HELOC vs Cash-Out Refinance Which Wins in 2025?

Table of Contents

Homeowners often face a crucial decision when tapping into their home equity: HELOC or cash-out refinance?

At HELOC360, we understand the importance of making the right choice for your financial future. This HELOC comparison will help you navigate the pros and cons of each option in 2025.

Let's explore which method might be the best fit for your unique situation and goals.

What Are HELOCs and Cash-Out Refinances?

HELOCs: Your Home as a Credit Card

A Home Equity Line of Credit (HELOC) functions like a credit card secured by your home. Lenders approve you for a credit limit based on your home's equity. During the draw period (typically 10 years), you can borrow as needed. The key advantage? You only pay interest on the amount you borrow, not the entire credit line.

HELOCs offer flexibility for various purposes (home improvements, debt consolidation, etc.). However, they usually come with variable interest rates, which can lead to fluctuating payments over time. Rates may continue dropping in 2025, as HELOCs tend to have variable interest rates that automatically change based on the prime rate.

Cash-Out Refinances: A New Mortgage with Extra Cash

A cash-out refinance replaces your existing mortgage with a new, larger loan. You receive the difference between your new loan amount and your current mortgage balance in cash. This option often provides fixed interest rates, resulting in more predictable monthly payments.

Cash-out refinances can benefit homeowners who need a large lump sum or want to take advantage of lower interest rates than their existing mortgage. They offer benefits like access to money at potentially a lower interest rate, plus tax deductions if you itemize. However, they typically involve closing costs and may extend your loan term.

How to Tap Into Your Home's Equity

Both HELOCs and cash-out refinances allow you to access your home's equity, but through different methods:

