How to Negotiate the Best HELOC Terms Like a Pro

Table of Contents

Securing the best terms for your Home Equity Line of Credit (HELOC) can save you thousands of dollars over time.

At HELOC360, we know that HELOC negotiation is a skill that can be learned and mastered.

This guide will equip you with the knowledge and strategies to negotiate like a pro, ensuring you get the most favorable HELOC terms possible.

Understanding HELOC Basics

What Is a HELOC?

A Home Equity Line of Credit (HELOC) is a financial tool that allows homeowners to borrow against the equity in their property. It functions as a revolving credit line, similar to a credit card, but uses your home as collateral.

How HELOCs Work

When you open a HELOC, the lender provides you with a credit limit based on your home's value and your outstanding mortgage balance. The HELOC lifecycle consists of two main phases:

- Draw Period (typically 5-10 years): You can borrow up to your credit limit as needed. You only pay interest on the amount you borrow, not the entire credit line.

- Repayment Phase: After the draw period ends, you can no longer borrow and must repay the outstanding balance (usually over 10-20 years).

Some lenders offer interest-only payments during the draw period. However, this option can lead to a significant payment increase when full repayment begins.

Key HELOC Terms

Interest rates for HELOCs are usually variable, tied to the prime rate plus a margin. As of June 18, 2025, the national average HELOC rate stands at 8.27%.

The loan-to-value (LTV) ratio plays a critical role in HELOC approval. Lenders typically set limits for how high your LTV ratio can be. For example, if your home is worth $300,000, your total borrowing (mortgage plus HELOC) shouldn't exceed a certain percentage of that value.

