HELOC vs Home Equity Loan: Understanding the Differences

Table of Contents

Homeowners often face a crucial decision when tapping into their home equity: HELOC vs home equity loan. These two financial tools offer distinct advantages and drawbacks.

At HELOC360, we understand the importance of making an informed choice. This guide will break down the key differences between HELOCs and home equity loans, helping you determine which option best suits your financial needs.

What Is a HELOC?

Definition and Basic Features

A Home Equity Line of Credit (HELOC) allows homeowners to access their home's equity as a flexible borrowing option. It functions similarly to a credit card, providing a revolving line of credit that you can use as needed. Consider a HELOC if you are confident you can keep up with the loan payments. If you fall behind or can't repay the loan on schedule, you could lose your home.

How HELOCs Work

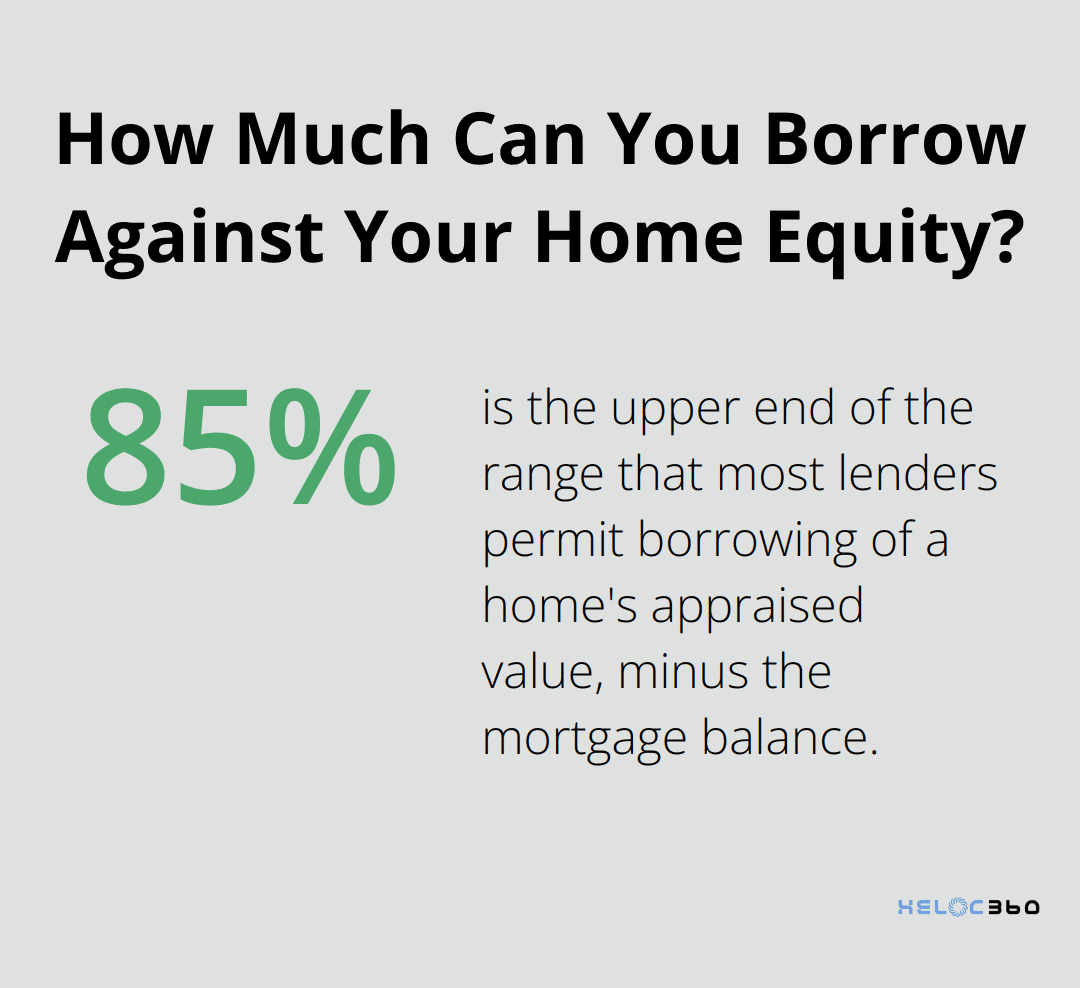

When you apply for a HELOC, lenders determine your credit limit based on your home's value and outstanding mortgage balance. Most lenders permit borrowing up to 80-85% of your home's appraised value, minus your mortgage balance.

HELOCs operate in two phases:

- Draw Period: This phase typically lasts up to 10 years. During this time, you can borrow funds up to your credit limit and are usually only required to pay interest on what you borrow.

- Repayment Period: After the draw period ends, you can no longer borrow funds. You must repay both principal and interest during this phase.