- HELOCs create a second mortgage

- Cash-out refinances modify your primary mortgage

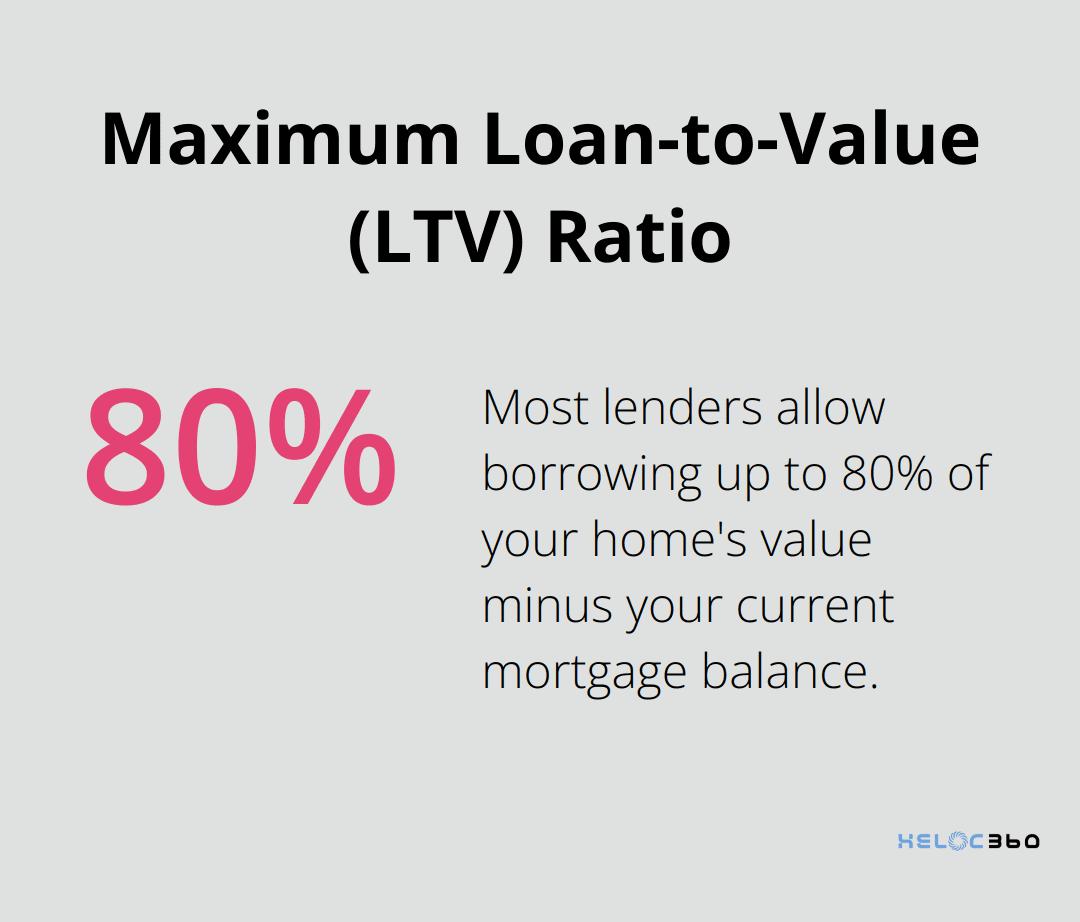

The amount you can borrow depends on your home's value and your existing mortgage balance. Most lenders allow borrowing up to 80-85% of your home's value minus your current mortgage balance.

For example:

- Home value: $250,000

- Current mortgage balance: $150,000

- Maximum LTV: 0.8 or 80%

Real-World Applications

Homeowners use these financial tools for various purposes:

- Home Renovations: A HELOC can fund a kitchen remodel, potentially increasing your home's value.

- Debt Consolidation: A cash-out refinance might help consolidate high-interest credit card debt, potentially saving thousands in interest over time.

The Importance of a Solid Repayment Plan

Both options use your home as collateral, so it's essential to have a robust repayment strategy. Consider your financial goals, current interest rates, and long-term plans before deciding which option suits you best.

As we move forward, let's compare HELOCs and cash-out refinances in more detail to help you make an informed decision in 2025.

How Do HELOCs and Cash-Out Refinances Compare in 2025?

