Secrets to Getting Your HELOC Application Approved Fast

Table of Contents

Getting your HELOC application approved quickly can make a big difference in your financial plans. At HELOC360, we've seen how proper preparation can significantly speed up the HELOC approval process.

This guide will reveal the secrets to fast-tracking your application, from organizing your documents to boosting your credit score. We'll also show you how to choose the right lender for your needs.

How to Prepare Your Financial Documents

Income Verification: The Foundation of Your Application

Start your HELOC application process by collecting your income verification documents. W-2 employees should gather their most recent pay stubs and the last two years of tax returns. Self-employed individuals need to prepare the last two years of tax returns, profit and loss statements, and bank statements that show business deposits.

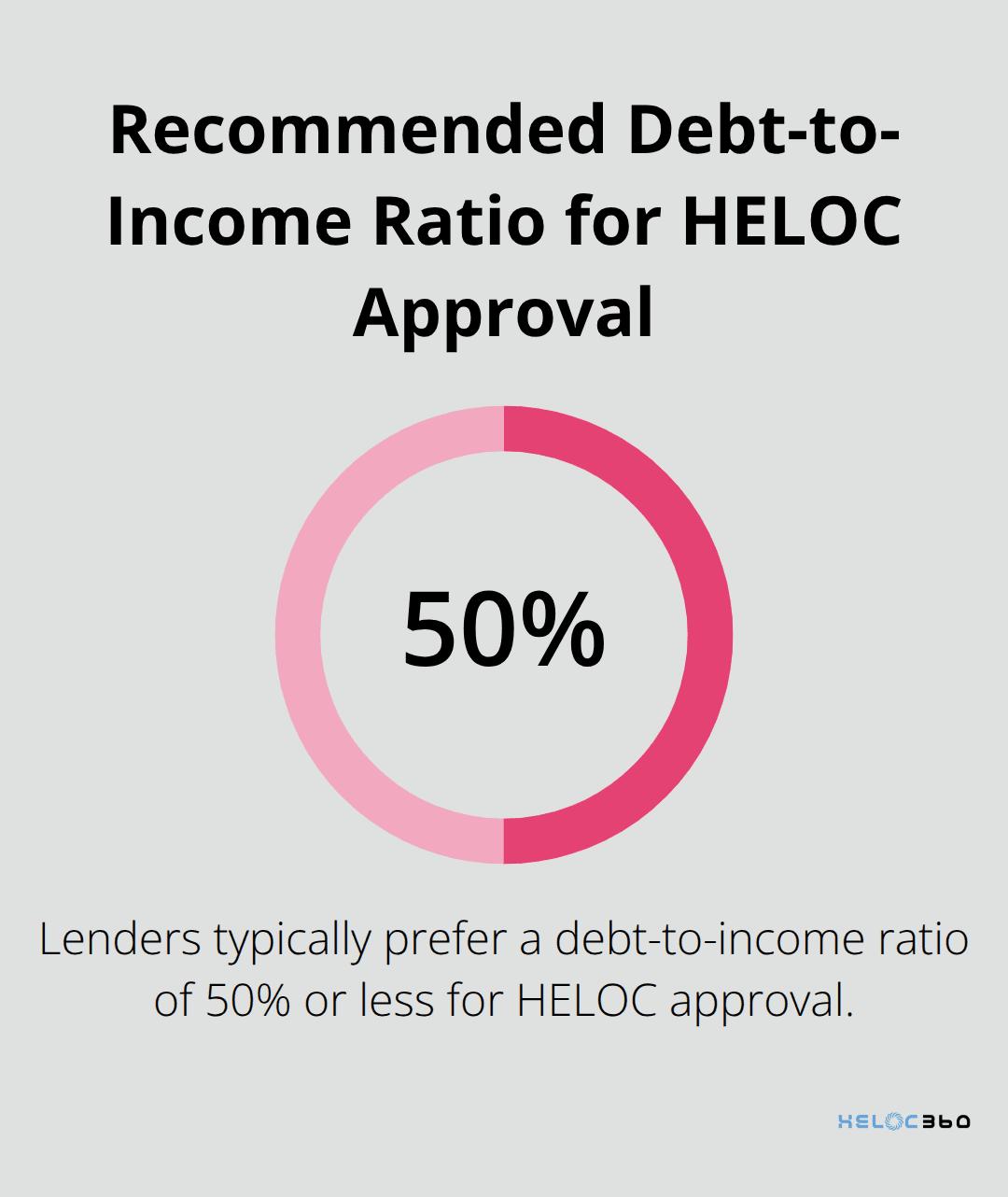

NerdWallet reports that lenders typically prefer a debt-to-income ratio below 50%. Ensure your income documents clearly demonstrate you meet this threshold.

