Why Refinancing Your HELOC Might Be a Game-Changer

Table of Contents

HELOC refinancing can be a powerful financial move for homeowners. At HELOC360, we've seen how this strategy can transform our clients' financial situations.

This post will explore why refinancing your HELOC might be the right choice for you. We'll cover the benefits, ideal timing, and key considerations to help you make an informed decision.

What Is HELOC Refinancing?

The Basics of HELOC Refinancing

HELOC refinancing is a strategic financial move that can transform your home equity borrowing. It involves the replacement of your existing Home Equity Line of Credit (HELOC) with a new one, often offering more favorable terms.

The Refinancing Process Explained

When you refinance your HELOC, you take out a new line of credit to pay off the existing one. This process differs from initial HELOC borrowing in several ways. You already understand how HELOCs work, which can streamline the refinancing process. Moreover, your home's value may have changed since you first took out the HELOC, potentially affecting your borrowing capacity.

Common Motivations for Refinancing

Homeowners consider HELOC refinancing for various reasons. A primary motivation is to secure a lower interest rate. HELOC rates have been affected by the Fed's rate cuts in 2024, making tapping home equity cheaper.

Another reason to refinance is to extend the draw period. If you approach the end of your current draw period, refinancing can provide more time to access funds. This can benefit those with ongoing projects or anticipated future expenses.