Interest Rates and Payment Structures

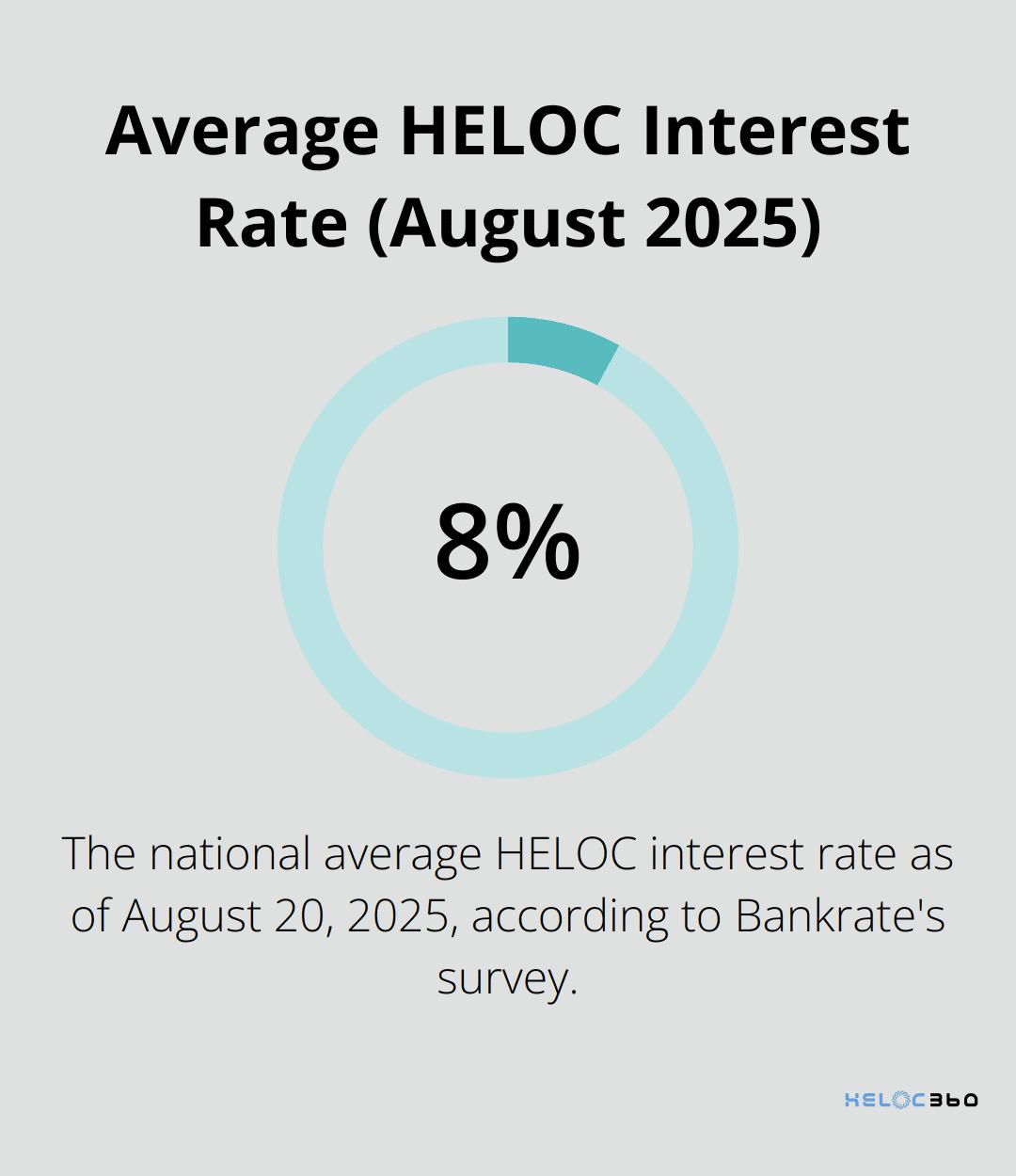

In 2025, HELOCs and cash-out refinances offer distinct interest rate structures. HELOCs typically feature variable rates, with the national average HELOC interest rate at 8.12% as of August 20, 2025, according to Bankrate's latest survey of the nation's largest home equity lenders.

HELOCs usually include a 10-year draw period where borrowers pay interest only on borrowed amounts. This period transitions into a repayment phase (often 10-20 years) where both principal and interest payments apply. This structure can lead to significant payment increases if not anticipated.

Cash-out refinances offer consistent monthly payments throughout the loan term (typically 15 or 30 years). This predictability appeals to those who prefer stable budgeting.

