Funding Your Business Dreams With a HELOC

Table of Contents

Are you ready to turn your entrepreneurial dreams into reality? A Home Equity Line of Credit (HELOC) might be the key to unlocking your business potential.

At HELOC360, we've seen countless entrepreneurs use HELOCs to fund their business ventures successfully. This flexible financing option can provide the capital you need to start, grow, or expand your business.

In this post, we'll explore how a HELOC for business can fuel your entrepreneurial journey and share strategies to make the most of this powerful financial tool.

How a HELOC Powers Your Business

Unleashing Your Home's Potential

A Home Equity Line of Credit (HELOC) allows you to borrow money as you need it at a relatively lower interest rate. When you open a HELOC, your lender approves a credit limit based on your home's value and your outstanding mortgage balance. You can then draw from this line of credit as needed, paying interest only on the amount you use.

This flexibility revolutionizes cash flow management for business owners. For instance, if you receive approval for a $100,000 HELOC and use $20,000 for inventory purchases, you'll only pay interest on that $20,000. This approach can lead to significant savings compared to taking out a lump-sum loan for the full amount.

Lower Rates, Higher Profits

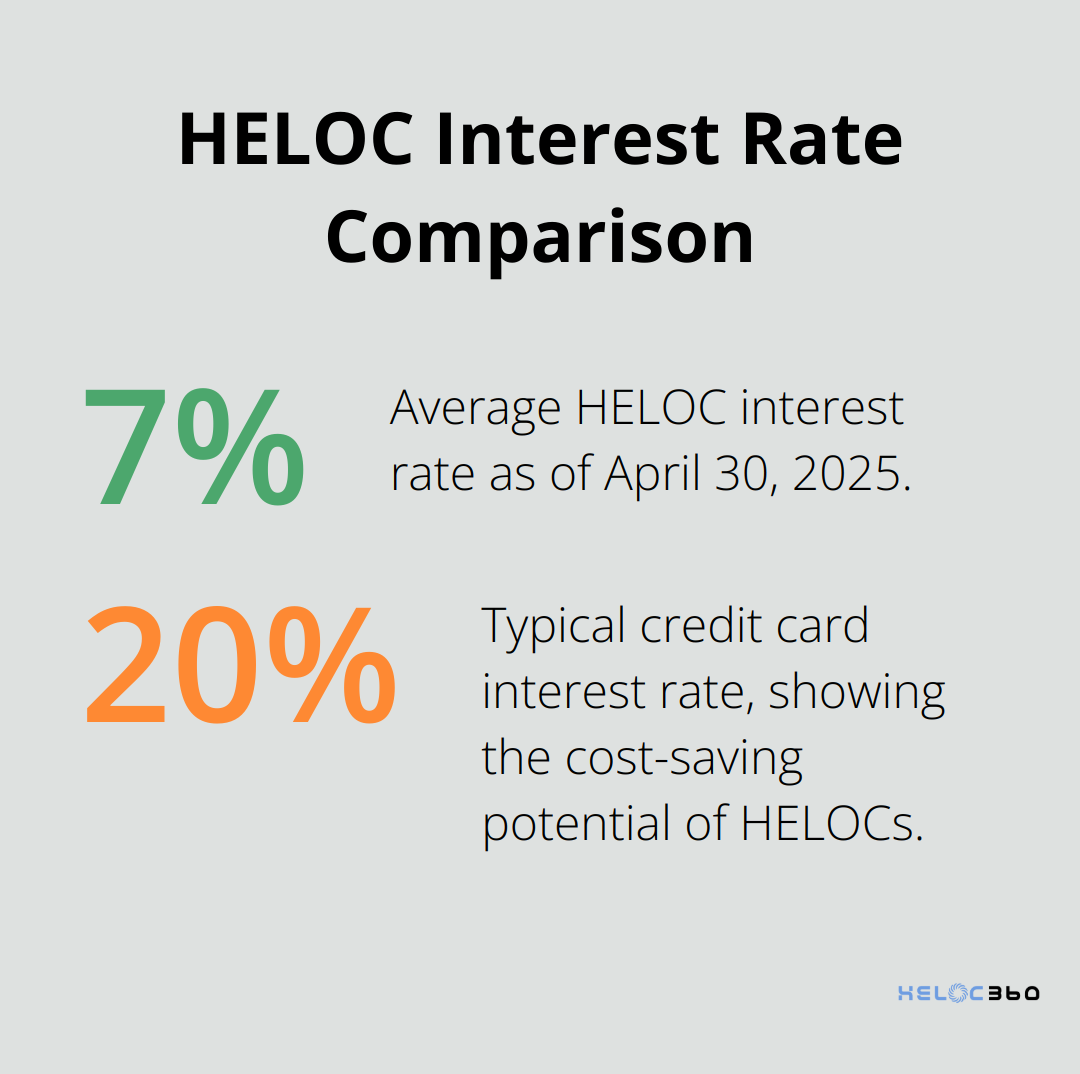

One of the most compelling advantages of using a HELOC for business financing is the interest rate. HELOCs typically offer lower rates than credit cards or unsecured business loans. According to Bankrate's latest survey of the nation's largest home equity lenders, as of April 30, 2025, the national average HELOC interest rate is 7.95%.

This difference translates to substantial savings over time. On a $50,000 balance, you could save over $4,000 in interest annually by choosing a HELOC over a credit card (a difference that can significantly impact your bottom line).

Flexibility Trumps Rigidity

Traditional business loans often come with strict terms and usage restrictions. In contrast, a HELOC provides the freedom to use funds as you see fit. You can cover payroll during a slow month, invest in new equipment, or launch a marketing campaign - your HELOC supports all your business needs.

