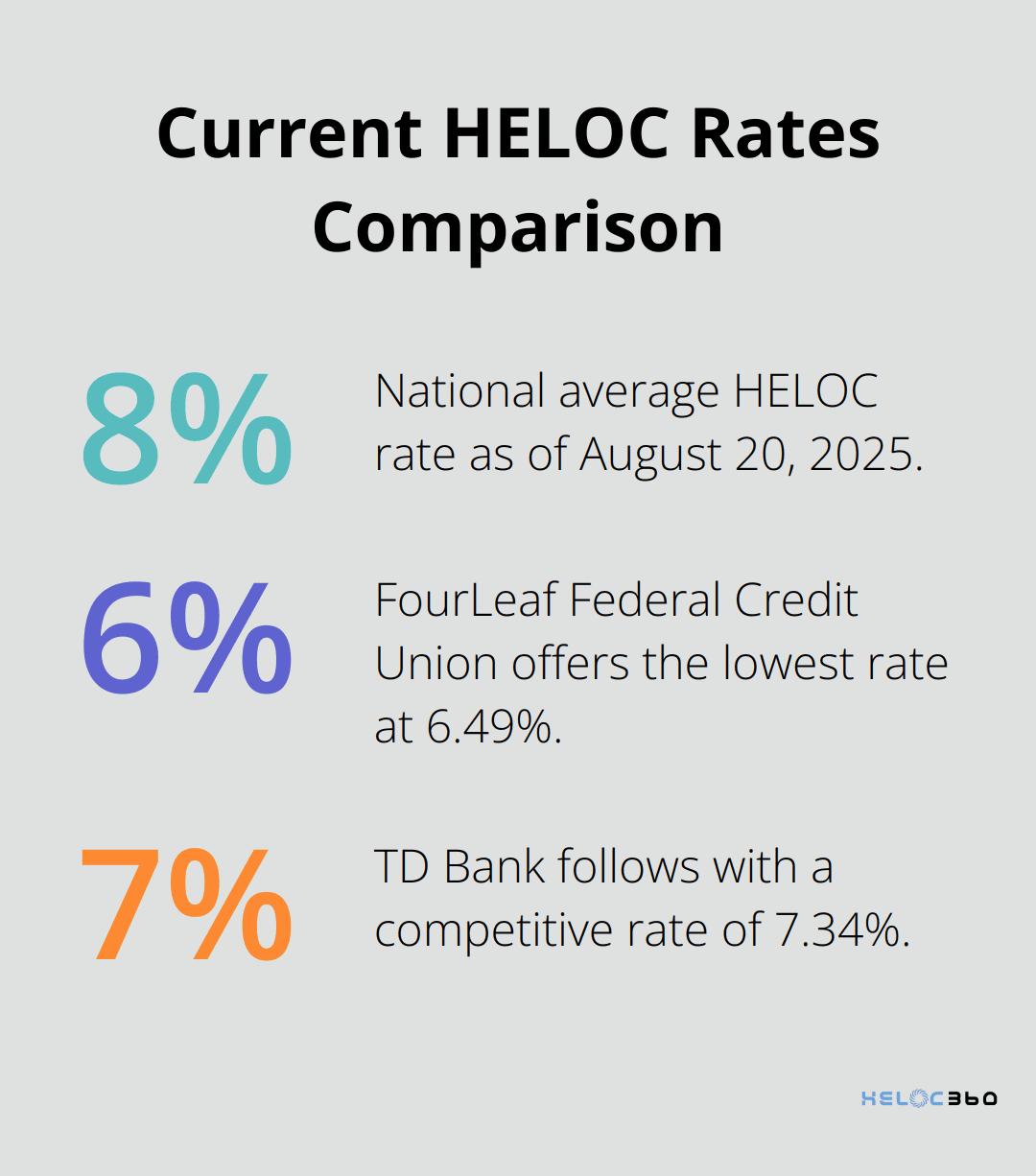

Current National Average

As of August 20, 2025, the national average HELOC interest rate is 8.12%, according to Bankrate's latest survey of the nation's largest home equity lenders. This figure serves as a benchmark, but it doesn't tell the complete story of the HELOC market.

Top Lenders Offering Competitive Rates

We've analyzed the market to find the most attractive rates available. Currently, FourLeaf Federal Credit Union leads with a rate of 6.49%, while TD Bank follows at 7.34%. These rates highlight the importance of comparing multiple lenders, as they sit significantly below the national average.

