How to Get a HELOC in 5 Simple Steps

Table of Contents

Wondering how to get a HELOC? You're in the right place. At HELOC360, we've broken down the process into five straightforward steps.

Whether you're a homeowner looking to tap into your equity or an investor seeking flexible financing, this guide will walk you through each stage of securing a Home Equity Line of Credit.

1. Assess Your Home Equity

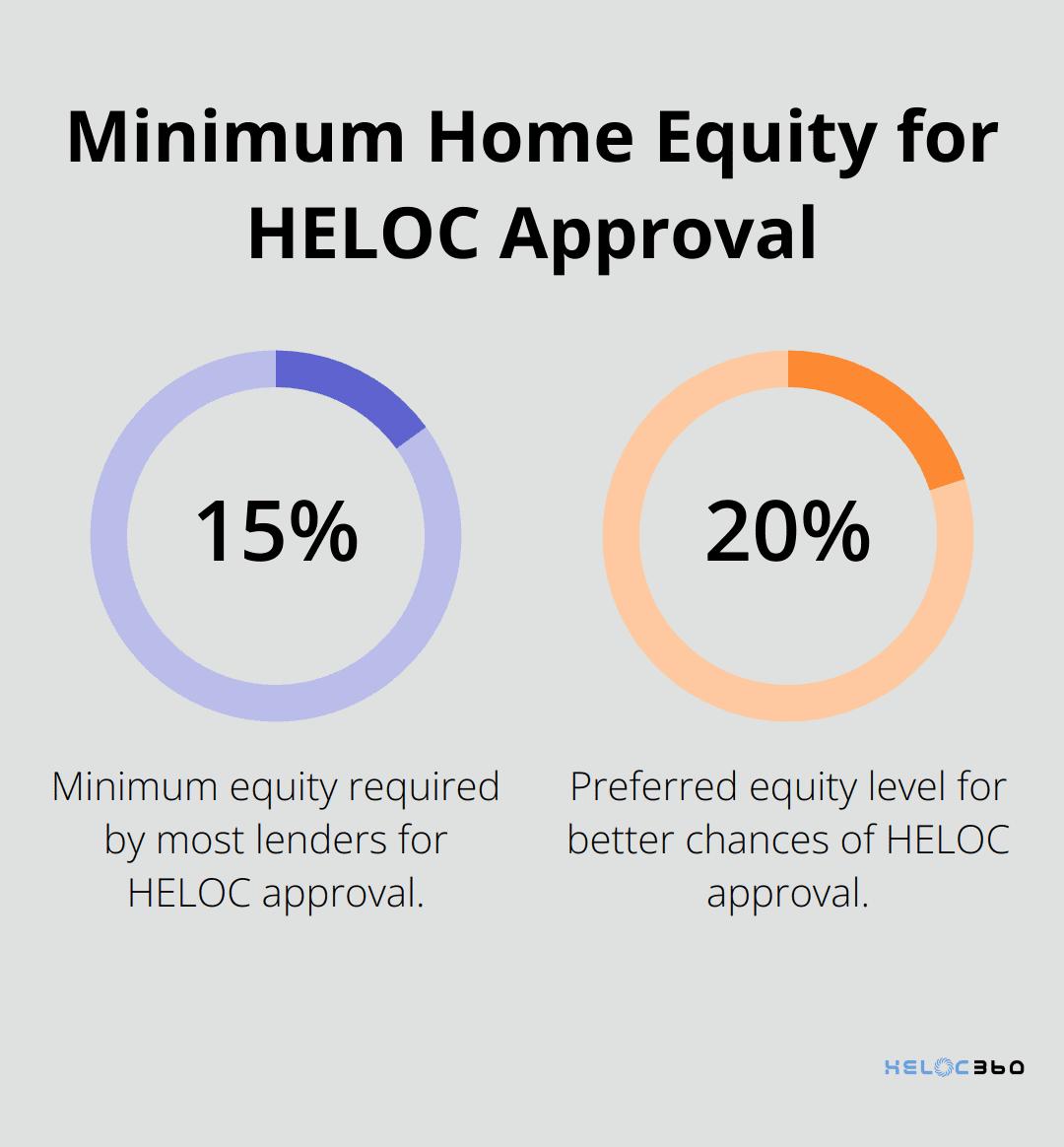

Determining your home equity is the first step in securing a HELOC. Start by estimating your home's current market value using online tools or consulting a local real estate agent. Then, check your most recent mortgage statement to find out how much you still owe on your home loan. The difference between these two figures is your home equity. Most lenders require at least 15% (preferably 20% or higher) equity for HELOC approval, so try to reach this benchmark.