Enhancing Financial Flexibility

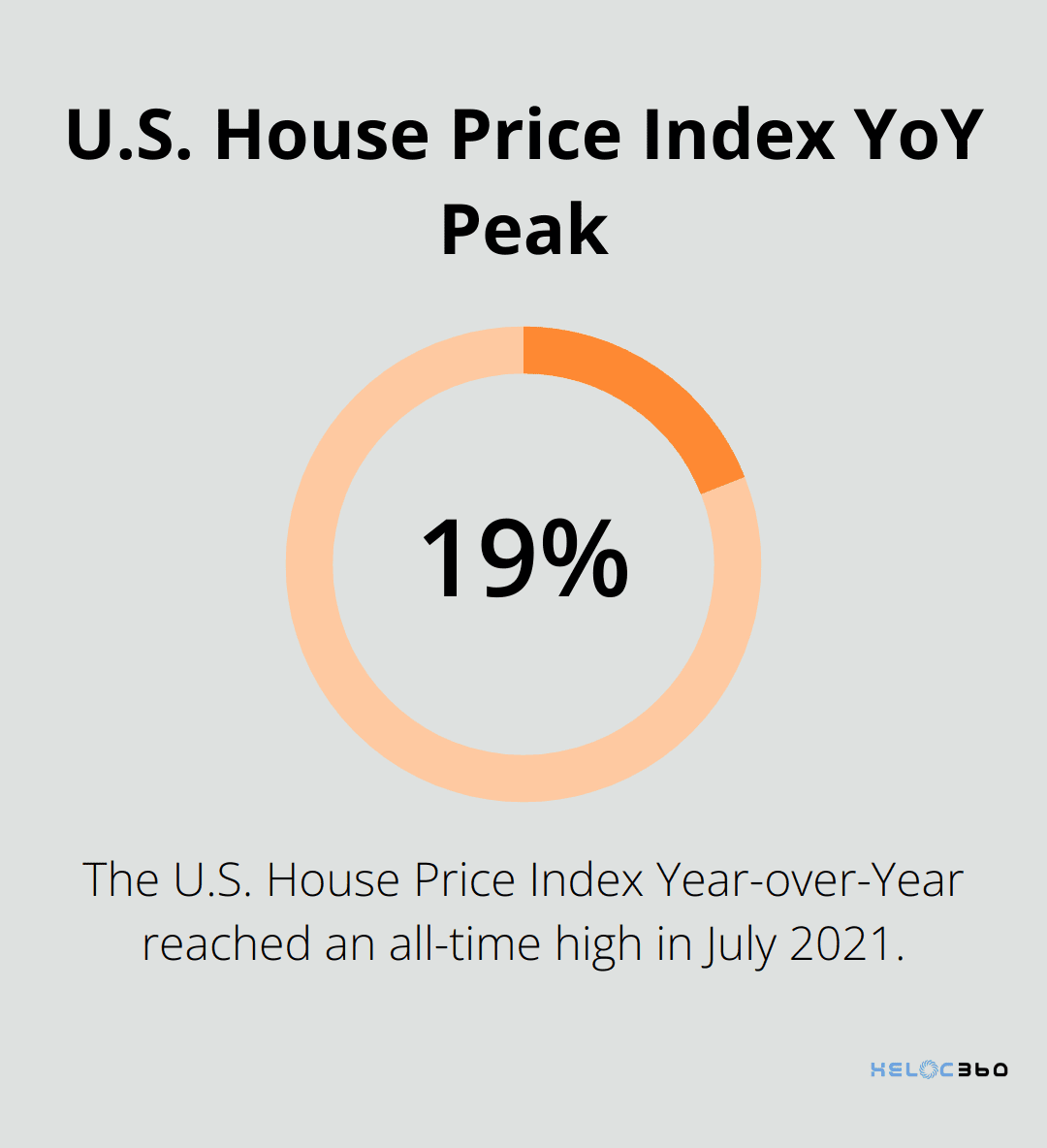

Refinancing offers an opportunity to increase your credit limit. House prices in the United States have seen significant changes, with the House Price Index YoY reaching an all-time high of 19.10 percent in July of 2021, according to Trading Economics. This allows many homeowners to tap into more equity. However, lenders don't automatically increase credit limits. You must request a modification or apply for a new HELOC to access this increased equity.

Some homeowners refinance to switch from a variable to a fixed interest rate. This change can provide more predictable monthly payments, especially in a rising rate environment. Fixed-rate HELOCs often come with slightly higher initial rates, so it's important to weigh the long-term benefits against short-term costs.

Key Considerations Before Refinancing

Before you decide to refinance, evaluate your current financial situation and future goals. Consider factors like your credit score, which can impact the rates you're offered, and any fees associated with refinancing. These can include application fees and closing costs which can range from 1-5% of the total loan amount.

It's also worth noting that refinancing may reset your repayment timeline. While this can lower your monthly payments in the short term, it could result in higher interest payments over the life of the loan. Always calculate the total cost of borrowing before making a decision.

As you weigh the pros and cons of HELOC refinancing, it's essential to understand the potential benefits this financial move can offer. Let's explore these advantages in more detail in the next section.