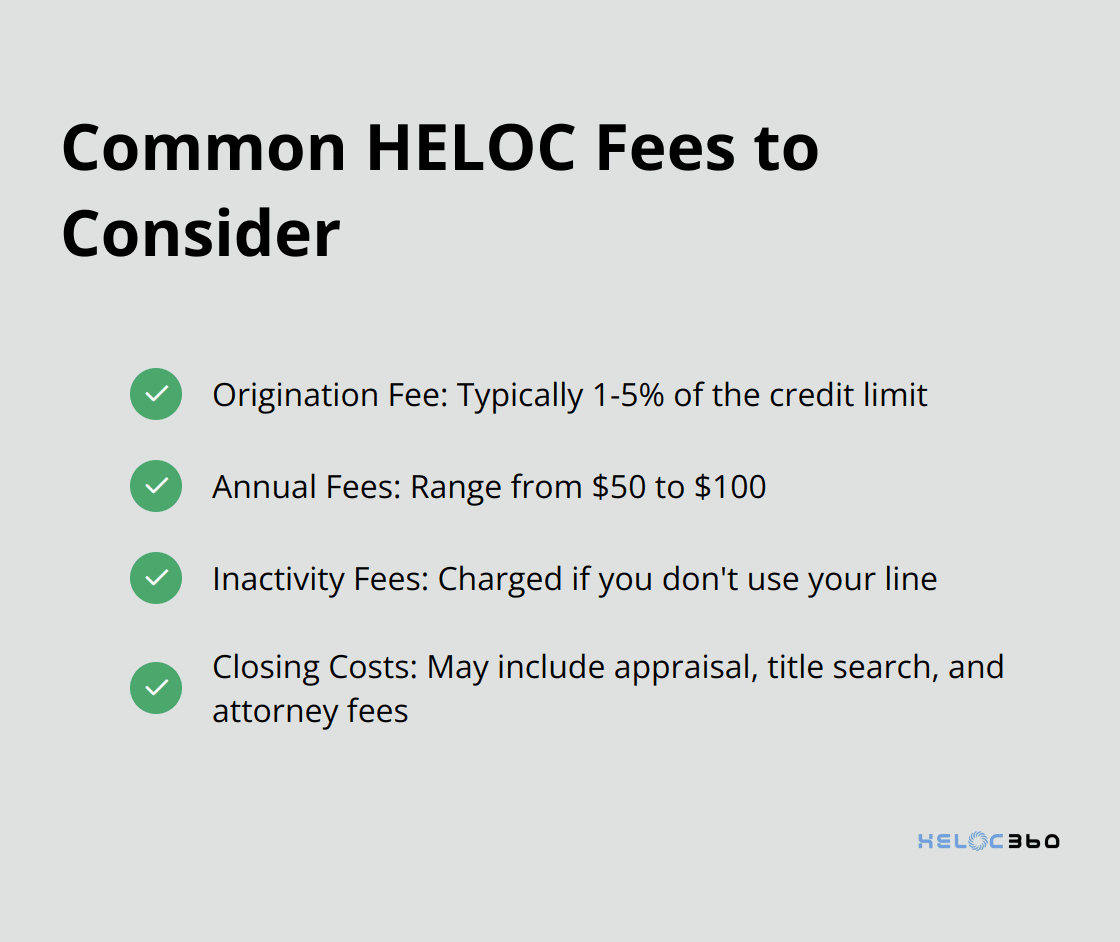

Common HELOC Fees

While HELOCs can offer cost-effective borrowing, they come with various fees:

- Origination Fee: Typically 1-5% of the credit limit

- Annual Fees: Range from $50 to $100

- Inactivity Fees: Some lenders charge if you don't use your line

- Closing Costs: May include appraisal fees, title search, and attorney fees

Home equity loan and HELOC closing costs and fees vary, depending on the lender, and can range from 1-5% of the total loan amount.

Some lenders waive closing costs but may charge a cancellation fee if you close the HELOC within a certain period (usually 3-5 years).

Understanding these basics forms the foundation for negotiating better HELOC terms. As you prepare to explore HELOC options, it's essential to research current rates and assess your financial situation. This knowledge will empower you to make informed decisions and potentially save thousands over the life of your loan.

How to Prepare for HELOC Negotiations

Research Current HELOC Rates

Effective HELOC negotiations start with thorough preparation. You should research current HELOC rates from various lenders. As of June 2025, HELOC interest rates dropped by 1.29 percentage points between January 2024 and January 2025 (from 8.92% to 7.63%). However, rates can vary significantly between lenders and based on your financial profile.

Use online comparison tools to get a sense of the rate range you might qualify for. Don't just look at the advertised rates - pay attention to the annual percentage rate (APR), which includes fees and gives a more accurate picture of the total cost.