Factors Influencing Today's HELOC Rates

Several key elements shape current HELOC rates:

- Federal Reserve Policy: Recent Fed decisions have impacted HELOC rates. While HELOC rates move with Fed cuts, not every borrower will see lower payments immediately.

- Economic Indicators: Inflation rates and overall economic health significantly impact HELOC rates. Monitoring these indicators can help you anticipate potential rate changes.

- Personal Financial Profile: Your individual circumstances greatly affect the rate you'll receive. Your credit score, home equity, and debt-to-income ratio all play critical roles in determining your offered rate.

Interpreting HELOC Rates

It's important to understand that the rates mentioned represent a snapshot of the market. HELOC rates can vary widely based on factors like loan amount, credit score, and loan-to-value ratio. For example, a $50,000 HELOC with an 8.28% interest rate might result in monthly payments around $530 (depending on specific terms).

We always recommend obtaining personalized quotes from multiple lenders. This approach ensures you're not just pursuing the lowest advertised rate, but finding the best overall deal for your unique situation.

Future Rate Projections

Curinos forecasts a robust 14–17% increase in home equity originations for 2025 compared with 2024, fueled in part by exceptional growth. This projection underscores the potential benefits of timing your HELOC application strategically. By staying informed about market trends and economic indicators, you can position yourself to secure more favorable rates.

As we move forward, let's explore how you can actively improve your chances of securing the best possible HELOC rate for your financial needs.

