Boost Your HELOC Qualification Odds Today

Securing a Home Equity Line of Credit (HELOC) can be a game-changer for homeowners seeking financial flexibility. However, meeting HELOC qualification criteria can sometimes feel like a challenge.

At HELOC360, we've seen firsthand how proper preparation can significantly boost your chances of approval. This guide will walk you through practical steps to enhance your financial profile and strengthen your HELOC application.

What Are HELOC Qualification Criteria?

Understanding HELOC qualification criteria is essential for homeowners who want to tap into their home equity. Lenders typically evaluate four key factors when considering HELOC applications: credit score, home equity, debt-to-income ratio, and employment stability.

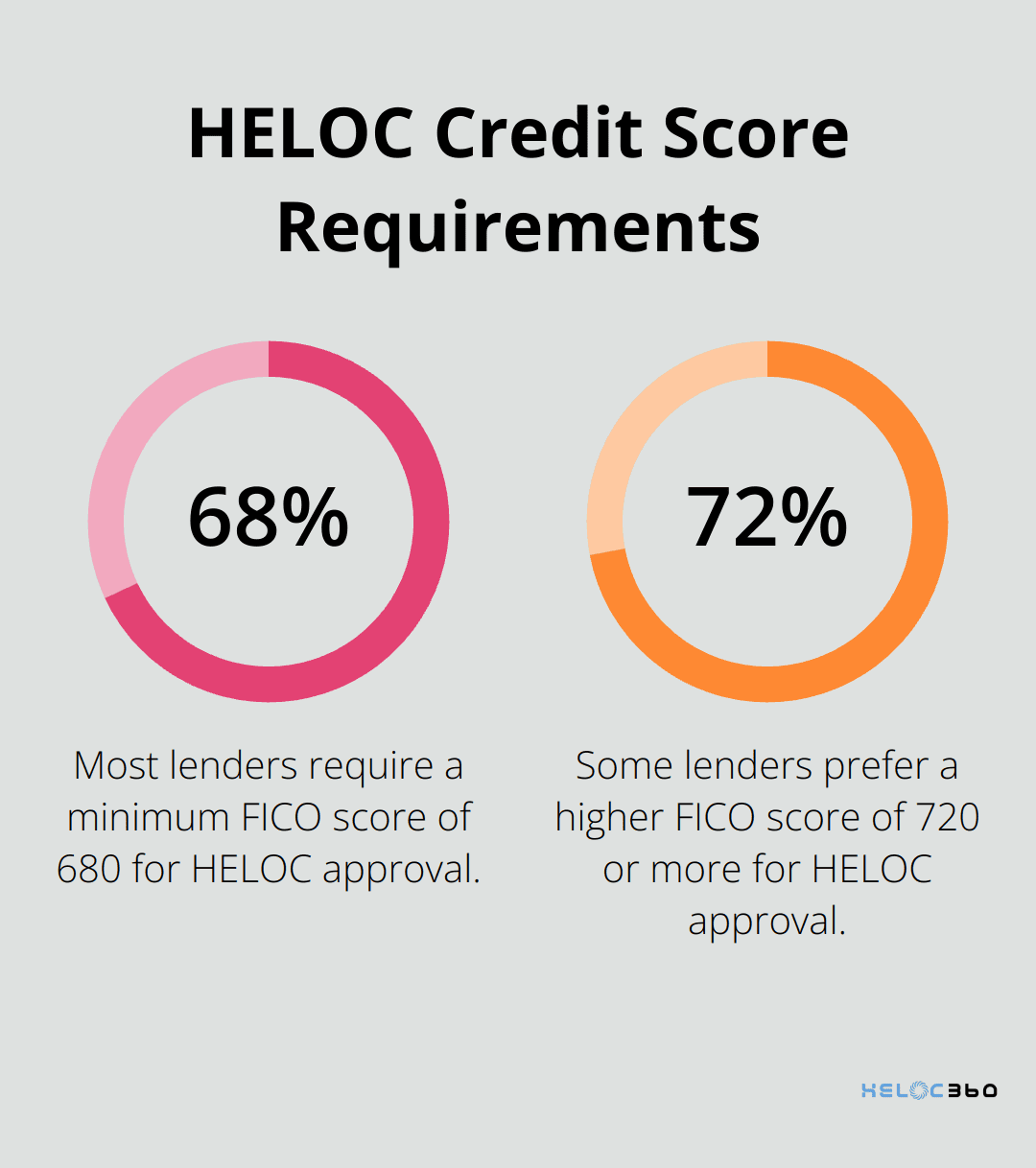

Credit Score: The Gateway to Approval

Your credit score plays a pivotal role in HELOC qualification. Most lenders require a FICO Score of at least 680 to qualify for a HELOC, but some lenders may prefer a credit score of 720 or more.