Flexibility and Fund Access

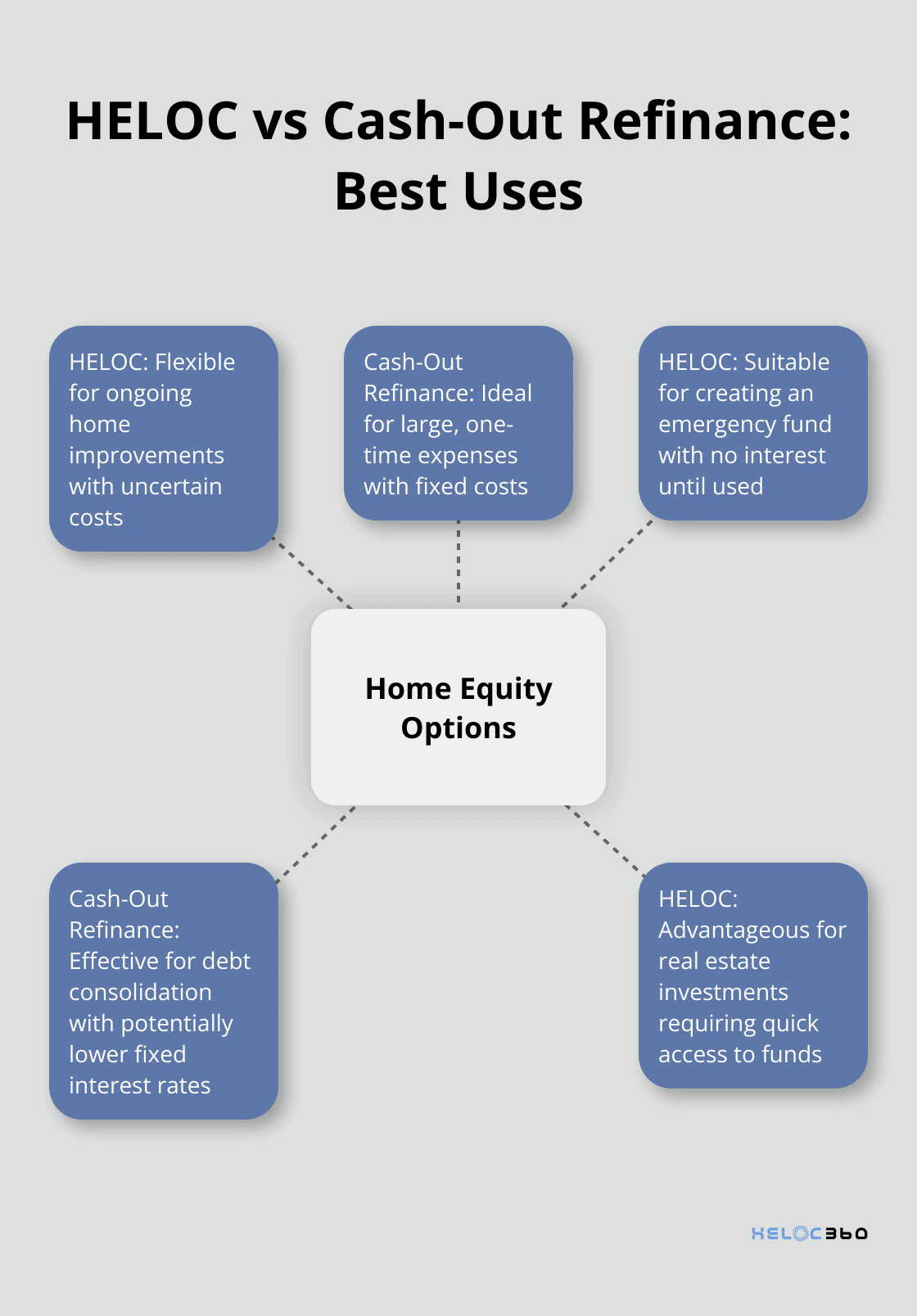

HELOCs excel in flexibility. Borrowers can draw funds as needed, repay, and re-borrow during the draw period. This makes HELOCs suitable for ongoing expenses or projects with uncertain costs.

Cash-out refinancing replaces your current mortgage with a new, larger loan. While ideal for large, one-time expenses, they lack flexibility for changing financial needs. Interest accrues on the entire amount from day one, regardless of immediate fund utilization.

Credit Score and Debt-to-Income Effects

Both options impact credit differently. HELOCs, as revolving credit lines, can cause short-term credit score fluctuations as utilization changes. Cash-out refinances, being installment loans, may initially lower credit scores due to hard inquiries and new accounts, but consistent payments can improve scores over time.

Regarding debt-to-income (DTI) ratios, cash-out refinances often allow higher DTIs (up to 50% in some cases). HELOCs typically require a DTI of 43% or lower. (These figures may vary based on individual lender policies.)

Tax Implications and Deductions

The Tax Cuts and Jobs Act of 2017 altered home equity borrowing rules. For tax years 2018 through 2025, interest deductibility now applies only when funds buy, build, or substantially improve the securing home.