Moreover, the revolving nature of a HELOC allows you to borrow, repay, and borrow again without reapplying. For businesses with cyclical sales or uneven revenue streams, a revolving line of credit can smooth out cash flow during lean periods.

Strategic Use of Home Equity

While HELOCs offer numerous benefits, it's important to approach them with a solid plan. Your home's equity is a valuable asset – with the right approach, it can become the catalyst for your business success.

The key lies in understanding how to leverage your home equity responsibly. This involves careful planning, regular financial reviews, and a clear strategy for using and repaying the funds.

As we move forward, we'll explore specific strategies for using a HELOC to fund your business dreams, ensuring you make the most of this powerful financial tool.

How to Leverage a HELOC for Business Success

Jumpstart Your Business with Initial Funding

A Home Equity Line of Credit (HELOC) can provide the capital you need to start your business. HELOCs can have lower interest rates than those for other business lending sources. Keep in mind your personal residence is securing the line of credit.

Use your HELOC to fund essential startup costs like inventory, equipment, or marketing. For example, if you open a small retail store, you might use $10,000 from your HELOC for initial inventory, $5,000 for point-of-sale systems, and $3,000 for your first marketing campaign.

Navigate Cash Flow Challenges

Cash flow management can make or break a business. A HELOC can serve as a financial buffer during lean periods or seasonal fluctuations.

If you run a landscaping business, you might experience slower winter months. Use your HELOC to cover operational costs during this time, ensuring you can pay employees and maintain equipment. When spring arrives and business picks up, you can repay the borrowed amount.

Fuel Business Growth and Expansion

As your business grows, so do your financial needs. A HELOC offers flexible financial help, whether you need to invest in a new marketing campaign, pay payroll during a sluggish month, or buy new equipment.