Home Equity: Your Borrowing Power

Lenders typically allow homeowners to borrow based on their loan-to-value (LTV) ratio. To calculate your LTV, divide your current loan balance by the current appraised value of your home. For example, if your loan balance is $140,000 and your home's appraised value is $200,000, your LTV would be 70% ($140,000 ÷ $200,000 = .70).

Debt-to-Income Ratio: Balancing Act

Your debt-to-income (DTI) ratio is important for HELOC approval. Your DTI is calculated by adding up all your monthly debt payments and dividing them by your gross monthly income.

Employment and Income Stability: Proving Reliability

Lenders want to see a stable income history, typically looking for at least two years of consistent employment. Self-employed individuals may need to provide additional documentation (such as tax returns for the past two years) to demonstrate income stability.

Lender-Specific Requirements

It's important to note that while these criteria are general guidelines, individual lender requirements may vary. Different lenders have varying policies regarding HELOC LTVs. While many cap their LTVs at 80-85%, some may offer higher limits for well-qualified borrowers. Shopping around and comparing offers from multiple lenders can help you find the best terms for your situation.

Now that you understand the key factors lenders consider, let's explore how you can improve your financial profile to increase your chances of HELOC approval.

How to Boost Your Financial Profile for HELOC Approval

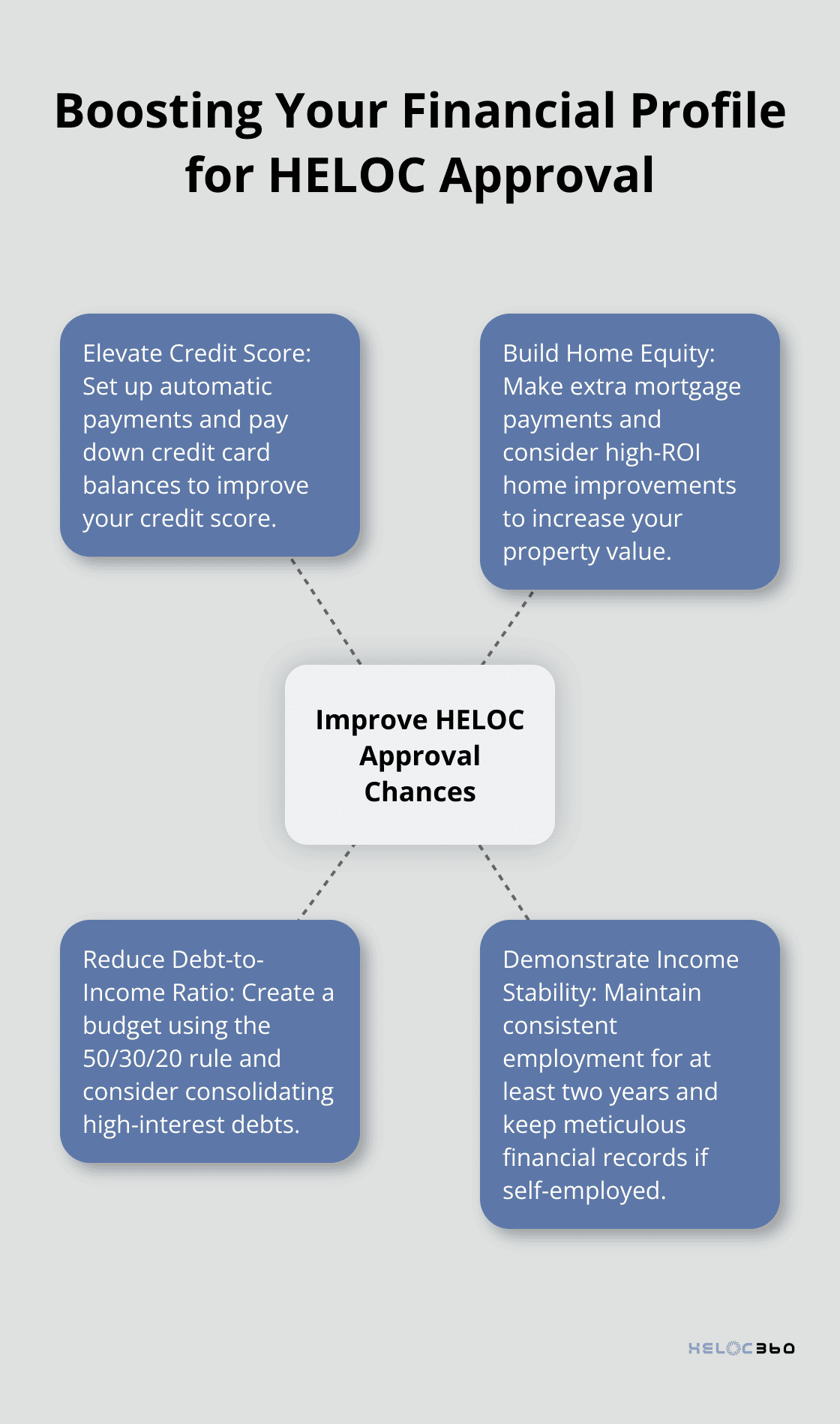

Elevate Your Credit Score

Your credit score significantly influences HELOC approval. Applying for, opening and using a HELOC can help or hurt your credit scores depending on your overall credit profile and how you manage the account. Set up automatic payments for all your bills to avoid missed due dates. Try to pay down credit card balances, as credit utilization comprises 30% of your score.