To calculate your potential borrowing amount, consider that you can typically borrow up to 85% of your home's value, minus what you still owe on your primary mortgage and any secondary home loans. For example:

- Home value: $300,000

- Outstanding mortgage: $200,000

- Equity: $100,000 (33% of home's value)

- Potential HELOC amount: $55,000 (85% of $300,000 minus $200,000)

Your credit score, income, and debt-to-income ratio will also influence your borrowing capacity. A clear understanding of your home equity will help you move confidently to the next step: checking your credit score and financial health.

Use this calculator to estimate monthly home equity payments based on the amount you want, rate options, and other factors.

2. Evaluate Your Financial Health

Check your credit score before you apply for a HELOC. While some lenders may approve a borrower with a minimum credit score of 620, others may prefer a higher score of around 680. You can obtain free weekly online credit reports from each of the three major credit bureaus through AnnualCreditReport.com. Review these reports for any errors that could negatively impact your score and dispute them if necessary.

Calculate your debt-to-income (DTI) ratio by dividing your monthly debt payments by your gross monthly income. Lenders typically prefer a DTI ratio of 43% or lower for HELOC applicants. If your DTI is higher, try to pay down some existing debts before you apply. Collect recent pay stubs, tax returns, and bank statements to prove your income and assets. These documents will be essential when you submit your HELOC application (and can speed up the process).

Now that you've assessed your financial health, it's time to explore your options. The next step involves researching and comparing HELOC lenders to find the best fit for your needs.