For cash-out refinances, the entire interest amount may qualify for deduction if used for home improvements (within the $750,000 new mortgage cap). HELOC interest deductions apply only to portions used for home improvements, subject to the same $750,000 limit.

Detailed record-keeping of fund usage maximizes potential tax benefits. (Tax laws can change, and individual situations vary. Consult a tax professional for personalized advice.)

As we explore these options, it's essential to consider how they align with specific financial goals and scenarios. Let's examine situations where HELOCs or cash-out refinances might prove more advantageous.

When Should You Choose a HELOC or Cash-Out Refinance?

Home Improvements and Renovations

HELOCs often outperform cash-out refinances for home improvements. Their flexibility allows borrowing as needed, which suits projects with uncertain costs. You pay interest only on the amount you use, potentially reducing expenses compared to a lump-sum cash-out refinance.

A HELOC excels for ongoing renovations. For example, when updating your kitchen over several months, you can draw funds for each project phase. This approach helps manage cash flow and minimizes interest payments.

Cash-out refinances might work better for fixed-cost, large-scale renovations. They provide a lump sum at a potentially lower, fixed interest rate. This option suits homeowners who prefer predictable monthly payments and have a clear project budget.

Debt Consolidation Strategies

Cash-out refinances often lead for debt consolidation. By consolidating debt into a fixed interest personal loan, you could potentially save hundreds, even thousands, of dollars in higher-rate debt.

Consider this scenario: You have $30,000 in high-interest credit card debt. A cash-out refinance could allow you to pay it off entirely. You'd then repay this amount as part of your mortgage at a much lower interest rate. This strategy can reduce your monthly payments and simplify your finances.

HELOCs can also consolidate debt, but their variable rates increase risk for long-term debt repayment. They suit consolidating smaller debts or serve as a temporary solution while you improve your credit score for a more favorable refinance later.

Investment Opportunities

HELOCs excel at creating financial flexibility for investments. Lower interest rates, flexibility and tax deductions are the potential benefits of using a HELOC.

Real estate investors can use a HELOC as a ready source of funds for down payments on new properties or quick renovations to flip houses. The ability to draw funds quickly can provide an edge in competitive markets.

Cash-out refinances suit large, one-time investments where you know the exact amount needed upfront.

Emergency Funds

As an emergency fund, a HELOC provides peace of mind without borrowing costs until you need the money. This setup can prove more cost-effective than a large cash-out refinance with funds sitting idle in a low-interest savings account.

HELOCs offer flexibility for unexpected expenses. You can access funds quickly when needed, without paying interest on unused amounts.

Cash-out refinances are less flexible for emergencies. They provide a lump sum upfront, which might not align with the unpredictable nature of emergencies.

Tax Considerations

Both HELOCs and cash-out refinances can offer tax benefits, but rules apply. Interest may be tax-deductible when funds are used to buy, build, or substantially improve the securing home (subject to limits and conditions set by the IRS).

For cash-out refinances, the entire interest amount may qualify for deduction if used for home improvements (within certain limits). HELOC interest deductions apply only to portions used for home improvements.

(Always consult a tax professional for personalized advice on tax implications.)

Final Thoughts

HELOCs and cash-out refinances offer distinct advantages for homeowners in 2025. HELOCs provide flexibility for ongoing projects, while cash-out refinances suit large, one-time expenses. Your choice depends on your financial goals, income stability, and comfort with interest rate types.

Tax implications play a significant role in your decision. Both options can offer benefits when used for home improvements, but specifics vary. We recommend consulting a tax professional to understand how your choice might impact your tax situation.

At HELOC360, we simplify the process of accessing your home equity. We provide expert guidance and connect you with suitable lenders to help you make an informed decision. Your home is a powerful financial tool, and understanding your options can help you achieve your financial goals.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.