Using a HELOC for Home Improvement A Smart Financial Move?

Table of Contents

Are you considering using a HELOC for home improvement? This financial tool can be a game-changer for homeowners looking to upgrade their living spaces.

At HELOC360, we've seen firsthand how HELOCs can transform homes and improve property values. But is it the right choice for you?

Let's explore the ins and outs of using a HELOC for home improvement and help you make an informed decision.

What Is a HELOC and How Can It Benefit Your Home Improvement Plans?

A Home Equity Line of Credit (HELOC) is a powerful financial tool that allows homeowners to tap into their home's equity for various purposes, including home improvements. Many homeowners successfully use HELOCs to fund their renovation projects and increase their property values.

How a HELOC Works

A HELOC functions like a revolving credit line, similar to a credit card, but with your home as collateral. You can borrow up to a certain limit, typically 85% of your home's value minus your mortgage balance. The Federal Reserve reports that as of 2023, the average HELOC limit is around $114,000.

Benefits of Using a HELOC for Home Improvements

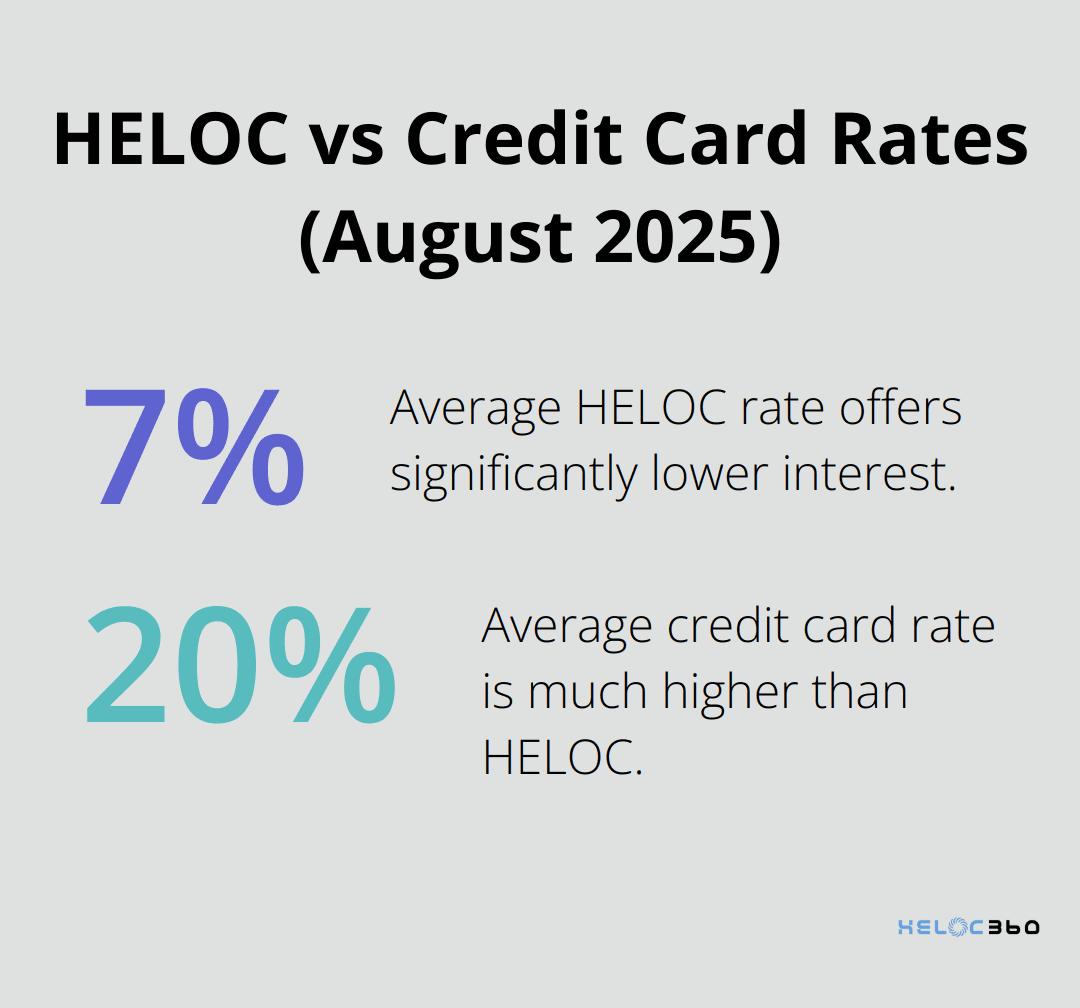

One of the main advantages of using a HELOC for home improvements is the flexibility it offers. You can draw funds as needed, which is perfect for ongoing renovation projects. HELOCs also typically offer lower interest rates compared to credit cards or personal loans. As of August 2025, the average HELOC rate is 7.5%, while credit card rates average around 20%. This difference can translate to significant savings over the life of your renovation project.

