What You Need to Know About HELOC Liens [Guide]

Table of Contents

Home equity lines of credit (HELOCs) can be a powerful financial tool, but they come with important considerations. One crucial aspect is understanding HELOC liens and their impact on your property.

At HELOC360, we've created this comprehensive guide to help you navigate the complexities of HELOC liens. We'll explore what they are, how they work, and what they mean for homeowners.

What Is a HELOC Lien?

Definition and Basics

A HELOC lien is a legal claim placed on your property when you take out a Home Equity Line of Credit. This lien gives the lender a secured interest in your home, acting as collateral for the borrowed funds. It's important to note that a HELOC lien differs from your primary mortgage lien.

How HELOC Liens Function

When you open a HELOC, the lender files a lien with your county recorder's office. This lien typically takes second priority to your primary mortgage. If you default on your HELOC payments, the lender has the right to foreclose on your property, but only after the primary mortgage lender receives payment.

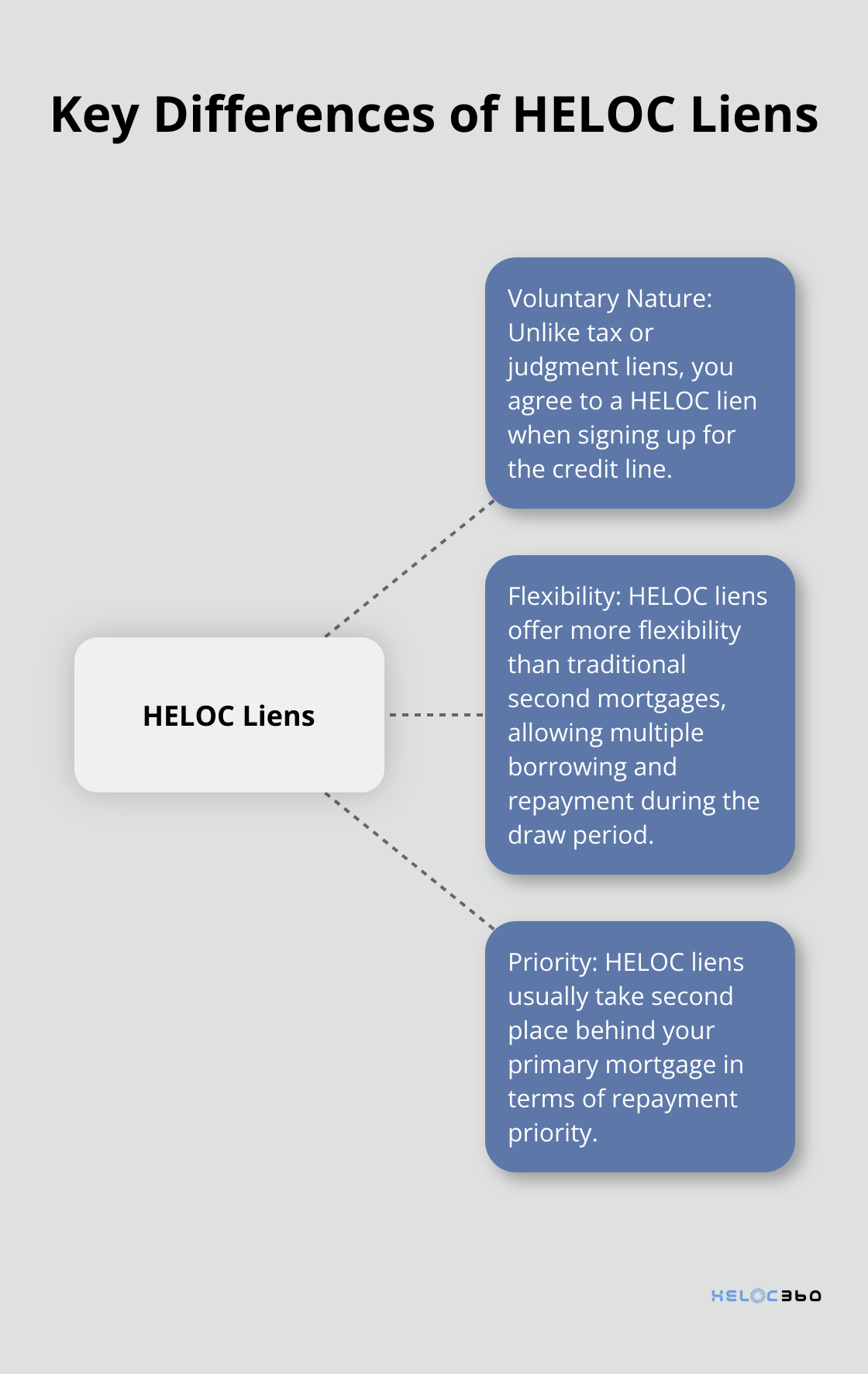

HELOC Liens vs. Other Types of Liens

HELOC liens stand apart from other types of liens in several ways:

- Voluntary nature: Unlike tax liens or judgment liens (which are involuntary), you agree to a HELOC lien when you sign up for the credit line.