How to Secure the Best HELOC Rate

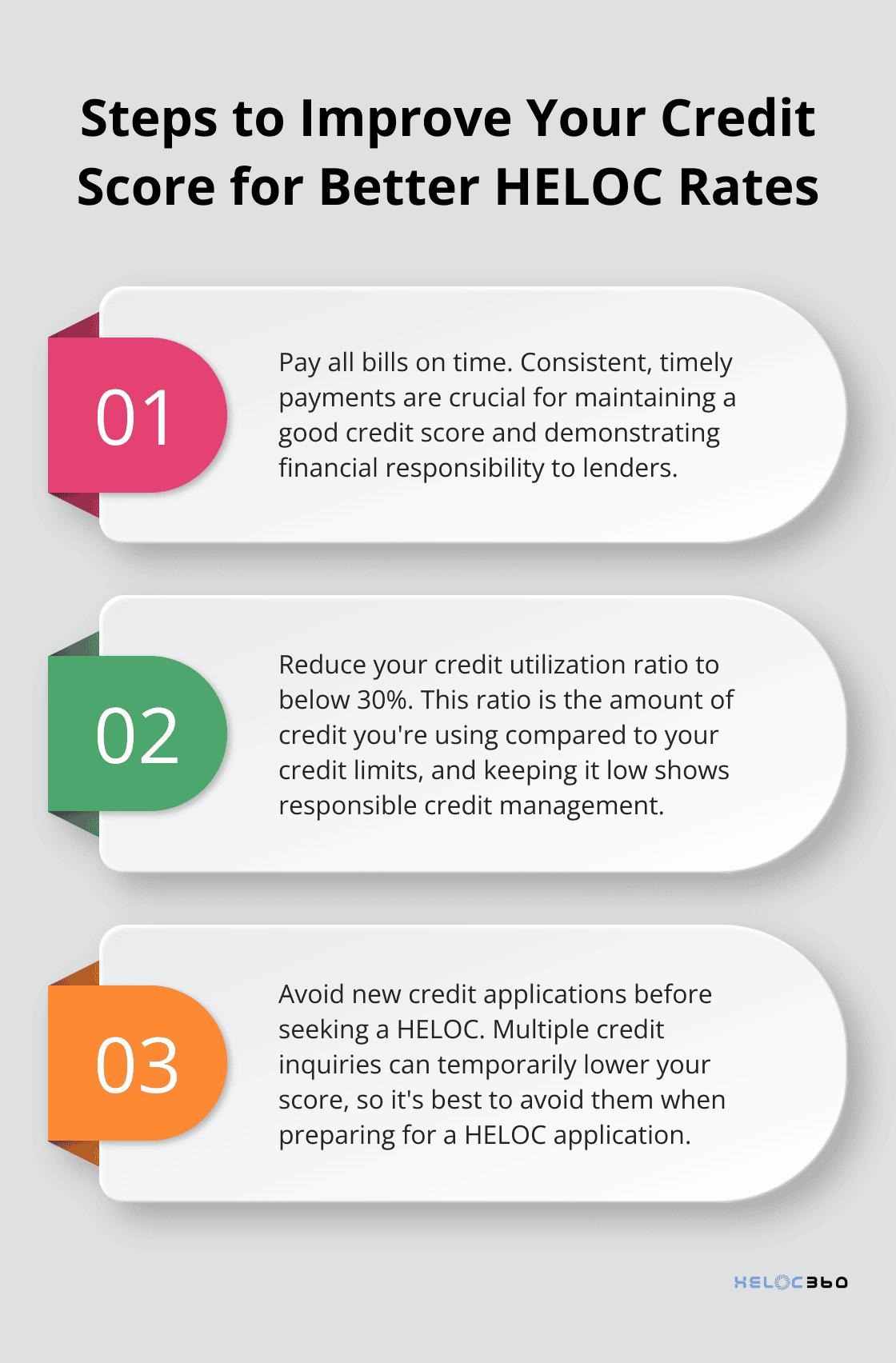

Improve Your Credit Score

Your credit score plays a pivotal role in determining your HELOC rate. Lenders use this three-digit number to assess your creditworthiness. A credit score of at least 680 can help you qualify for better rates, with some lenders preferring 720 or higher. To enhance your score:

Increase Your Home Equity

Lenders typically prefer a combined loan-to-value ratio (CLTV) below 85%. This means the total of your mortgage balance and desired HELOC amount should not exceed 85% of your home's current value. To boost your equity:

- Make extra mortgage payments when possible

- Complete value-adding home improvements

- Wait for natural market appreciation in your area

Shop Around for the Best Offers

Don't accept the first offer you receive. Compare multiple lenders to find significant savings. A study by Freddie Mac revealed that homebuyers can potentially save $600–$1200 annually by applying for mortgages from multiple lenders.

Explore Fixed-Rate Options

While HELOCs traditionally come with variable rates, some lenders offer fixed-rate options or the ability to convert a portion of your balance to a fixed rate. This can provide stability in a rising rate environment. For example, some banks (like Bank of America) offer a fixed-rate option on their HELOCs, allowing borrowers to lock in a portion of their line at a set rate.

Negotiate Terms and Fees

Many borrowers don't realize that HELOC terms are often negotiable. Ask about waiving annual fees, reducing closing costs, or lowering the interest rate. Some lenders may match or beat a competitor's offer to earn your business.

The strategies outlined above will position you well to secure a HELOC with favorable terms. Your preparation efforts can translate into thousands of dollars saved over the life of your HELOC. (This financial impact underscores the importance of thorough research and negotiation.)

As you work towards securing the best HELOC rate, it's essential to understand the various rate structures available. Let's examine how different HELOC rate structures can affect your borrowing experience and long-term costs.