3. Find the Best HELOC Lender for Your Needs

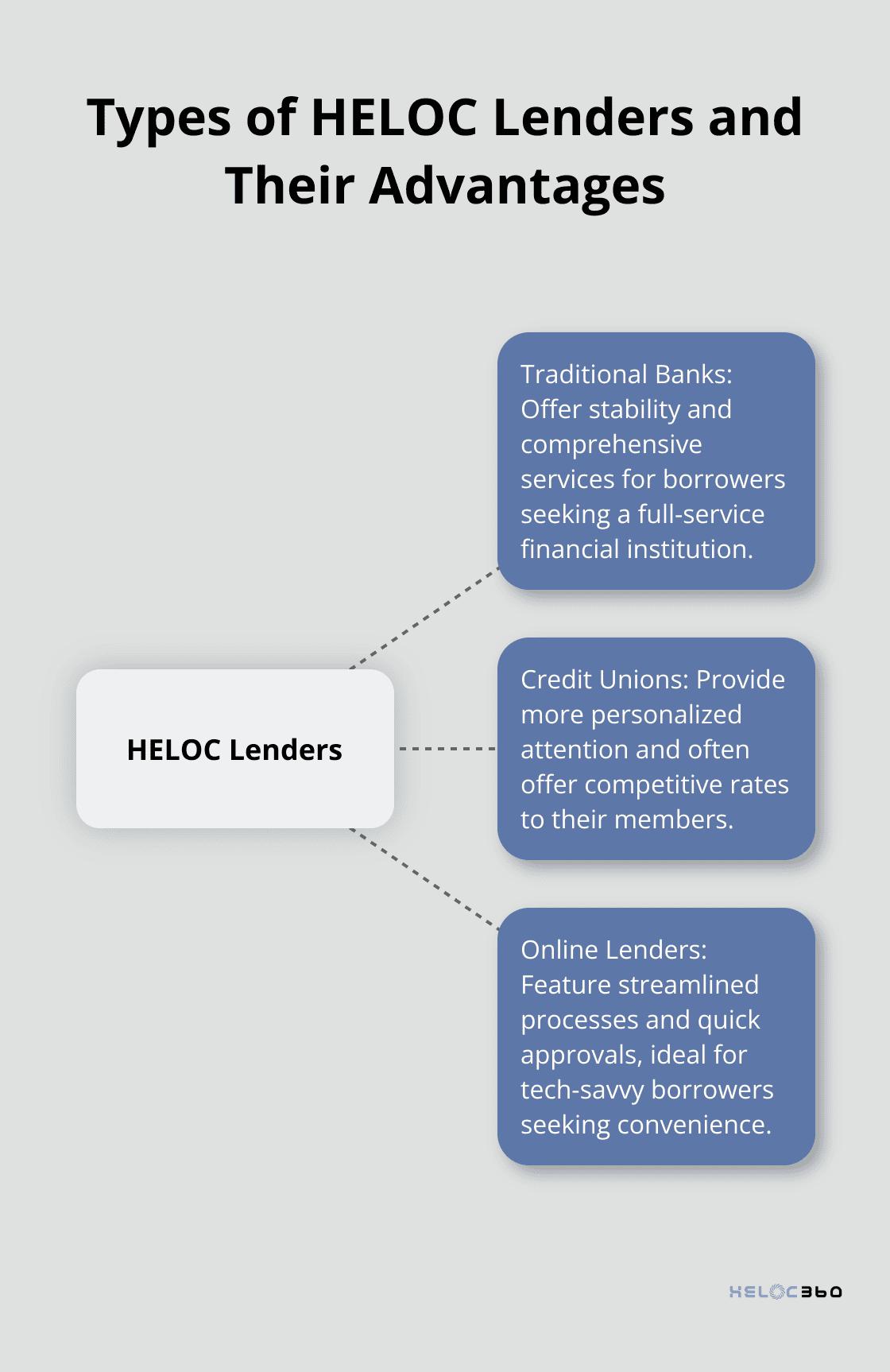

Selecting the right HELOC lender plays a key role in securing favorable terms and a smooth borrowing experience. You should explore offerings from various financial institutions, including traditional banks, credit unions, and online lenders. Each type of lender offers unique advantages: banks provide stability and comprehensive services, credit unions often offer more personalized attention and competitive rates, while online lenders typically feature streamlined processes and quick approvals.

To find the most advantageous deal, you need to compare interest rates, fees, and terms across multiple lenders. Pay special attention to the annual percentage rate (APR), which reflects the true cost of borrowing (including both interest and fees).

Customer service and reputation should not be overlooked when choosing a HELOC lender. Read customer reviews and ratings on trusted financial websites to understand the experiences of other borrowers. Look for lenders with a history of transparent communication, responsive customer support, and fair lending practices. Consider using comparison tools available on financial websites to quickly assess multiple lenders side-by-side. While many options exist, HELOC360 stands out as a resource for comparing HELOCs. HELOCs differ from traditional loans in several ways, including using your home as collateral, which can result in lower interest rates compared to personal loans. However, you should always evaluate multiple options to ensure you get the best deal for your specific financial situation. As you narrow down your choices, you'll want to start preparing the necessary documentation for your HELOC application.

4. Prepare Your HELOC Documentation

Collect all necessary paperwork to streamline your HELOC application process. Start with pay stubs for the past month showing year-to-date income and other proof of income, such as tax returns or Form W-2, to demonstrate your income stability. Self-employed applicants should gather profit and loss statements and business tax returns. Include property-related documents such as your current mortgage statement, property tax bill, and homeowners insurance policy. These items help lenders assess your home's value and equity position. Don't forget to compile bank statements from recent months and information on other assets or investments.

Create a digital folder with scanned copies of all documents for easy online application submission. This organization ensures you won't miss any essential paperwork and allows for quick uploads. Some lenders might request additional information, so keep your financial records easily accessible. A thorough and organized approach to documentation demonstrates your financial responsibility to potential lenders and speeds up the approval process. Your preparation sets the stage for the final step: submitting your HELOC application with confidence.