- Flexibility: HELOC liens offer more flexibility than traditional second mortgages, allowing you to borrow and repay funds multiple times during the draw period.

- Priority: HELOC liens usually take second place behind your primary mortgage in terms of repayment priority.

Legal Implications for Homeowners

The presence of a HELOC lien on your property carries significant legal implications. It can affect your ability to sell or refinance your home. When you decide to sell, you'll need to pay off the HELOC balance to clear the lien. This could reduce your proceeds from the sale.

Considerations Before Taking on a HELOC Lien

If you're thinking about a HELOC, you should weigh these factors carefully:

- Impact on home equity: A HELOC lien will reduce your available equity. Lenders may freeze or reduce your credit line if your home's value falls or if they see a change for the worse in your financial situation.

- Repayment obligations: You'll need to repay the borrowed amount (plus interest).

- Foreclosure risk: Failure to repay can lead to foreclosure.

Understanding these aspects of HELOC liens is essential for making informed decisions about leveraging your home equity. As we move forward, let's explore the process of how HELOC liens are placed on your property and what this means for you as a homeowner.

How Does the HELOC Lien Process Work?

Placing a HELOC Lien on Your Property

The HELOC lien process starts when you apply for and receive approval for a Home Equity Line of Credit. After you sign the agreement, your lender files a document (often called a deed of trust or mortgage) with your local county recorder's office. This document officially records the lender's interest in your property.

Your lender will conduct a title search to check for existing liens or encumbrances that could affect their position. A professional title abstractor examines public records to pull together all relevant information. They will also require a property appraisal to determine your home's current market value, which influences your borrowing amount.