How HELOC Rate Structures Work

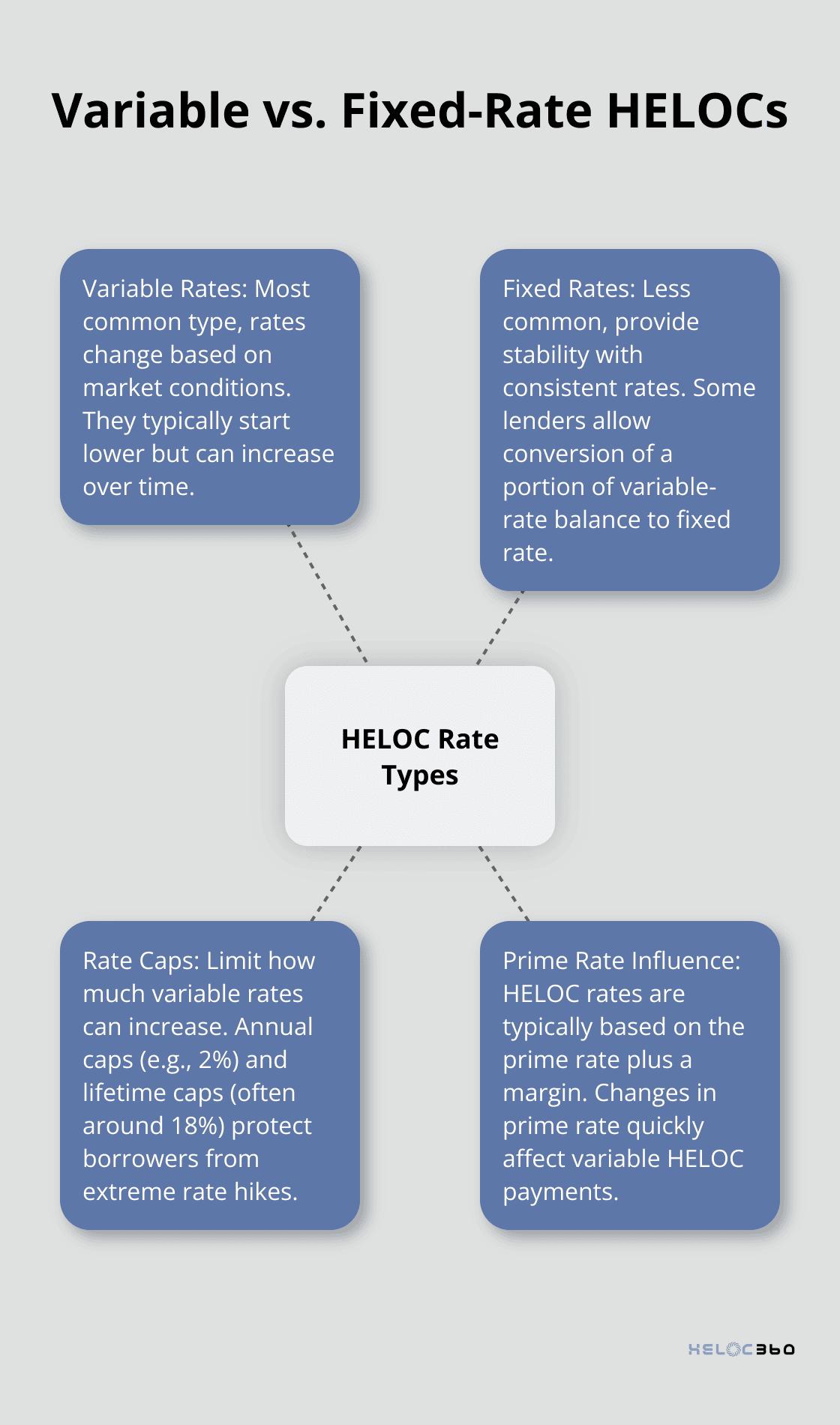

Variable vs. Fixed-Rate HELOCs

Most HELOCs offer variable rates that change based on market conditions. These rates typically start lower than fixed-rate options but can increase over time if market conditions result in higher rates.

Fixed-rate HELOCs provide stability but are less common. Some lenders allow conversion of a portion of your variable-rate balance to a fixed rate, offering a balance between flexibility and predictability.

The Prime Rate's Influence

The prime rate, set by major banks, forms the foundation for HELOC rates. Lenders typically add a margin to the prime rate to determine your HELOC rate. As of August 2025, with a prime rate of 5.5%, a lender might offer a HELOC at prime + 2%, resulting in a 7.5% rate.

Prime rate changes can quickly affect your HELOC payments. Current HELOC borrowers can expect their interest rate and payments to adjust within a month or two after a Fed rate change.

Safeguards: Rate Caps and Floors

Rate caps limit how much your HELOC rate can increase over time. A 2% annual cap means your rate won't go up by more than 2 percentage points in a year, regardless of market conditions. Lifetime caps, often around 18%, set the maximum rate you'll ever pay.

Rate floors set the minimum rate. Even if the prime rate drops significantly, your HELOC rate won't fall below this floor. Ask potential lenders about their cap and floor policies to understand your long-term cost boundaries.

Navigating Introductory Rates

Many lenders offer tempting introductory rates, sometimes as low as 1–2% for the first 6–12 months. While these can provide initial savings, it's important to understand the rate after the promotional period ends.

Always factor in the long-term rate when budgeting for a HELOC to avoid payment shock when the introductory period ends.

Final Thoughts

The HELOC market offers significant opportunities for informed borrowers. Today's best HELOC rates, such as FourLeaf Federal Credit Union's 6.49% and TD Bank's 7.34%, highlight potential savings compared to the 8.12% national average. These figures emphasize the importance of thorough research and comparison when seeking the best HELOC rates.

Securing a competitive rate requires focus on credit score improvement, home equity increase, and extensive lender comparison. Negotiation of terms and fees can lead to substantial long-term savings. Understanding rate structures, prime rate impact, and rate cap benefits will empower you to make informed borrowing decisions.

We at HELOC360 commit to helping homeowners maximize their home equity potential. Our platform provides expert guidance and connects you with lenders that align with your financial goals. For tailored HELOC solutions, visit our comprehensive platform to unlock your home's equity and achieve your financial aspirations.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.