Build More Home Equity

Increasing home equity is vital for HELOC qualification. To capitalize on this trend, consider making extra mortgage payments. An additional $100 per month can significantly reduce your principal over time. Home improvements can also boost your property value. Focus on projects with high ROI, such as kitchen remodels. The average rate on HELOCs ticked up above 8%, according to Bankrate's weekly survey, while home equity loan rates remained unchanged.

Reduce Your Debt-to-Income Ratio

A lower debt-to-income (DTI) ratio improves your HELOC eligibility. To calculate your estimated DTI ratio, simply enter your current income and payments. This can help you understand what it means for your financial situation. To improve your DTI, create a budget using the 50/30/20 rule: allocate 50% of your income to needs, 30% to wants, and 20% to savings and debt repayment. Consider consolidating high-interest debts into a personal loan with a lower interest rate. This strategy can reduce your monthly payments and improve your DTI.

Demonstrate Income Stability

Lenders favor applicants with stable income. If you're self-employed, maintain meticulous financial records. Use accounting software like QuickBooks or FreshBooks to track income and expenses. For W-2 employees, staying with the same employer for at least two years can strengthen your application. If you've recently changed jobs within the same industry, highlight how your new position offers career growth and increased earning potential.

Prepare for the Next Steps

As you work on improving these aspects of your financial profile, you'll position yourself as a stronger candidate for HELOC approval. The next crucial step is to prepare a compelling HELOC application that showcases your improved financial standing and demonstrates your readiness to responsibly manage a home equity line of credit.