Assess Your Financial Health

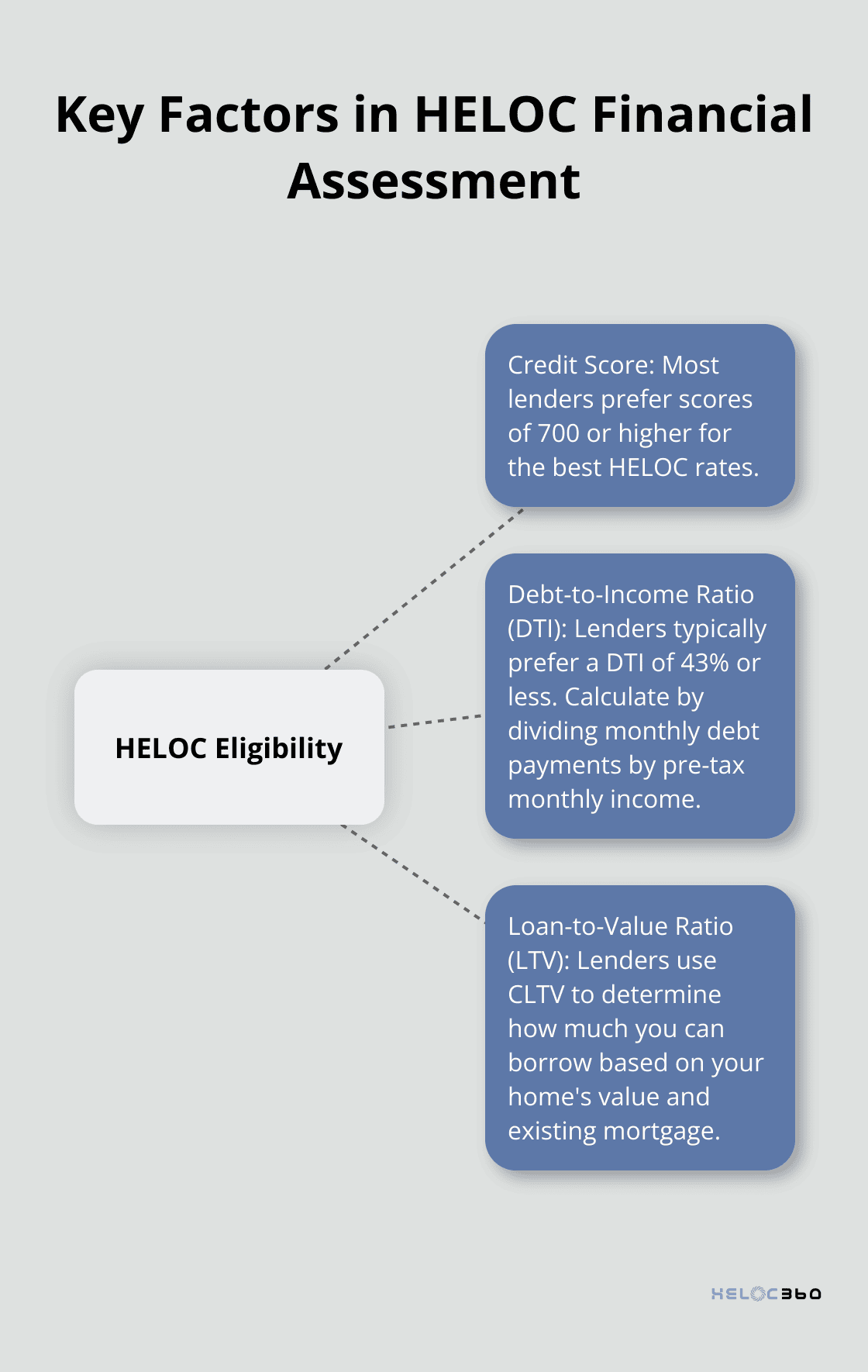

Your financial situation plays a crucial role in the terms you'll be offered. Start by checking your credit score - most lenders prefer scores of 700 or higher for the best HELOC rates. If your score is lower, consider taking steps to improve it before applying.

Next, calculate your debt-to-income (DTI) ratio. To calculate your DTI, add up your monthly debt payments, divide that number by your pre-tax monthly income, and multiply by 100. Most lenders prefer a DTI of 43% or less. If yours is higher, focus on paying down existing debts before applying for a HELOC.

Also, determine your home's current value and your existing mortgage balance. This will help you calculate your loan-to-value (LTV) ratio, which lenders use to determine how much you can borrow. Most lenders use your combined-loan-to-value ratio, or CLTV, to decide if you have enough equity for a HELOC.

Compile Necessary Documentation

Lenders will require various documents to verify your financial situation. Having these ready can speed up the process and demonstrate your preparedness. Typically, you'll need:

- Proof of income: Recent pay stubs, W-2 forms, or tax returns if self-employed

- Property information: Your most recent mortgage statement and property tax bill

- Asset documentation: Bank statements and investment account statements

- Debt information: Statements for any outstanding loans or credit card balances

Some lenders might also require a recent home appraisal. Check if you can use a recent appraisal or if the lender will require a new one.