HELOC vs. Other Financing Options

When comparing HELOCs to other financing options, it's important to consider your specific needs. Home equity loans provide a lump sum upfront, which might be suitable for one-time, large expenses. However, they lack the flexibility of a HELOC for ongoing projects.

Personal loans, while unsecured, often come with higher interest rates. Cash-out refinancing is another option, but it involves replacing your entire mortgage, which may not be ideal if you already have a low interest rate on your existing mortgage.

Choosing the Right Option for You

Your choice of financing will depend on various factors (such as your credit score, home equity, and project timeline). It's essential to weigh the pros and cons of each option carefully. A HELOC might be the best choice if you want flexibility and potentially lower interest rates, but it's not a one-size-fits-all solution.

As you consider your options, you might want to explore platforms that can help you navigate the HELOC landscape. These tools can connect you with lenders offering competitive rates and terms, ensuring you get the best deal for your unique situation.

Now that we've covered the basics of HELOCs and their benefits for home improvements, let's move on to some key considerations you should keep in mind before deciding to use a HELOC for your renovation projects.

Key Considerations Before Using a HELOC

Interest Rates and Repayment Terms

HELOCs typically feature variable interest rates, which can impact your payments over time. As of August 2025, the average HELOC rate is 8.13%. However, this rate may change based on market conditions and your credit profile. You should factor potential rate increases into your home improvement budget.

HELOC repayment terms consist of two phases: the draw period and the repayment period. The draw period (often 5-10 years) allows you to borrow funds as needed and make interest-only payments. The repayment phase follows, requiring you to pay back both principal and interest. This transition can significantly increase your monthly payments, so plan accordingly.

Impact on Home Equity

Using a HELOC means borrowing against your home's equity, which affects your overall financial picture. While home improvements can potentially increase your property value, it's not guaranteed. Consider how much equity you're comfortable leveraging and how it aligns with your long-term financial goals.