Asset Statements: Proof of Financial Stability

Collect statements for all your assets next. Include checking and savings accounts, investment portfolios, and retirement accounts. Lenders want to see sufficient reserves to cover HELOC payments.

The Federal Reserve notes that having a buffer of savings for emergencies can help families cope with fluctuations in income and unexpected expenses. Try to show a healthy amount in liquid assets to demonstrate financial stability.

Debt Information: A Clear Financial Picture

Organize information about all your current debts. This includes credit cards, personal loans, and any other mortgages. Prepare to provide account numbers, current balances, and monthly payment amounts.

Property Documents: Showcasing Your Home's Value

Compile documents related to your property. This includes your deed, homeowners insurance policy, and recent property tax assessments. If you've had a recent appraisal, include that as well.

The National Association of REALTORS® provides the latest real estate research and statistics that affect the industry. Stay informed about current market trends to understand how they might impact your home's value.

Meticulous preparation of these documents not only satisfies lender requirements but also demonstrates your financial responsibility. This thorough approach increases your chances of a swift approval. Now that you've organized your financial documents, let's move on to the next critical step: boosting your credit score to further strengthen your HELOC application.

How to Boost Your Credit Score for HELOC Approval

Your credit score significantly influences the HELOC approval process. A strong credit score can accelerate applications. Here's how you can improve your credit score before applying for a HELOC.