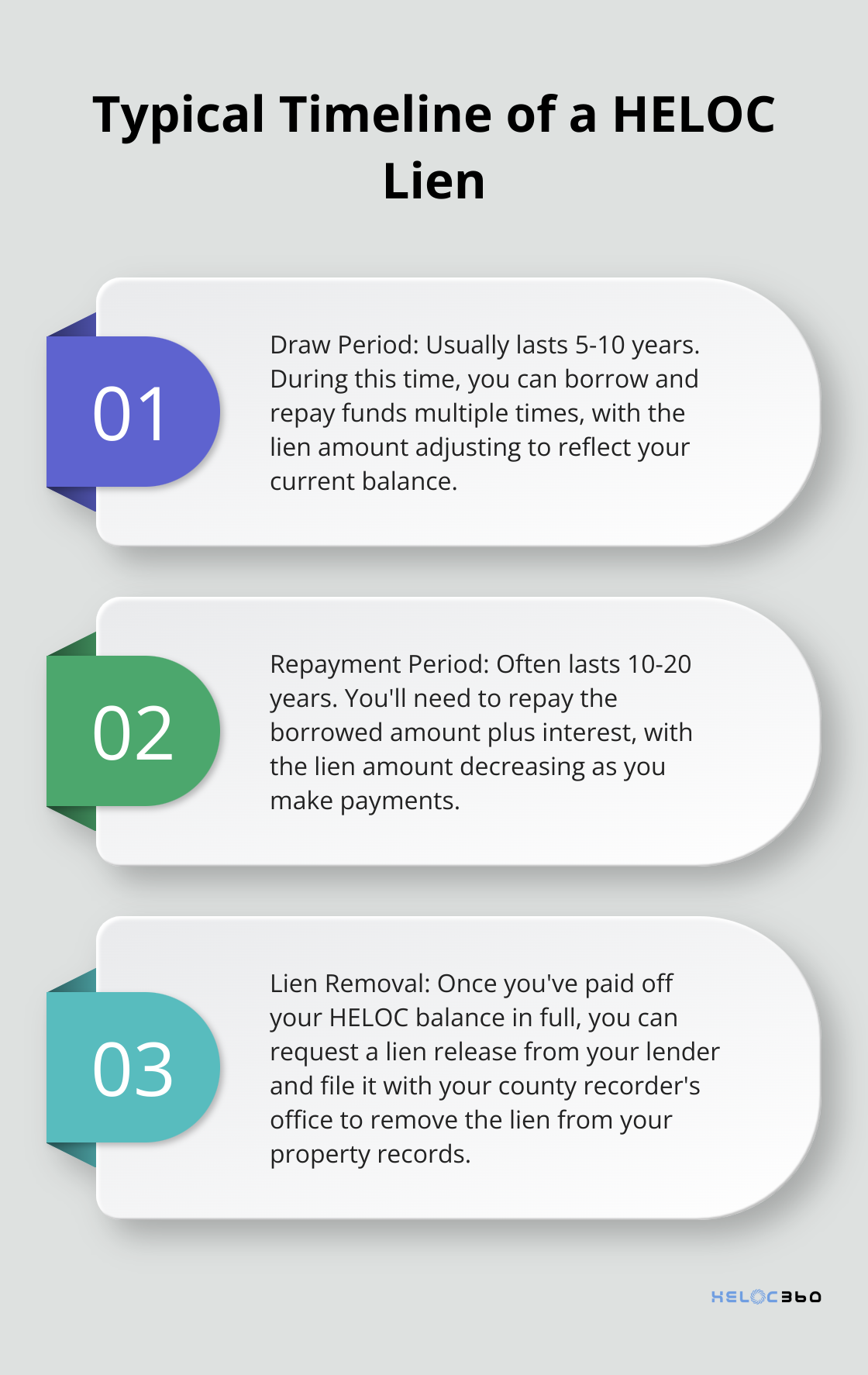

The Lifespan of a HELOC Lien

A HELOC lien typically stays on your property for the duration of your agreement with the lender. This period includes both the draw period (usually 5-10 years) and the repayment period (often 10-20 years). The exact timeline can vary based on your specific agreement and lender policies.

The lien amount may fluctuate during this time. As you borrow and repay funds, the lien adjusts to reflect your current balance. This dynamic nature distinguishes HELOC liens from traditional mortgage liens, which have a fixed amount that decreases steadily over time.

Removing a HELOC Lien from Your Property

Removing a HELOC lien requires specific actions on your part. The most straightforward way to remove the lien is to pay off your HELOC balance in full. Once you've done this, you should request a lien release from your lender. The FDIC may be able to assist you in obtaining a lien release if the lender is no longer in business.

After you receive the lien release, you must file it with your county recorder's office. This step is essential - without it, the lien may still appear on your property records, potentially causing complications in future real estate transactions.

Some lenders may charge a fee for processing the lien release. Always check your HELOC agreement or ask your lender about any potential costs associated with lien removal.

Understanding HELOC Lien Priority

HELOC liens usually take second place behind your primary mortgage in terms of repayment priority. This means that if you default on your payments and your home goes into foreclosure, the primary mortgage lender gets paid first from the sale proceeds. The HELOC lender only receives payment if there are remaining funds after the first mortgage is satisfied.

This priority system can affect your ability to refinance or take out additional loans against your home equity. Lenders will consider the total amount of liens against your property when determining your eligibility for new financing.

The HELOC process involves several steps and considerations. At the end of the approval process, you'll get a three-day right of rescission. As we move forward, let's explore how these liens impact homeowners in various aspects of property ownership and financial planning.

How HELOC Liens Impact Your Homeownership

Property Sales and Refinancing Challenges

Home equity "investment" contracts (HEIs) can complicate the process of selling or refinancing your home. With HEIs, homeowners get cash up front in exchange for a repayment later, but these contracts can be risky. When you sell, you must pay off the balance to clear the lien. This reduces your sale proceeds, potentially affecting your ability to purchase a new home or invest elsewhere.

Refinancing with a lien presents its own set of challenges. Lenders evaluate the total amount of liens against your property to determine your eligibility for new financing.