Credit Score Requirements

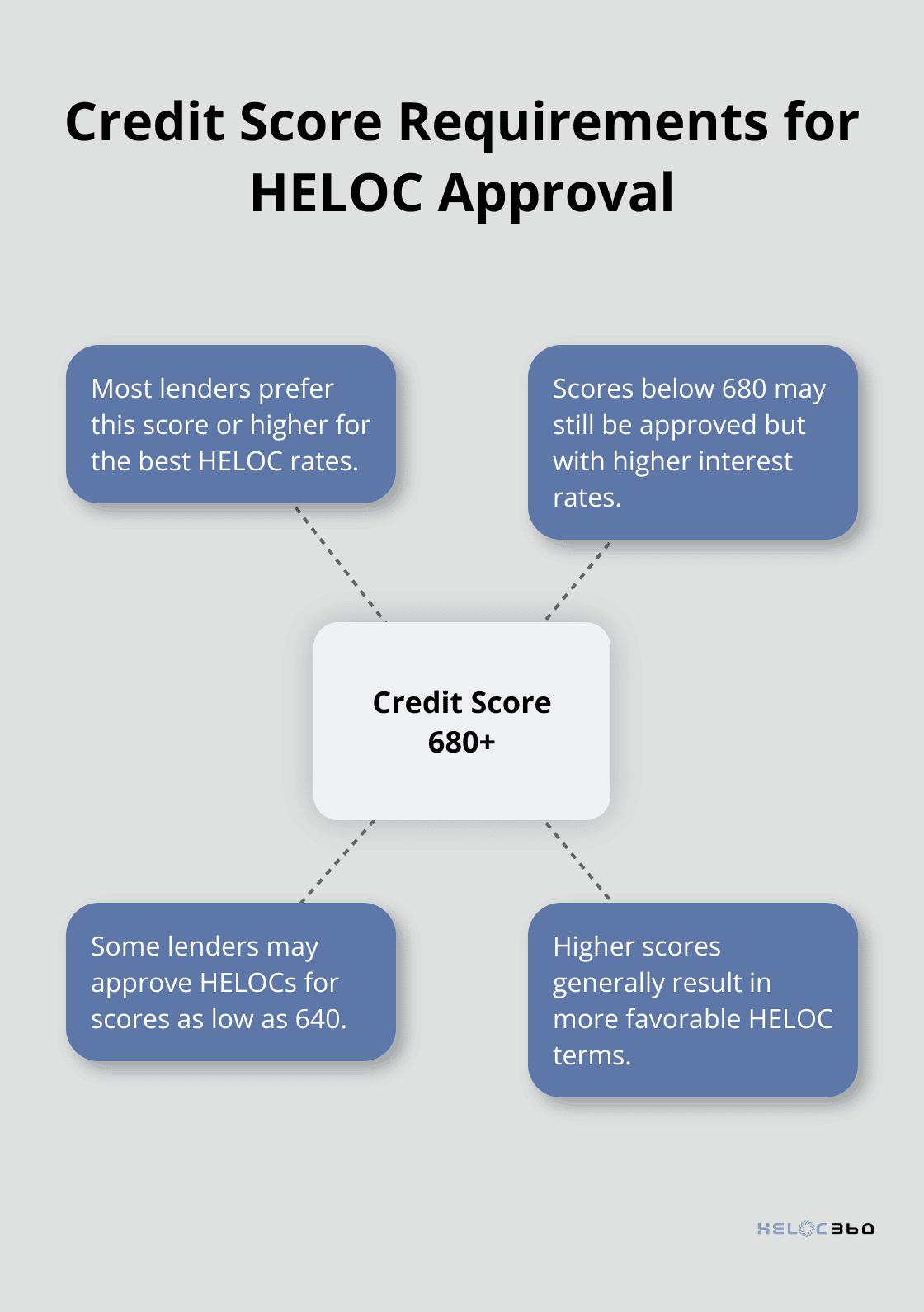

Your credit score plays a significant role in HELOC approval and the interest rate you'll receive. Most lenders prefer a credit score of 680 or higher for the best rates. However, some lenders may approve HELOCs for scores as low as 640. Before applying, check your credit report for any errors and take steps to improve your score if needed.

Potential Risks and Drawbacks

While HELOCs offer flexibility and potentially lower interest rates, they come with risks. The most significant is the possibility of losing your home if you default on payments, as your property serves as collateral. Additionally, if your home's value decreases, you could end up owing more than your home is worth.

Another consideration is the temptation to overspend. The revolving nature of a HELOC can make it easy to borrow more than you initially planned. Set a strict budget for your home improvement project and stick to it to avoid this pitfall.

Be aware of potential fees associated with HELOCs. These may include application fees, annual maintenance fees, and early closure fees. Always read the fine print and factor these costs into your decision-making process.

Now that you understand the key considerations for using a HELOC, let's explore how to maximize its value for your home improvement projects.