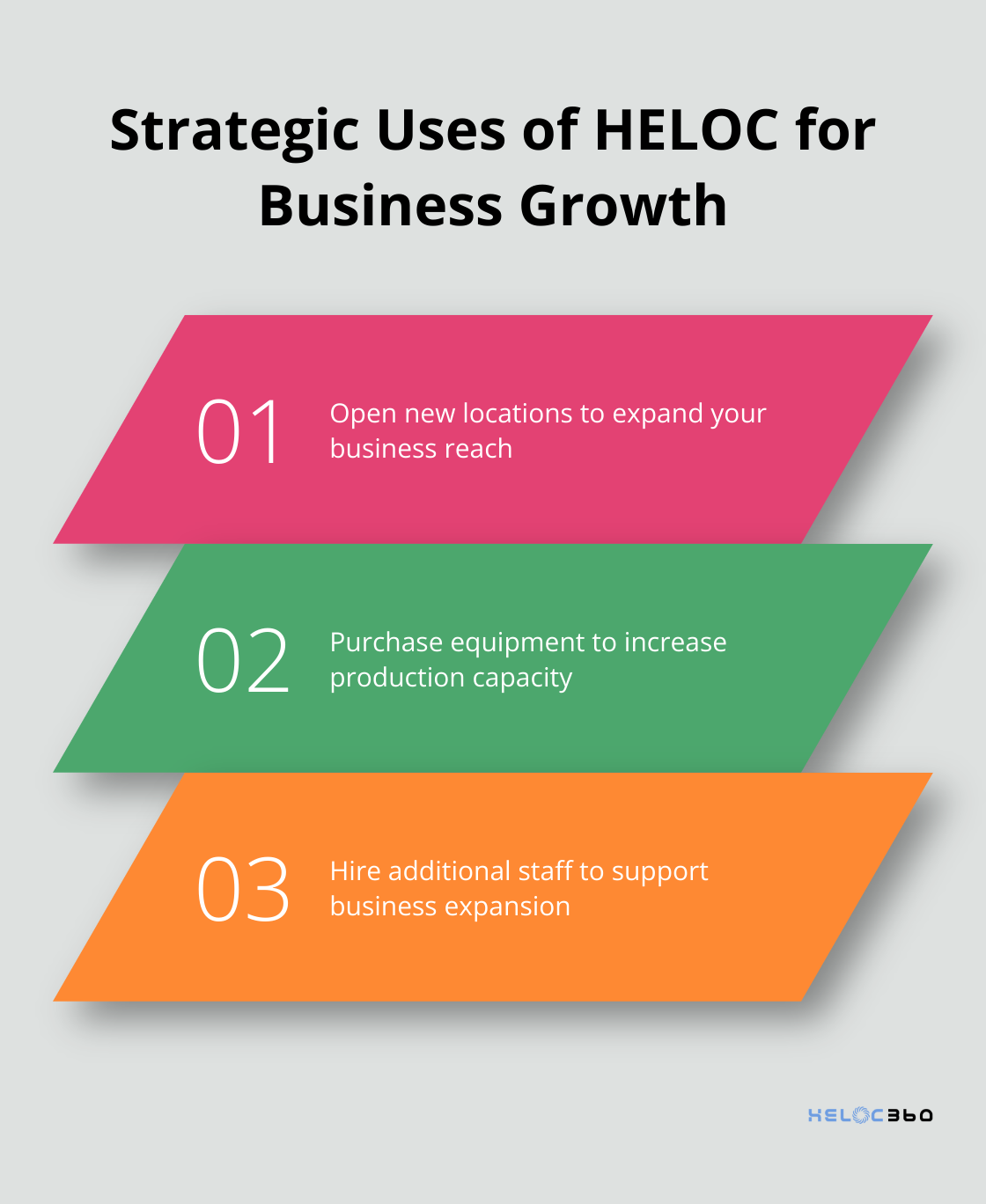

Consider using your HELOC to:

- Open a new location: If you run a successful coffee shop, use your HELOC to fund the down payment on a second location.

- Purchase equipment: Invest in new machinery to increase production capacity. For example, a small manufacturing business could use a $50,000 HELOC draw to purchase a new CNC machine (potentially doubling output).

- Hire additional staff: Use your HELOC to cover payroll for new employees until revenue catches up with expanded operations.