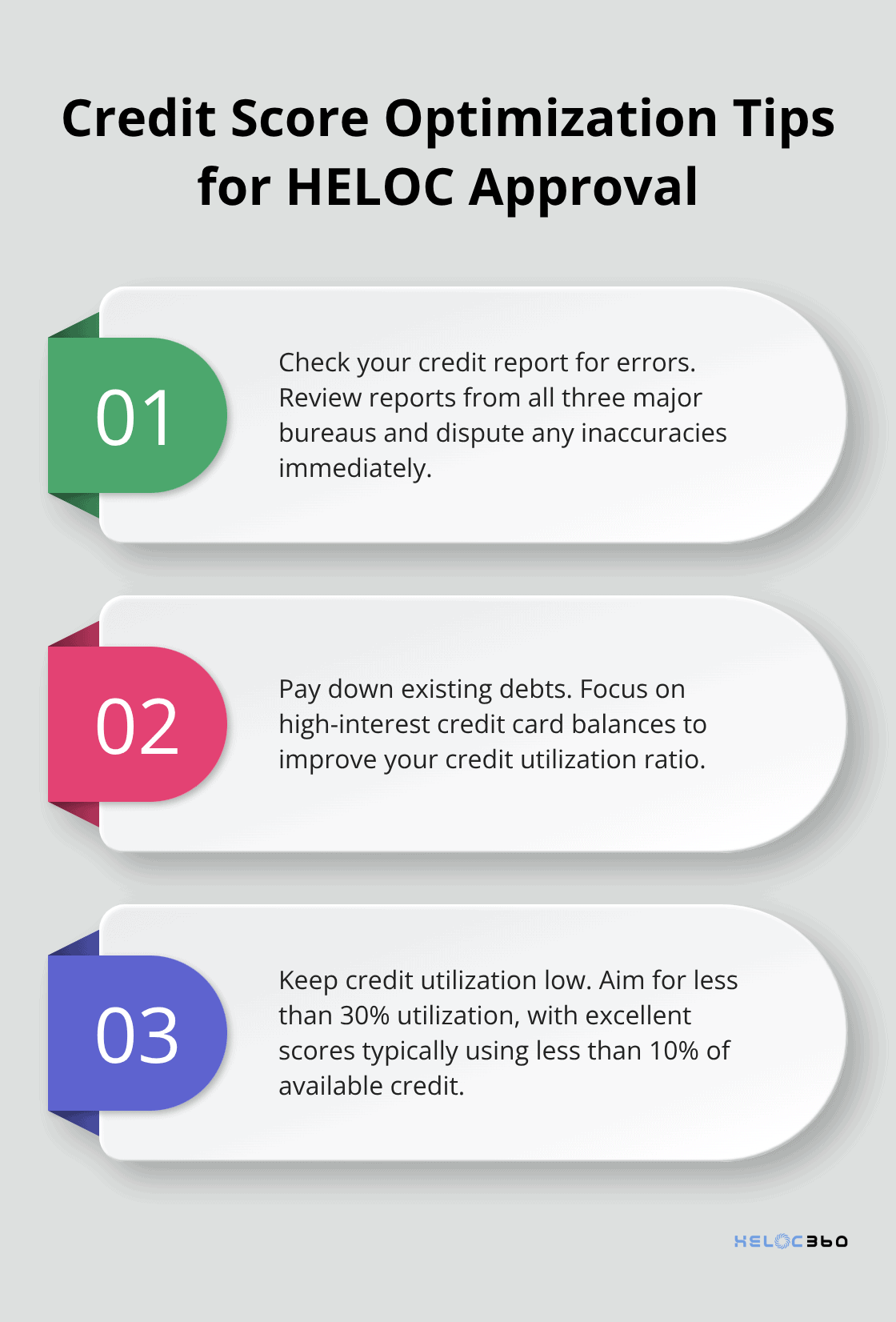

Check Your Credit Report for Errors

Obtain your free credit report from Equifax, Experian, and TransUnion. Review each report for inaccuracies such as incorrect account information, outdated personal details, or fraudulent accounts.

If you find any errors, file a dispute with the relevant credit bureau immediately. They must investigate and respond within 30 days. This action could quickly add points to your score.

Pay Down Existing Debts

Reducing your existing debts is one of the most effective ways to improve your credit score. Prioritize high-interest credit card balances. The Consumer Financial Protection Bureau recommends keeping your credit utilization ratio (the percentage of available credit that you're using on your credit cards and other lines of credit) below 30%.

For instance, if you have a $10,000 credit limit, try to keep your balance under $3,000. Experian reports that consumers with excellent credit scores (800+) typically use less than 10% of their available credit.

Keep Credit Utilization Low

While paying down debts, monitor your ongoing credit usage. Avoid maxing out your credit cards, even if you pay them off in full each month. Credit scoring models often look at your balance at the time it's reported, which may not align with your payment date.

Make multiple payments throughout the month to keep your reported balance low. This strategy can help maintain a low credit utilization ratio, potentially boosting your score.

Avoid New Credit Applications

In the months before your HELOC application, don't apply for new credit. Each hard inquiry on your credit report can temporarily lower your score by a few points. While a single hard inquiry is typically fewer than five points, multiple inquiries in a short period can add up and signal risk to lenders.

New credit accounts also lower your average account age, another factor in your credit score calculation. FICO (the most widely used credit scoring model) considers the age of your oldest account, the newest account, and the average age of all your accounts.

These strategies can potentially lead to a significant improvement in your credit score within a few months. This boost can increase your chances of HELOC approval and help you secure more favorable terms and interest rates. Now that you've optimized your credit score, it's time to focus on another critical aspect of the HELOC application process: selecting the right lender for your needs.

How to Find the Best HELOC Lender

Selecting the right lender for your Home Equity Line of Credit (HELOC) will impact your approval process and terms. This guide will help you navigate the lender selection process effectively.