A key characteristic of HELOCs is their variable interest rates (often tied to the prime rate). This means your payments may change over time. As of February 5, 2025, Bankrate reports the average HELOC rate at 8.28%, near its lowest level in almost two years.

Common Uses for HELOCs

HELOCs offer versatility for various financial needs:

- Home Improvements: Many homeowners use HELOCs to fund renovations. For example, a $30,000 kitchen remodel could potentially increase a home's value by $20,000 to $25,000 (according to Remodeling Magazine's Cost vs. Value report).

- Debt Consolidation: HELOCs can help consolidate high-interest debts. If you have $20,000 in credit card debt at 18% APR, using a HELOC at 8.28% could result in significant interest savings.

- Education Expenses: Parents often use HELOCs to fund their children's education costs.

- Emergency Funds: HELOCs provide a safety net for unexpected expenses.

- Business Investments: Entrepreneurs may use HELOCs to fund business ventures or expansions.

While HELOCs offer numerous advantages, it's important to note that your home serves as collateral. Missed payments could put your property at risk of foreclosure. This underscores the importance of understanding all aspects of HELOCs and finding a reputable lender that aligns with your needs.

As we move forward, let's explore another popular option for accessing home equity: home equity loans. Understanding the differences between these two financial tools will help you make an informed decision about which option best suits your financial goals.

What Are Home Equity Loans?

Definition and Basic Features

Home equity loans allow homeowners to borrow against the value of their property. These loans offer predictable payments and tax advantages, but come with risks like potential property loss and fees. Unlike HELOCs, home equity loans provide a lump sum upfront, which makes them suitable for large, one-time expenses.

Fixed Rates and Predictable Payments

A key advantage of home equity loans is their fixed interest rates. Over the past three years, home equity loans have become a popular alternative for borrowing, since they carry lower interest rates than other types of loans. This fixed rate ensures consistent monthly payments throughout the loan term, which typically ranges from 5 to 30 years.

Loan-to-Value Considerations

Lenders usually permit borrowing up to 80-85% of your home's value, minus your existing mortgage balance. This is known as the loan-to-value (LTV) ratio. For instance, if your home is worth $300,000 and you owe $200,000 on your mortgage, you might qualify to borrow up to $55,000 (85% of $300,000, minus $200,000).

Popular Uses for Home Equity Loans

Home equity loans often serve various purposes:

- Major Home Renovations: The National Association of Realtors reports on both interior and exterior home improvement projects, providing cost recovery estimates for representative remodeling projects.

- Debt Consolidation: Consolidating high-interest debt with a home equity loan could potentially save you money in interest over time.

- Education Expenses: Many parents use home equity loans to fund their children's education.

- Large Purchases: Some homeowners use these loans for significant expenses like weddings or starting a business.

It's important to note that home equity loans use your home as collateral. This means defaulting on payments could put your property at risk. Always carefully consider your ability to repay before taking out any loan.

Now that we've explored home equity loans, let's compare them to HELOCs to help you determine which option might better suit your financial needs.