- Launch new products: Fund research, development, and initial production runs for new offerings.

Create a Strategic Repayment Plan

While a HELOC offers flexibility and lower interest rates, you must have a solid repayment plan. Always consider the potential return on investment before using your HELOC for business purposes. Try to align your repayment schedule with your business's cash flow cycles.

For instance, if you use your HELOC to purchase inventory for a seasonal business, plan to repay the borrowed amount after your peak sales period. This strategy ensures you can meet your HELOC obligations without straining your business finances.

Seek Expert Guidance

Navigating the world of HELOCs and business finance can be complex. Platforms like HELOC360 can provide valuable insights and connect you with lenders that fit your unique needs. (These services can help you make informed decisions about using your home equity for business purposes.)

As you explore the possibilities of using a HELOC for your business, it's important to understand the potential risks involved. Let's examine how to mitigate these risks and use your HELOC responsibly in the next section.

How to Manage HELOC Risks

Understand Your Financial Obligations

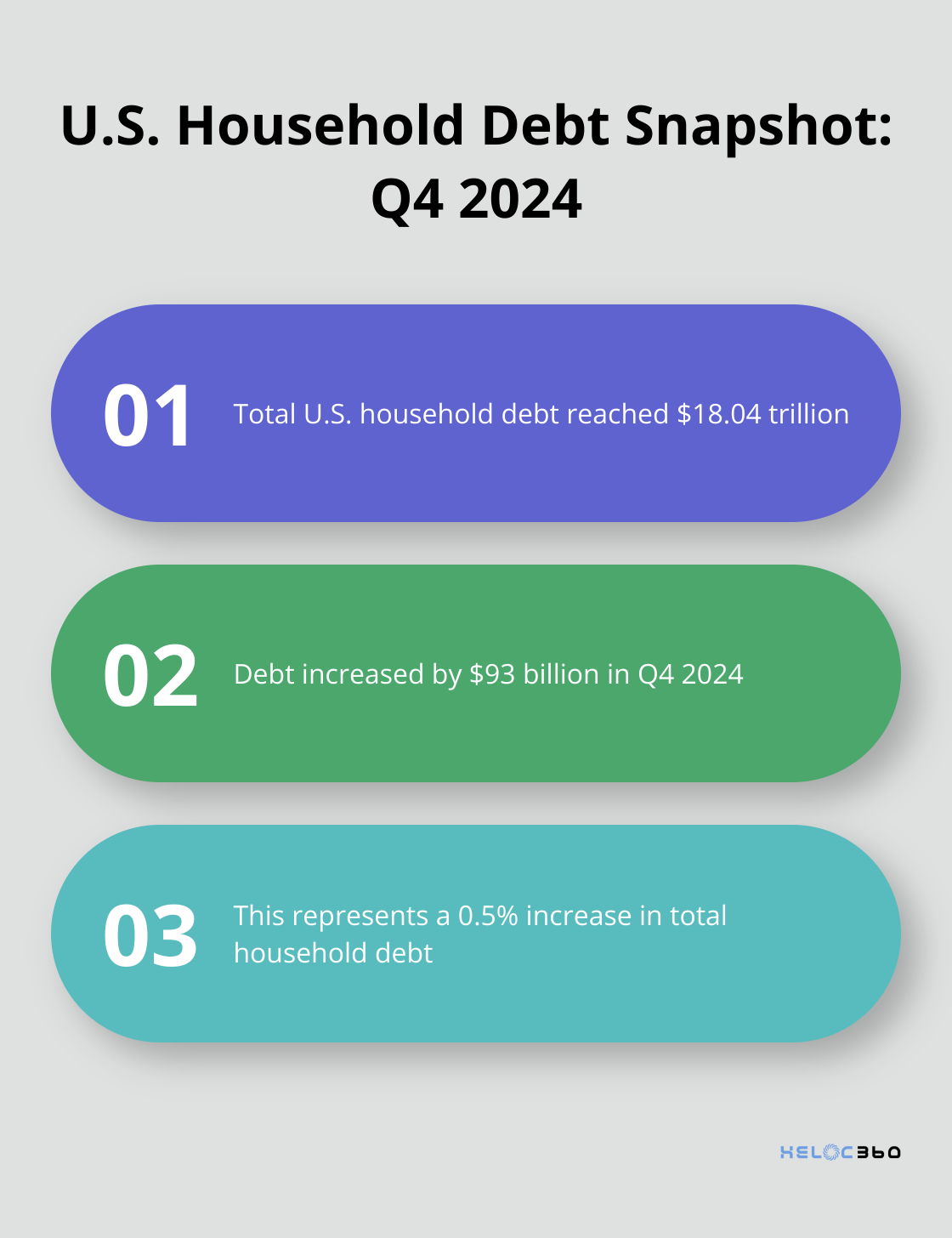

A Home Equity Line of Credit (HELOC) secured by your home carries significant responsibility. Defaulting on payments puts your house at risk. The Federal Reserve Bank of New York reported that total household debt increased by $93 billion (0.5%) in Q4 2024, to $18.04 trillion. This statistic highlights the need for meticulous financial planning.

To minimize this risk, create a comprehensive budget that includes both business and personal expenses. Factor HELOC payments into your projections and maintain a reserve for unexpected costs. Financial management tools (such as QuickBooks or Xero) can help you track your finances with precision.

Prepare for Interest Rate Changes

HELOCs typically feature variable interest rates, which means your payments can increase as rates rise. HELOC rates fell for much of 2024, with a substantial decline over the past seven months. To safeguard against potential future increases, set aside a portion of your monthly profits to cover potential rate hikes.

Some lenders provide rate caps or the option to convert part of your HELOC to a fixed-rate loan. Explore these options with your lender to add an extra layer of financial protection.

Keep Personal and Business Finances Separate