How to Craft a Winning HELOC Application

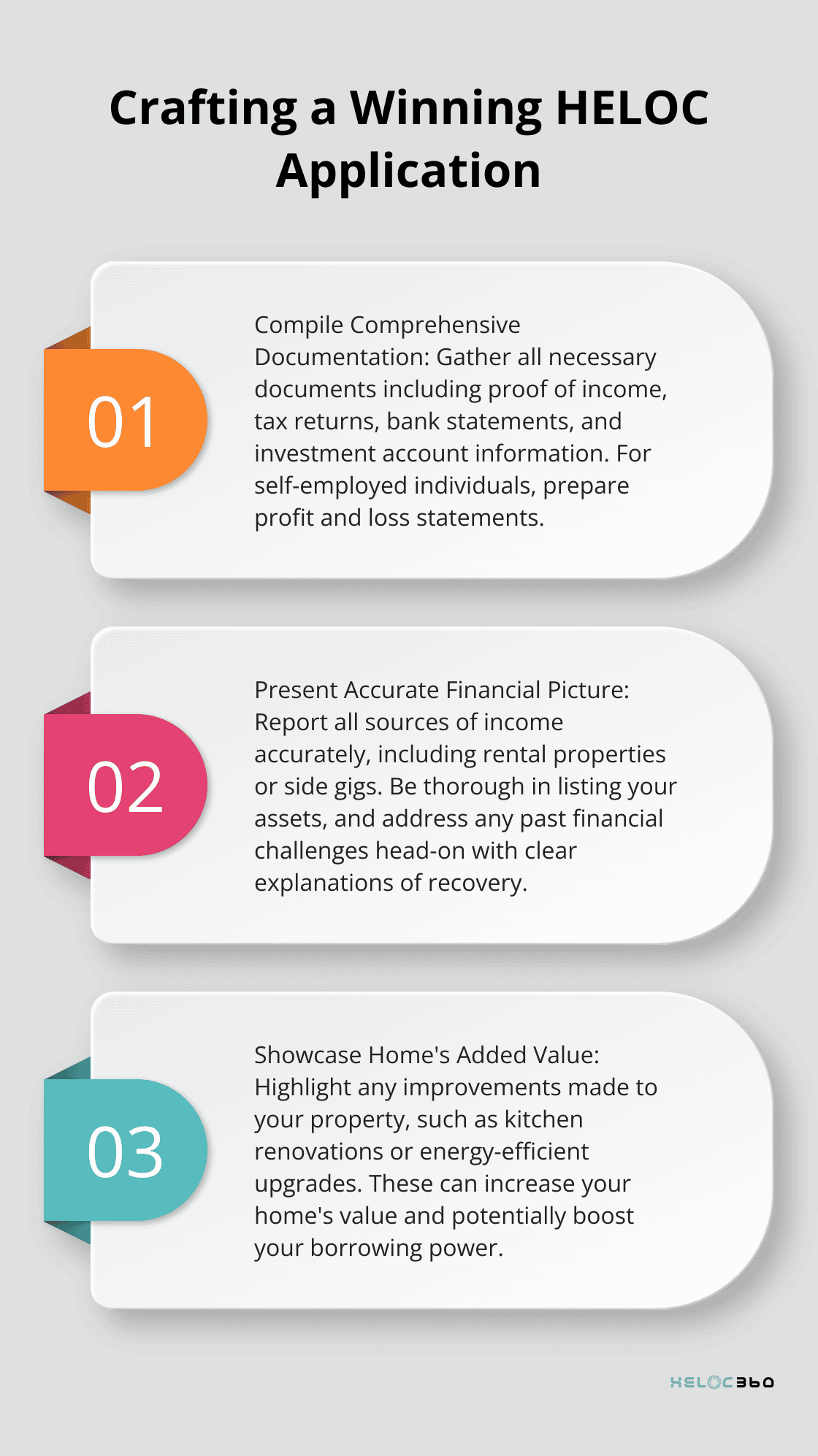

Compile a Comprehensive Documentation Package

Start by gathering all necessary documents. Traditionally, lenders require several documents to approve a HELOC. These include proof of income, such as pay stubs or tax returns, and verification of your assets. Self-employed individuals should prepare profit and loss statements. Don't forget recent bank statements and investment account information. A complete documentation package streamlines the process and demonstrates your organizational skills to lenders.

Present Your Financial Picture Accurately

When you report your income and assets, accuracy is paramount. Include all sources of income (such as rental properties or side gigs). Be thorough in listing your assets, including savings accounts, investments, and valuable personal property. HELOC rates have fallen substantially from the highs reached at the beginning of 2024, with HELOC rates in particular hitting new lows as of April 30, 2025.

Address Past Financial Challenges Head-On

Don't shy away from credit issues or financial setbacks. Provide a clear, concise explanation of what happened and how you recovered. For example, if you lost your job but have since secured stable employment, highlight this positive turn. Experian analyzed U.S. consumer credit data to find recent trends in the home financing market, providing insights into HELOC trends for 2025.

Showcase Your Home's Added Value

Highlight any improvements you've made to your property. Did you renovate the kitchen? Install energy-efficient windows? These upgrades can increase your home's value and potentially boost your borrowing power. The National Association of Realtors reports that kitchen remodels recover about 52% of their cost at resale, while new windows can recoup up to 72% of their cost.

Leverage Professional Guidance

Consider seeking professional advice to strengthen your application. Financial advisors or HELOC specialists can provide valuable insights into lender preferences and help you present your financial information in the most favorable light. Their expertise can prove invaluable in navigating the application process and increasing your chances of approval.

Final Thoughts

HELOC qualification requires a strategic approach to improve your financial profile. You should focus on enhancing your credit score, building home equity, reducing your debt-to-income ratio, and demonstrating income stability. These actions will position you as a strong candidate for HELOC approval and show lenders that you can manage credit effectively.

Thorough preparation plays a key role in the HELOC application process. You need to gather comprehensive documentation, present your financial picture accurately, address past challenges, and showcase your home's added value. These steps will contribute to a compelling application and increase your chances of approval.

The HELOC qualification process can be complex, but you don't have to navigate it alone. HELOC360 simplifies your journey and helps you unlock the full potential of your home equity. Our platform provides expert guidance, connects you with suitable lenders, and offers tailored solutions (meeting your unique financial goals).

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.