Which Option Fits Your Financial Needs

Interest Rates and Repayment Terms

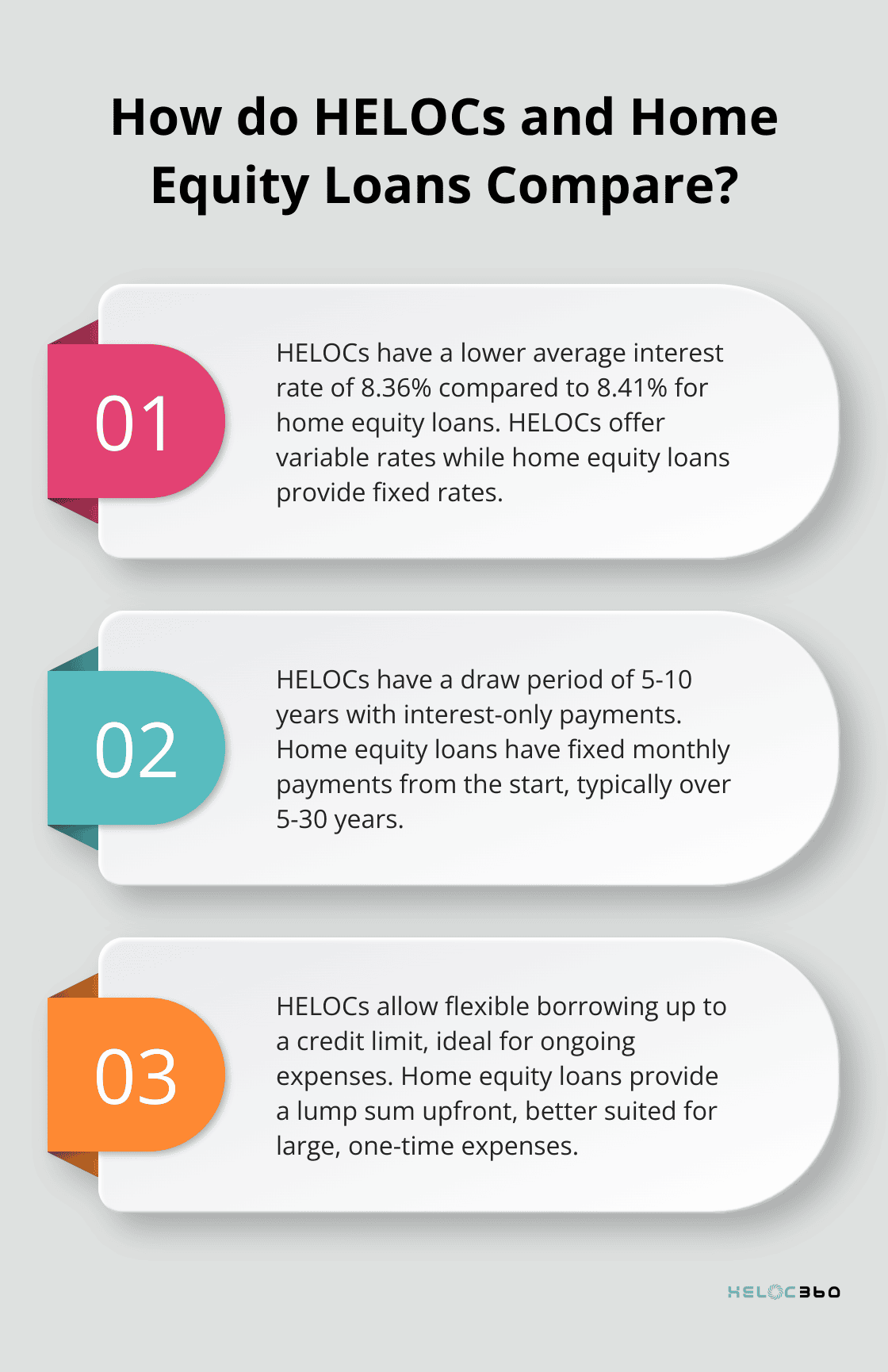

HELOCs and home equity loans differ in their interest rate structures and repayment terms. HELOCs have a lower interest rate than home equity loans (8.36% versus 8.41%), but it also has a significantly lower rate than many alternatives. Home equity loans provide fixed rates.

The repayment structure varies significantly between the two options. HELOCs have a draw period typically lasting from 5-10 years, with most lenders offering 10 years to draw from your line of credit. During this time, borrowers can access funds as needed and often make interest-only payments. After this period, borrowers enter the repayment phase, paying back both principal and interest. Home equity loans, in contrast, have fixed monthly payments from the start, typically over a 5 to 30-year term.

Borrowing Flexibility

HELOCs provide more flexibility in borrowing. Users can draw funds as needed up to their credit limit, similar to a credit card. This makes HELOCs ideal for ongoing expenses or projects with uncertain costs. Home equity loans provide a lump sum upfront, which suits large, one-time expenses better.

For instance, a home renovation project with unpredictable costs might benefit from a HELOC. You can draw funds as needed, potentially saving on interest for unused funds. Conversely, if you plan to consolidate a known amount of debt, a home equity loan's lump sum could be more appropriate.

Credit Score Impact

Both HELOCs and home equity loans can affect your credit score. Opening either type of account may cause a temporary dip in your score due to the hard inquiry. However, timely payments can positively impact your credit over time.

HELOCs might have a more significant impact on your credit utilization ratio (a key factor in credit scoring). As you draw from your HELOC, your credit utilization increases, potentially affecting your score. With a home equity loan, your utilization remains constant after the initial borrowing.

Tax Implications

The Tax Cuts and Jobs Act of 2017 changed the tax landscape for both HELOCs and home equity loans. Interest is only tax-deductible if the funds are used to buy, build, or substantially improve the home that secures the loan. The introduction of the Tax Cuts and Jobs Act (TCJA) eliminated deductions on interest if you use the funds for anything else, such as to consolidate debt. A tax professional can provide guidance on how this applies to your specific situation.

Final Thoughts

Your choice between a HELOC and a home equity loan depends on your financial goals and circumstances. HELOCs offer flexibility with variable rates and draw periods, while home equity loans provide fixed rates and lump-sum payouts. You should consider your borrowing needs, risk tolerance, and repayment ability when deciding between a HELOC vs home equity loan.

Both options use your home as collateral, so you must borrow responsibly. Your financial situation, including your credit score and home equity, will play a role in determining which option is available to you and at what terms. We at HELOC360 understand that navigating these choices can be complex.

Our platform simplifies the process, providing you with information and tools to make an informed decision. We connect you with lenders that match your specific needs (helping you unlock the potential of your home equity). You can confidently choose the right home equity product for your unique situation with HELOC360.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.