Understand HELOC Terms and Fees

Before you start negotiations, familiarize yourself with common HELOC terms and fees. This knowledge will help you ask the right questions and identify areas for potential negotiation. Key terms to understand include:

- Draw period length

- Repayment period

- Interest rate structure (variable vs. fixed)

- Rate caps

- Prepayment penalties

Common fees to watch out for include origination fees (typically 1-5% of the credit limit), annual fees ($50-$100), and closing costs. Some lenders waive certain fees, so this can be a point of negotiation.

Armed with this knowledge and preparation, you're ready to start comparing offers from different lenders. In the next section, we'll explore strategies to negotiate the best possible terms for your HELOC. If you're considering alternatives or need to modify your existing HELOC, it's important to understand all your options.

How to Negotiate Your HELOC Like a Pro

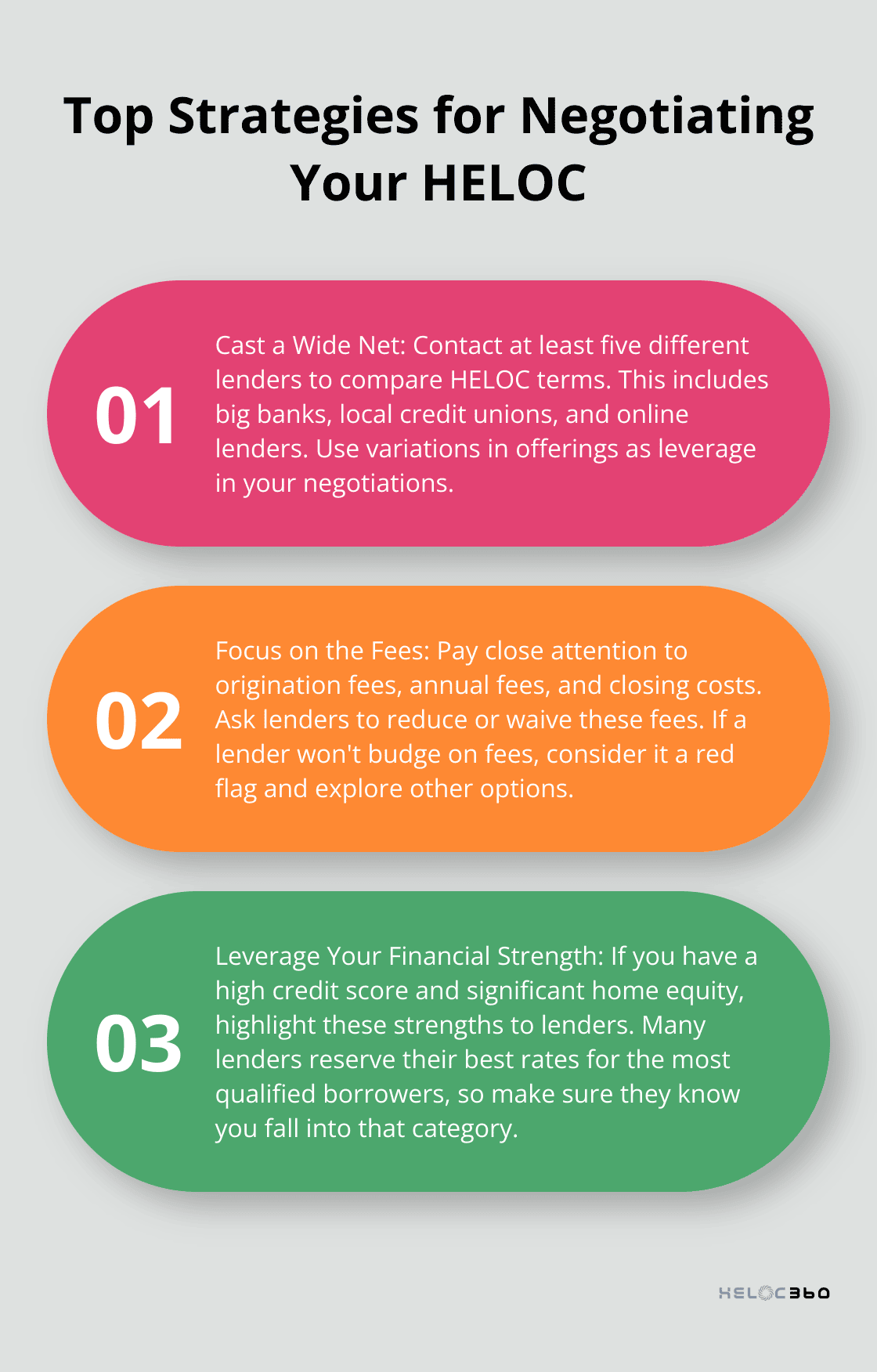

Cast a Wide Net

Contact at least five different lenders to compare their HELOC terms. This includes big banks, local credit unions, and online lenders. Each will have different offerings, and you can use these variations as leverage in your negotiations.

If Bank A offers you a 7.5% interest rate, but Credit Union B offers 7.2%, go back to Bank A and ask them to match or beat that rate. Many lenders will compete for your business, especially if you have a strong credit profile.

Focus on the Fees

HELOC fees can add up quickly. When negotiating, pay close attention to origination fees, annual fees, and closing costs. You can often reduce or waive these entirely if you ask.

For instance, if a lender charges a $500 origination fee, ask if they can waive it. If they won't waive it completely, try to negotiate it down. Everything is negotiable. If a lender won't budge on fees, consider it a red flag and explore other options.

Negotiate Beyond the Interest Rate

While the interest rate is important, don't forget about other terms that can impact your HELOC's cost and flexibility. Negotiate for a longer draw period if you need more time to access funds. Ask about the possibility of converting a portion of your balance to a fixed rate during the repayment period for more predictable payments.

Some lenders offer rate discounts for setting up automatic payments or maintaining a certain balance in a linked checking account. Ask about these options to potentially lower your rate further.

Leverage Your Financial Strength