Combining personal and business finances can result in tax complications and obscure your business's true financial health. Open a dedicated business checking account and use it exclusively for your HELOC funds and business transactions.

Form a Limited Liability Company (LLC) or corporation to further separate your personal assets from your business liabilities. Forbes Advisor reports that out of the 33.3 million small businesses in the country, 27.1 million are managed solely by their owners and do not employ any additional staff, potentially exposing owners to personal liability.

Develop a Robust Repayment Plan

Craft a clear repayment strategy before you start using your HELOC. Try to pay more than the minimum required payment when possible. If your business experiences seasonal fluctuations, schedule larger payments during your high-income periods.

Establish specific repayment milestones. For instance, if you use $50,000 from your HELOC to purchase equipment, create a plan to repay that amount within a set timeframe based on the expected return on investment from the equipment.

Watch Your Credit Utilization

Your credit score can fluctuate based on how much of your available HELOC you use. Credit experts generally recommend keeping your credit utilization below 30%. If you need to use more, plan to pay it down quickly.

Check your credit report regularly. Identifying and correcting errors can help maintain a healthy credit score, which is essential for future financing needs.

Final Thoughts

A HELOC for business funding offers a powerful way to turn entrepreneurial dreams into reality. This financial tool provides access to flexible, low-interest financing that can fuel business growth, from covering startup costs to managing cash flow and expanding operations. However, the benefits of using a HELOC for your business come with responsibilities, which require careful financial planning, diligent risk management, and a solid repayment strategy.

Your home secures a HELOC, which underscores the importance of responsible borrowing and thorough financial planning. Every business decision should factor in potential returns and risks. HELOC360 offers valuable support for those ready to explore the possibilities of using a HELOC for their business ventures (our platform simplifies the process of leveraging home equity).

HELOC360 provides expert guidance and connects you with lenders that match your specific needs. We help you make informed decisions about using your home's value to achieve your business goals. The financial power of a HELOC, combined with responsible management and strategic planning, can create a solid foundation for your business success.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.