Financial Risks and Benefits

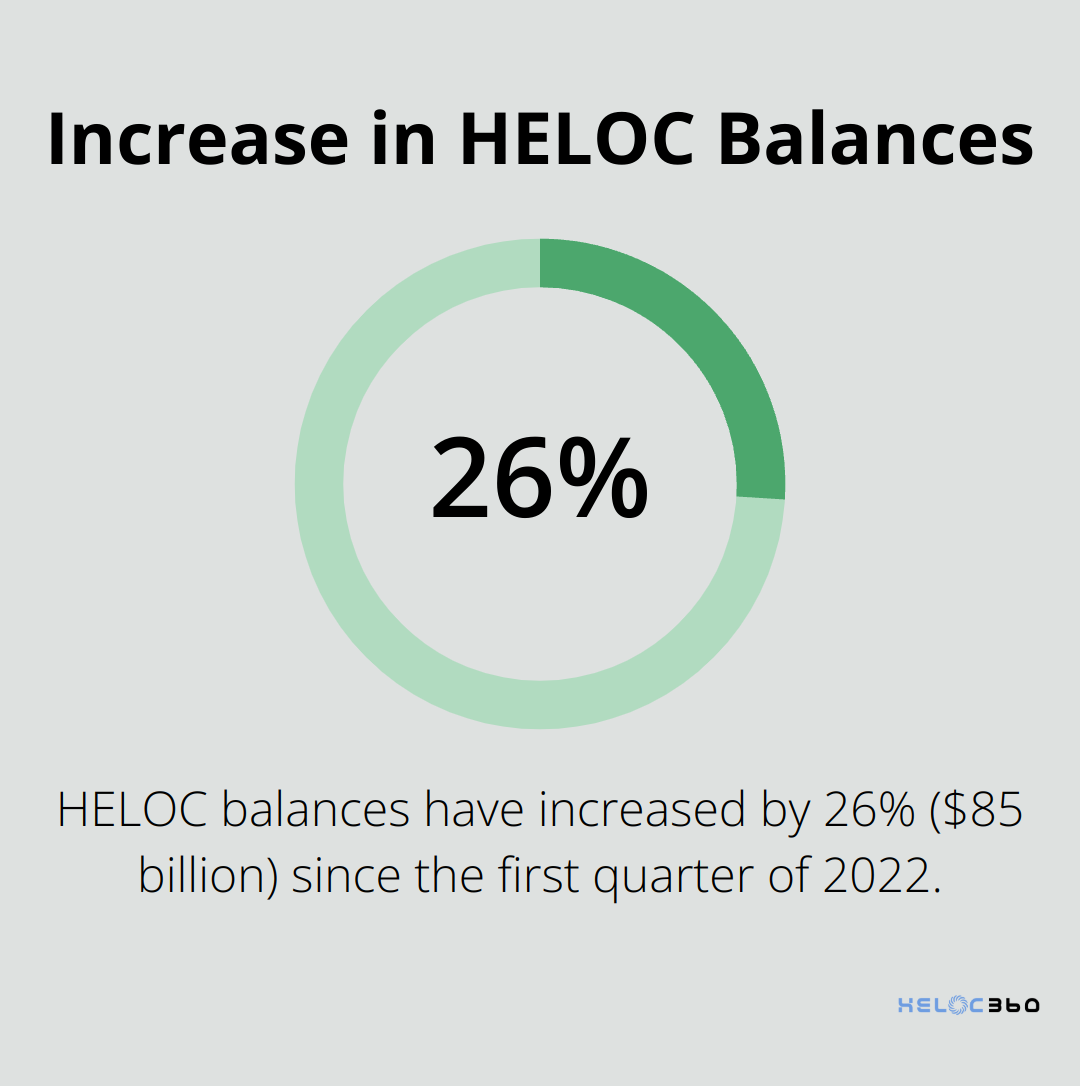

HELOCs offer financial flexibility but come with risks. The most significant risk is foreclosure if you default on payments. Credit card balances now total $402 billion in outstanding HELOC balances, $85 billion above the low reached in the first quarter of 2022.

However, HELOCs can provide substantial benefits when used wisely. They often offer lower interest rates compared to credit cards or personal loans.

Credit Score Implications

A HELOC lien can affect your credit score both positively and negatively. Timely payments can boost your credit score. However, late payments or high utilization of your HELOC can harm your credit. A recent report shows that the average FICO score fell to 742 in 2023 from 752 in 2022. Average CLTV at closing increased to 62 percent in 2023 from 58 percent in 2022.

To optimize your credit score, try to maintain a lower HELOC utilization rate. Setting up automatic payments ensures you never miss a due date.

Impact on Future Borrowing

The presence of a HELOC lien can influence your ability to secure additional loans. Lenders consider your total debt obligations when evaluating loan applications. A high HELOC balance might limit your options for future borrowing or result in less favorable terms.

Property Value Fluctuations

Your HELOC's available credit can change based on your property's value. If your home's value decreases, the lender may reduce your credit limit (a process known as a "freeze" or "reset"). This can impact your financial planning and access to funds when you need them most.

Legal Considerations

Legal issues can significantly affect your HELOC eligibility and terms. Ongoing lawsuits or other legal matters may be viewed unfavorably by lenders, potentially impacting your ability to secure or maintain a HELOC.

Final Thoughts

HELOC liens represent a lender's legal claim on your property when you take out a Home Equity Line of Credit. These liens impact various aspects of homeownership, from property sales to refinancing options. HELOC liens can affect your ability to sell or refinance your home, influence your credit score, and impact future borrowing opportunities.

While HELOCs offer financial flexibility, they also come with risks (including potential foreclosure if payments are not met). You should weigh the benefits against the potential drawbacks before obtaining a HELOC. Consider your long-term financial goals, your ability to repay the borrowed funds, and how a HELOC lien might affect your future plans for your property.

We at HELOC360 provide tailored solutions and expert guidance to help you make informed decisions about your home's value and financial future. Our platform empowers you with the knowledge needed to leverage your home equity responsibly and effectively. A well-managed HELOC can become a powerful financial tool when used wisely and with a clear understanding of its implications.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.