How to Maximize Your HELOC's Value

Focus on High-ROI Projects

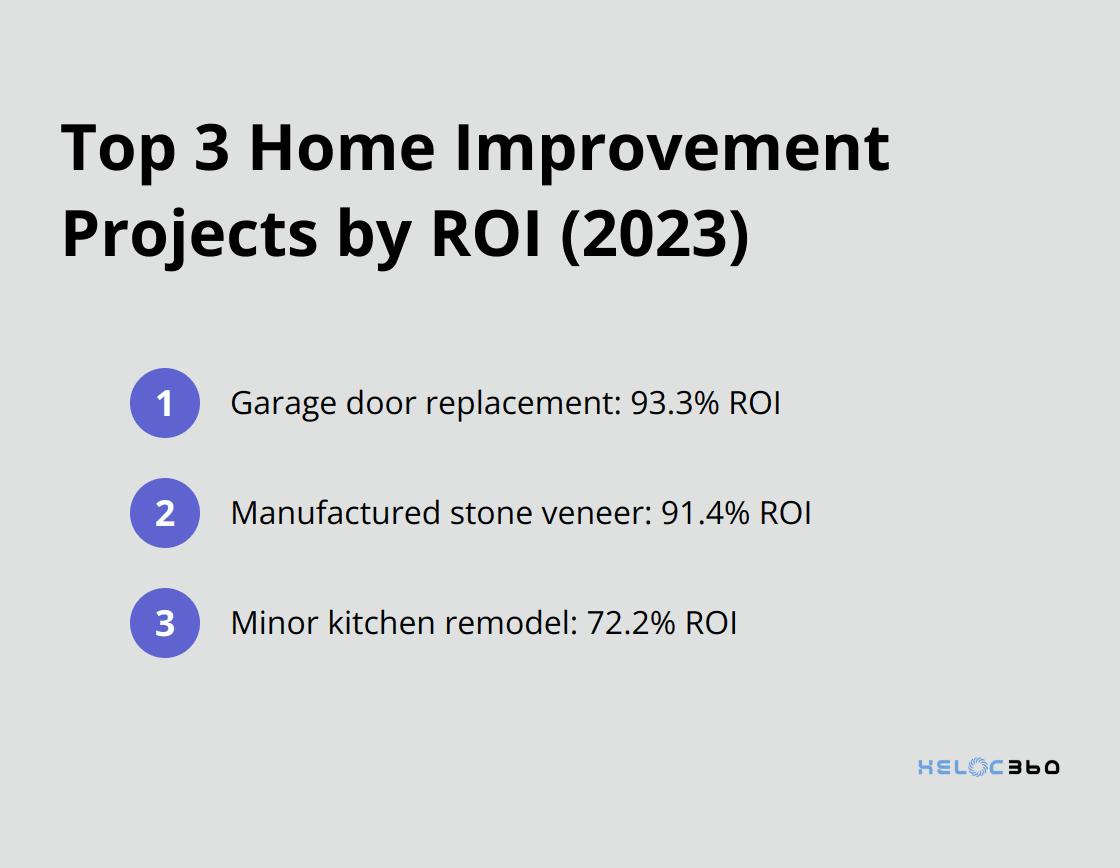

Not all home improvements offer equal returns on investment (ROI). The 2023 Cost vs. Value Report by Remodeling Magazine highlights some of the highest ROI projects:

- Garage door replacement (93.3% ROI)

- Manufactured stone veneer (91.4% ROI)

- Minor kitchen remodel (72.2% ROI)

These projects enhance your home's functionality and aesthetics while significantly boosting its market value. A minor kitchen remodel (costing around $26,000) can recoup about $18,800 in added home value.

Create a Detailed Budget and Timeline

Before you tap into your HELOC, develop a comprehensive budget and project timeline. This step prevents overspending and ensures project completion within the HELOC's draw period.

Start by obtaining multiple quotes from contractors for each aspect of your project. Add a 10-20% buffer to your budget for unexpected expenses. Nine out of 10 homeowners who bought a home in the last three years say they were unprepared for the extra costs of maintaining and financing their property.

Break down your project into phases, aligning each phase with your HELOC draws. This approach helps manage cash flow and keeps interest charges in check.

Manage Your HELOC Effectively

To maximize the benefits of your HELOC while minimizing costs:

- Pay more than minimum payments: During the draw period, pay more than just the interest. This reduces your principal and overall interest costs.

- Use a HELOC calculator: These tools help you estimate monthly home equity payments based on the amount you want, rate options, and other factors.

- Set up automatic payments: This practice ensures you never miss a payment, protecting your credit score and avoiding potential penalties.

- Monitor your credit utilization: Keep your HELOC balance below 30% of your credit limit to maintain a healthy credit score.

- Consider rate-lock options: Some lenders offer the ability to lock in rates on portions of your HELOC balance (providing protection against future rate increases).

Leverage Expert Guidance

Navigating the complexities of HELOCs and home improvements can be challenging. Platforms like HELOC360 offer expert guidance and connect you with lenders that fit your unique needs. This support can help you make informed decisions and maximize the value of your HELOC.

Stay Informed About Market Trends

Keep an eye on real estate market trends in your area. Understanding which home improvements are most valued in your local market can help you prioritize projects that will yield the highest returns. Local real estate agents or home appraisers can provide valuable insights into which improvements are most likely to increase your home's value.

Final Thoughts

A HELOC for home improvement can offer a flexible and cost-effective way to fund renovations. Homeowners who use this financial tool can potentially increase their property value while creating a more comfortable living space. However, it's important to consider the risks, such as variable interest rates and using your home as collateral, before making a decision.

Successful use of a HELOC requires careful planning, a realistic budget, and a clear understanding of your financial goals. Focusing on high-ROI projects and managing your HELOC effectively will help you maximize the value of your home improvements. You should also stay informed about local real estate market trends to prioritize renovations that will yield the highest returns.

Navigating the complexities of HELOCs doesn't have to be overwhelming. HELOC360 provides expert guidance and connects homeowners with suitable lenders (making it easier to explore your options). With the right approach and resources, a HELOC can become a powerful tool for transforming your home and potentially enhancing your financial future.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.