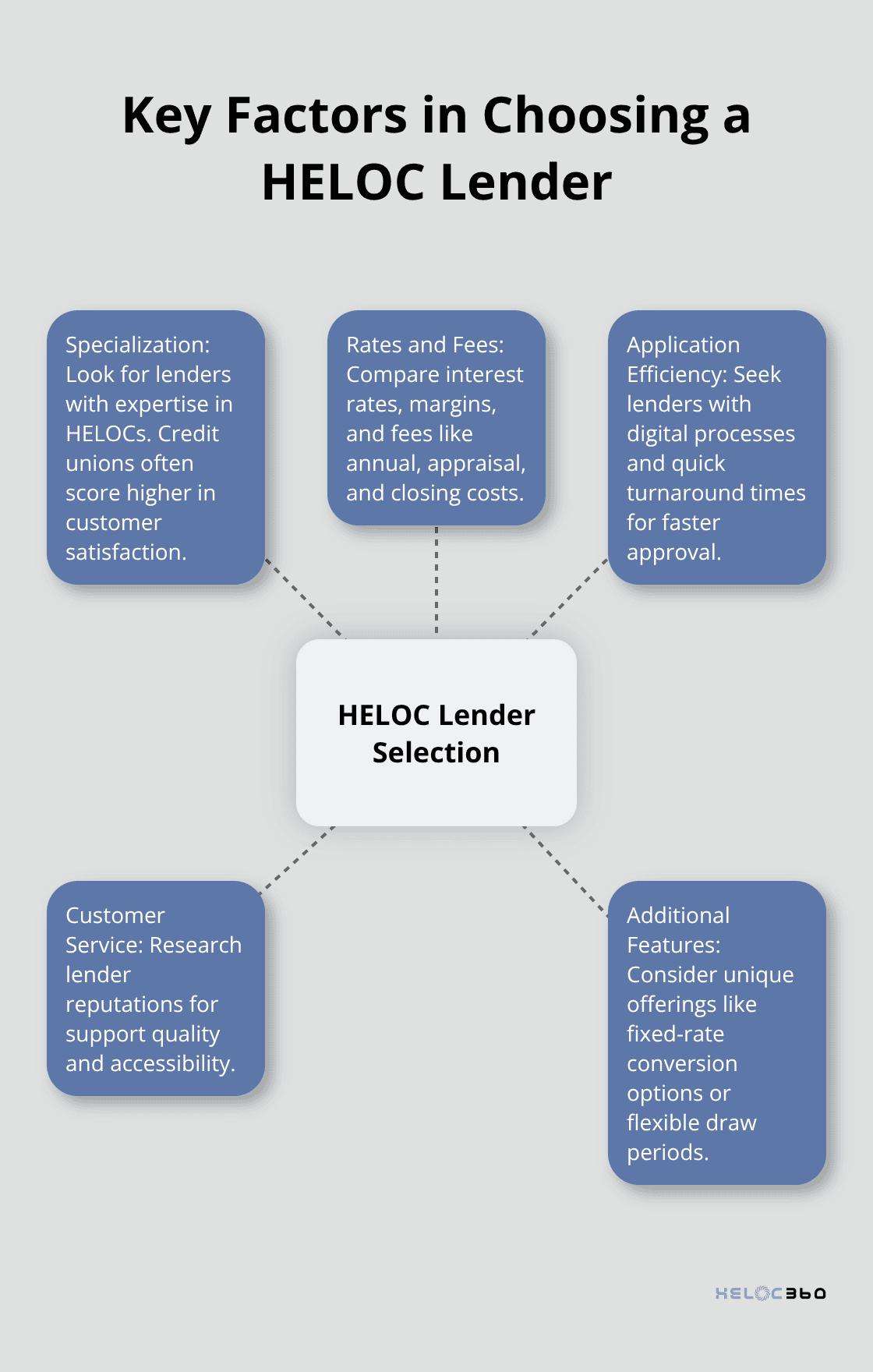

Identify HELOC Specialists

Focus on lenders who specialize in HELOCs. These institutions often have streamlined processes and deeper expertise in home equity products. A 2025 J.D. Power study found that credit unions typically score higher in customer satisfaction for banking products compared to banks, with credit unions scoring 74 points higher than the average bank.

Search for lenders with a strong track record of HELOC approvals and positive customer reviews. The Federal Reserve Bank of New York reported that mortgage balances increased by $190 billion during the first quarter of 2024, indicating growing activity in the housing market.

Analyze Rates and Fees

Interest rates and fees will significantly impact the overall cost of your HELOC. As of August 27, 2025, the national average HELOC rate is 8.10%, according to Bankrate's latest survey of the nation's largest home equity lenders.

Pay close attention to the margin (the percentage points added to the prime rate to determine your variable rate). Margins typically range from 0.5% to 2%. A lower margin can save you thousands over the life of your HELOC.

Don't overlook fees. Common HELOC fees include annual fees ($0 to $75), appraisal fees ($300 to $700), and closing costs (2% to 5% of the credit limit). Some lenders waive these fees for high credit limits or existing customers.

Evaluate Application Efficiency

Time often matters when you apply for a HELOC. Look for lenders that offer digital application processes and quick turnaround times. Some online lenders provide conditional approval within minutes and final approval within days, compared to weeks with traditional banks.

Check if lenders offer features like online document upload, e-signature capabilities, and real-time application status tracking. These features can speed up the process and reduce frustration.

Consider Customer Service

The quality of customer service can make a big difference in your HELOC experience. Research lenders' reputations for customer support, especially for handling issues or questions during the application process and throughout the life of the HELOC.

Look for lenders that offer multiple channels of communication (phone, email, chat) and extended customer service hours. This accessibility can prove invaluable if you encounter any issues or need clarification on your HELOC terms.

Explore Additional Features

Some lenders offer unique features that might align with your financial goals. These could include:

- Fixed-rate conversion options (allowing you to lock in a portion of your balance at a fixed rate)

- Interest-only payment periods

- Flexible draw periods

- No prepayment penalties

Try to find a lender whose offerings match your specific needs and financial situation.

Final Thoughts

Securing a fast HELOC approval requires thorough preparation and strategic decision-making. Organize your financial documents, boost your credit score, and select the right lender to increase your chances of success. These steps will demonstrate your financial responsibility and help lenders process your application quickly.

HELOC360 simplifies the HELOC journey with expert guidance and lender connections. We understand the complexities of navigating the HELOC landscape and provide resources to unlock your home equity's full potential. Our platform matches you with lenders that fit your unique needs, making it easier to achieve your financial goals.

Your home's value is a powerful financial tool. Take action today to prepare for a swift and successful HELOC approval. With proper preparation and the right support, you can confidently use your home equity to open new doors for your financial future.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.