How HELOC Refinancing Can Boost Your Financial Health

Lower Interest Rates: A Path to Savings

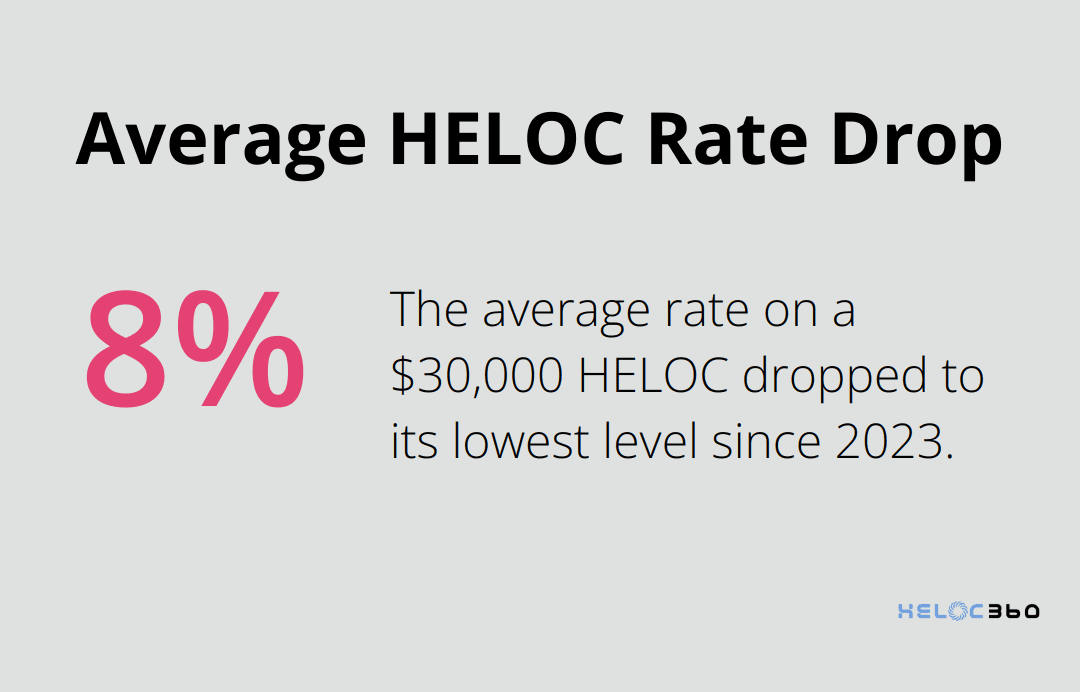

HELOC refinancing offers homeowners a chance to secure lower interest rates. According to recent data, the average rate on a $30,000 HELOC dropped to 8.01 percent, its lowest level since 2023. This decrease translates to substantial savings for homeowners with existing HELOCs.

Extended Financial Flexibility

Refinancing resets the clock on your HELOC's draw period. Most HELOCs have a 10-year draw period, but refinancing can extend this timeframe. This extension proves valuable for long-term projects or anticipated future expenses. For example, refinancing four years into your current HELOC could potentially add six more years of draw time.

Increased Home Equity Access

Recent years have seen changes in home values. The Case-Shiller index, which lags reality on the ground by 4-6 months, has started to pick up price drops in some areas, particularly in the West. This fluctuation in home values can affect the amount of equity homeowners can access through refinancing.

Payment Stability Through Fixed Rates

Switching from a variable to a fixed interest rate provides more predictable monthly payments. While fixed rates typically start slightly higher than variable rates, they protect against potential rate increases. This stability aids in budgeting and long-term financial planning.

Weighing Costs and Benefits

While the benefits of refinancing can be substantial, it's important to consider the associated costs. Closing fees range from $750 to $6,685, depending on line amount and state law requirements. These typically include origination fees (3.5% of line amount) and other costs. Try to calculate the break-even point to ensure the benefits outweigh the costs.

As you consider the potential advantages of HELOC refinancing for your financial health, it's equally important to understand when this strategy might be most beneficial. Let's explore the optimal timing for HELOC refinancing in the next section.