If you have a high credit score and significant home equity, you're in a strong position to negotiate. Don't hesitate to highlight these strengths to lenders.

You might say, "I see you're offering a rate of 7.5%, but given my high credit score and substantial equity in my home, I believe I should qualify for your best rate. Can you do better?" Many lenders reserve their best rates for the most qualified borrowers, so make sure they know you fall into that category.

Time Your Application Strategically

The HELOC market can be seasonal. Many lenders offer special promotions in the spring and fall when home improvement projects are common. Try to time your application to coincide with these promotions to secure better terms.

Additionally, keep an eye on broader economic trends. If experts expect the Federal Reserve to lower interest rates soon, it might benefit you to wait a few months before locking in your HELOC terms.

Negotiating your HELOC terms is not just about getting the lowest rate – it's about finding the best overall package that suits your financial needs (including factors like flexibility and long-term costs). These strategies can help you secure a HELOC that truly works for you. Remember, if you're planning a complete home remodel, having the entire budget available upfront can help you negotiate better deals with contractors.

Final Thoughts

HELOC negotiation requires strategic preparation and a thorough understanding of current rates, your financial health, and HELOC terms. You should focus on fees, leverage your financial strengths, and consider the entire package beyond just the interest rate. The timing of your application can also impact the terms you receive, potentially saving you thousands over the life of your HELOC.

HELOC360 simplifies the process of finding and comparing HELOC offers. We provide the knowledge and tools you need to make informed decisions about your home equity. Our platform connects you with lenders that match your specific needs, helping you unlock the full potential of your home's value.

With the right approach and support, you can turn your home equity into a powerful financial tool. HELOC360 empowers you to secure terms that align with your financial goals (whether funding home improvements, consolidating debt, or creating financial flexibility). You can approach HELOC negotiations with confidence using the strategies outlined in this guide and the resources available through our platform.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.