5. Submit Your HELOC Application and Await Approval

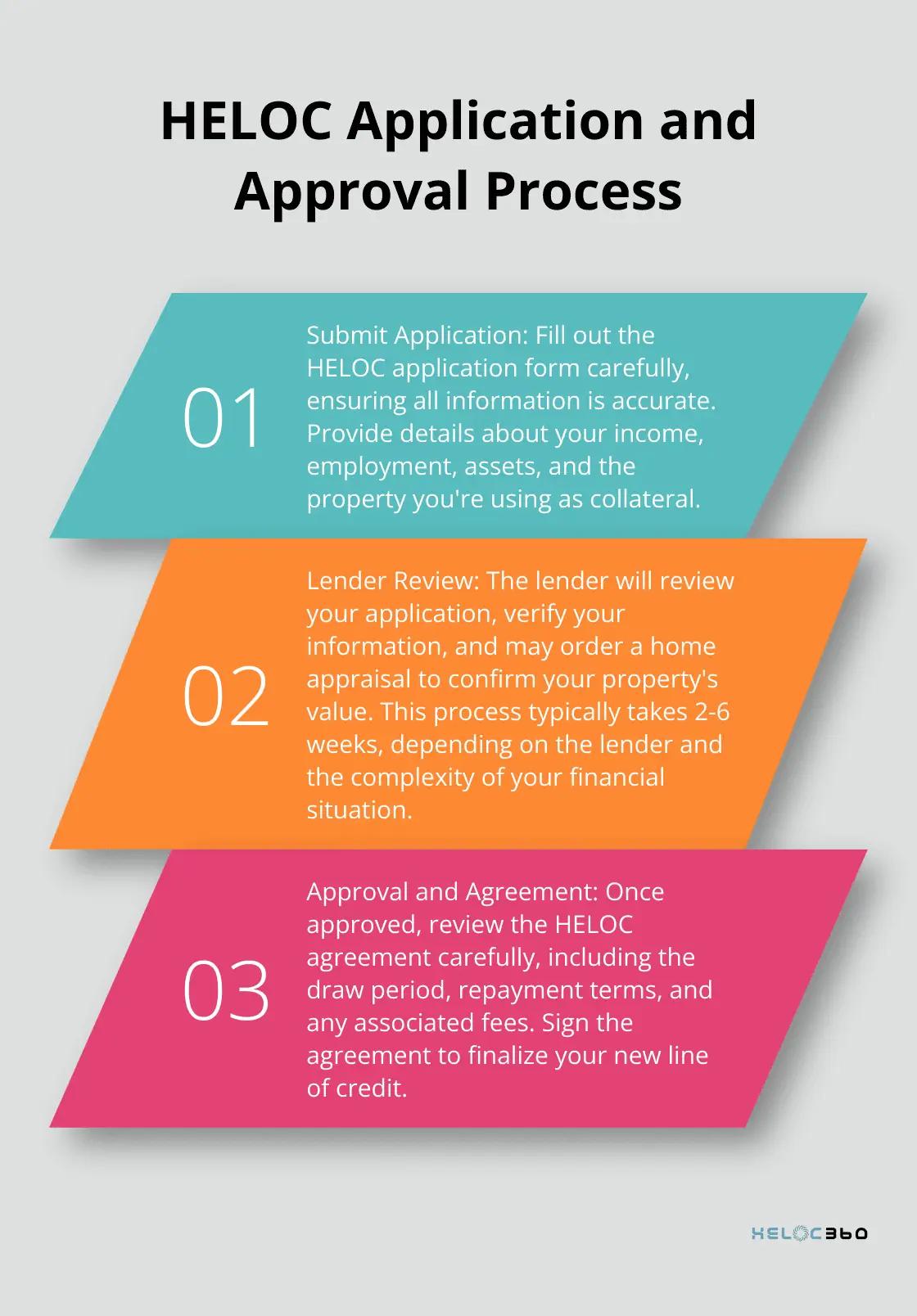

Select your preferred lender based on your research and start the HELOC application process. Many lenders offer online applications, which can speed up the process significantly. Fill out the application form carefully, ensuring all information is accurate to avoid delays. Provide details about your income, employment, assets, and the property you're using as collateral. Upload or submit all the required documentation you've gathered, including proof of income, property information, and financial statements.

After submission, the lender will review your application, verify your information, and may order a home appraisal to confirm your property's value. The approval process typically takes 2–6 weeks, depending on the lender and the complexity of your financial situation. While waiting, avoid making major financial changes or applying for new credit, as this could impact your application. Once approved, review the HELOC agreement carefully, including:

- Draw period

- Repayment terms

- Any associated fees

Sign the agreement to finalize your new line of credit. With your HELOC secured, you're now ready to leverage your home equity for your financial goals. However, be aware that using your home as collateral means the lender could foreclose on it if you don't repay what you borrow.

Final Thoughts

Getting a HELOC doesn't have to be complex. We at HELOC360 simplify the process, offering expert guidance and connecting you with lenders that match your unique needs. Our platform helps you navigate the HELOC landscape efficiently, understanding that every homeowner's situation differs.

A HELOC can be a powerful tool to achieve your financial goals. You can use it for home improvements, debt consolidation, or creating financial flexibility. The key is to use this financial tool wisely to improve your overall financial situation.

Now that you know how to get a HELOC, it's time to take action. Don't let your home's equity sit idle—explore your options today and take the first step towards financial empowerment. With the right approach and resources, you can turn your home's value into a powerful asset for your future.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.