When to Refinance Your HELOC

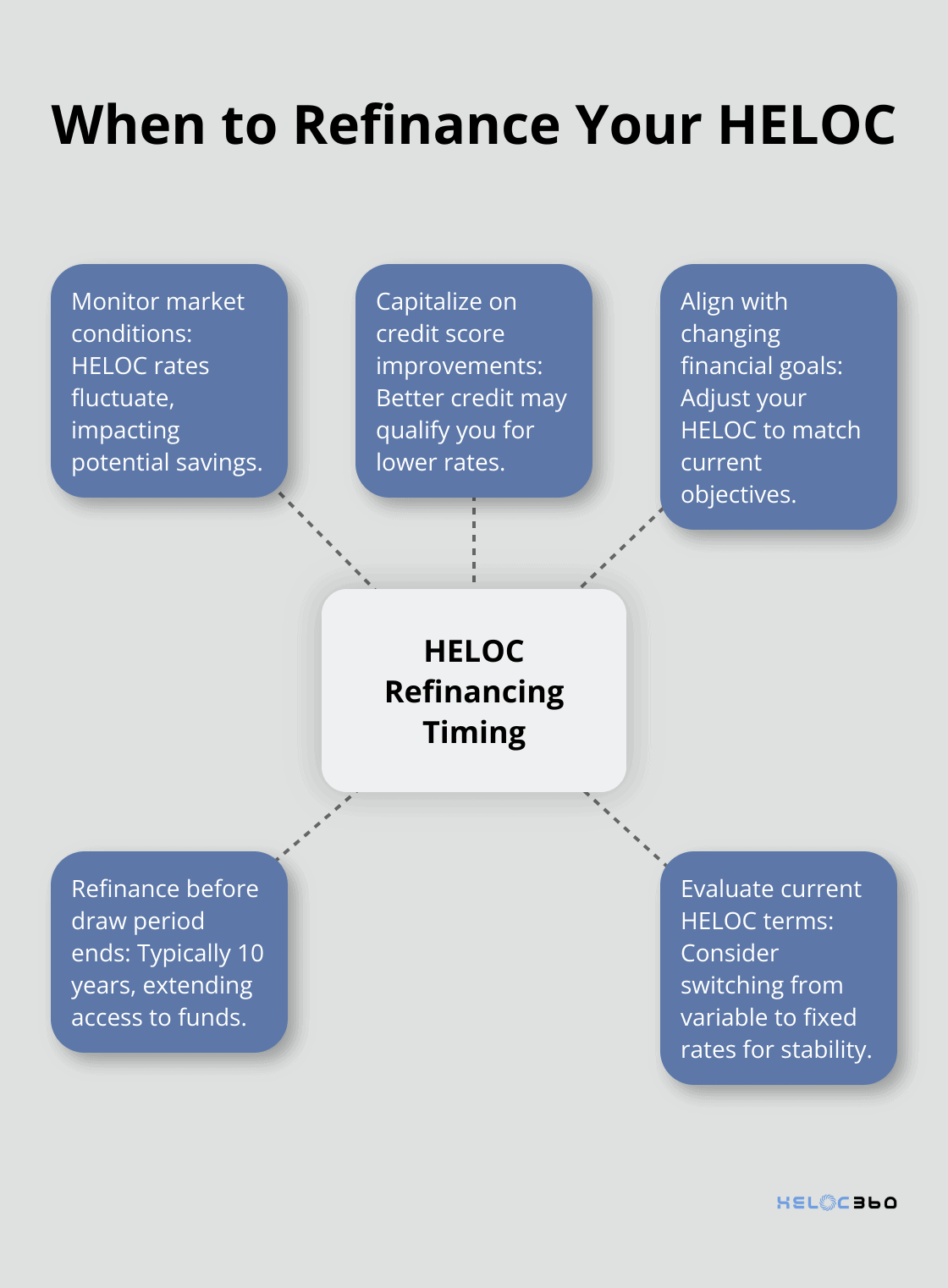

Monitor Market Conditions

The timing of your HELOC refinance can significantly impact your savings. Market trends play a key role in determining favorable refinancing opportunities. Freddie Mac reports that HELOC rates have fluctuated recently. According to their records, the average 30-year rate reached 6.48% during the initial week of 2023, increasing steadily afterwards. This trend presents an opportunity for homeowners to consider refinancing and potentially save on interest over their HELOC's lifetime.

Capitalize on Credit Score Improvements

Your credit score heavily influences your HELOC terms. A higher score since your initial HELOC might qualify you for better rates. Research suggests that changes in credit scores can impact loan prepayment behavior, which could affect refinancing decisions.

Align with Changing Financial Goals

Financial needs evolve over time. You might have opened a HELOC for home renovations but now consider using it for debt consolidation or education expenses. Refinancing allows you to adjust your HELOC to match your current financial objectives. If you need a larger credit line, refinancing can help you access more of your home's equity, especially if your property value has increased.

Refinance Before Draw Period Ends

Most HELOCs feature a 10-year draw period. As this period nears its end, consider refinancing to extend your access to funds. This step becomes particularly important if you anticipate future borrowing needs. Refinancing before the repayment period starts can help you avoid a sudden increase in monthly payments, which typically occurs when you transition from interest-only to principal-plus-interest payments.

Evaluate Your Current HELOC Terms

Take a close look at your existing HELOC terms. If you have a variable interest rate, you might benefit from switching to a fixed rate through refinancing. This change can provide more predictable monthly payments and protect you from potential rate increases. Additionally, if your current HELOC has unfavorable terms or high fees, refinancing offers an opportunity to shop around for better options.

Final Thoughts

HELOC refinancing offers homeowners a powerful tool to optimize their financial strategy. It provides potential benefits such as lower interest rates, extended draw periods, increased credit limits, and the option to switch to fixed rates. These advantages can significantly impact your financial health and create new opportunities for wealth building.

The decision to refinance your HELOC requires careful evaluation of your personal financial situation. You must consider factors like your credit score, home value, and long-term financial goals. Market conditions, improved creditworthiness, and changes in financial objectives also play a role in determining the right time to refinance.

At HELOC360, we understand the complexities of HELOC refinancing and aim to simplify the process. Our platform provides expert guidance tailored to your unique needs, helping you unlock the full potential of your home equity. If you're considering HELOC refinancing, visit HELOC360 to access the tools and knowledge you need to make an informed decision.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.