Avoiding Foreclosure With Your HELOC [Expert Guide]

Table of Contents

HELOC foreclosure is a serious concern for many homeowners. At HELOC360, we understand the stress and uncertainty that can come with managing a home equity line of credit.

This expert guide will provide you with essential strategies to avoid foreclosure and protect your home. We'll explore the unique risks associated with HELOCs, offer practical solutions, and discuss legal options to help you navigate these challenging financial waters.

The Risks of HELOC Foreclosure

Understanding the Unique Nature of HELOCs

Home Equity Lines of Credit (HELOCs) offer homeowners a flexible way to access their home's equity. However, they come with distinct risks that can lead to foreclosure if not managed properly.

HELOCs operate differently from traditional mortgages. They consist of two phases: a draw period and a repayment period. During the draw period (typically up to 10 years), borrowers can access funds as needed and are usually only required to pay interest on what they borrow. When the repayment period starts, borrowers must pay both principal and interest, which can result in a significant increase in monthly payments.

The Federal Reserve reports that many HELOC borrowers make only interest payments during the draw period. This practice can create a financial shock when the repayment period begins, increasing the risk of default.

Common Triggers for HELOC Defaults

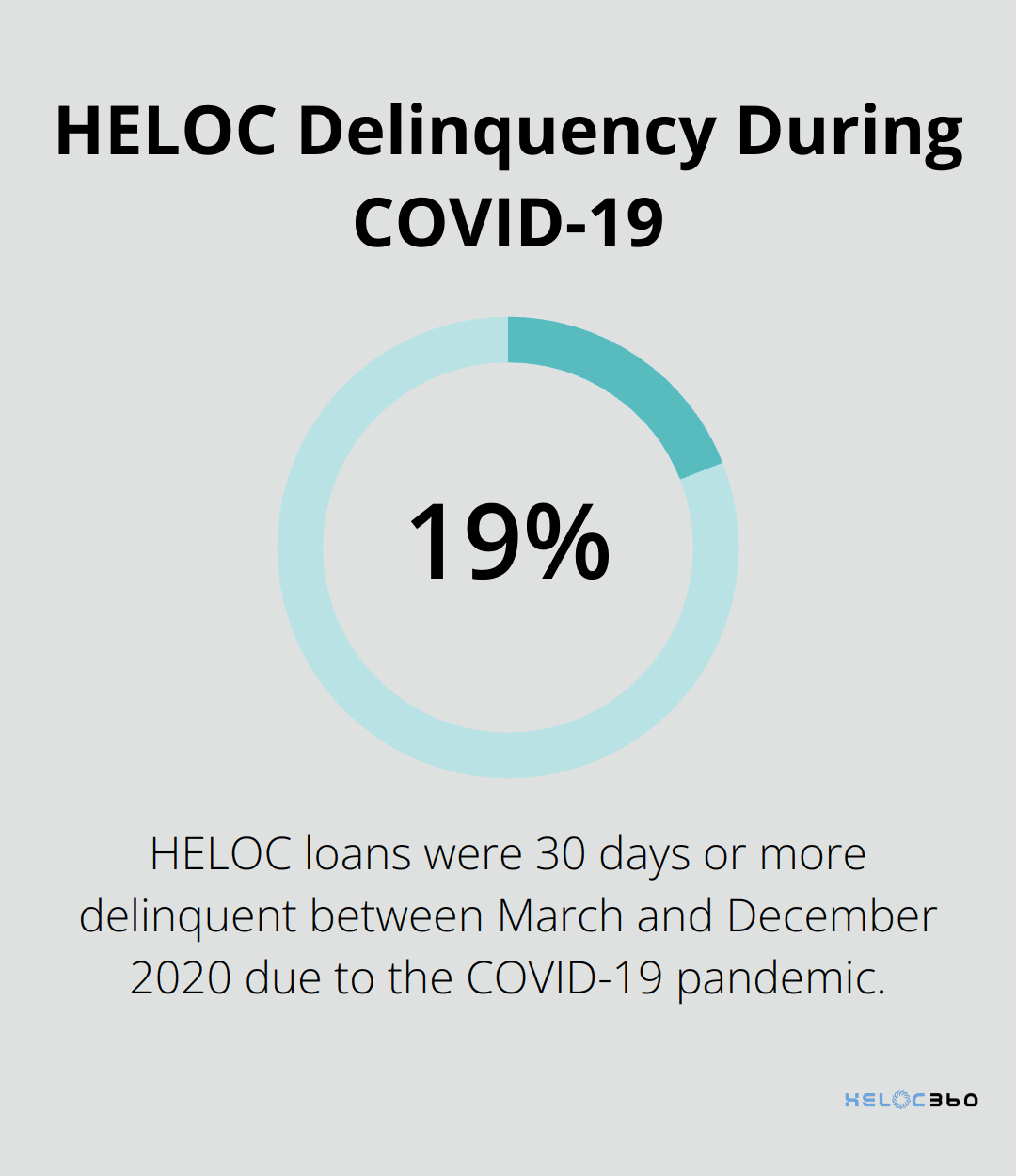

Financial hardships stand as the primary cause of HELOC defaults. Job loss, medical emergencies, or unexpected expenses can quickly impair a homeowner's ability to make payments. The COVID-19 pandemic exemplified this risk, leading to a surge in HELOC delinquencies. A study found that 19% of loans were 30 days or more delinquent at some point between March and December 2020.

Another significant risk factor lies in the adjustable interest rates typical of HELOCs. As interest rates rise, monthly payments increase, potentially stretching budgets to their limits. The Federal Reserve's recent rate hikes have placed many HELOC borrowers in a precarious position.

The HELOC Foreclosure Process

When a HELOC goes into default, the foreclosure process can move swiftly. Unlike first mortgages (which often have more protections and longer timelines), HELOC lenders may initiate foreclosure proceedings after just a few missed payments.

In some states, HELOC lenders can foreclose through a process called "power of sale," which proceeds faster than judicial foreclosure. This means homeowners might have less time to catch up on payments or explore alternatives.

Many homeowners find themselves caught off guard by the speed of HELOC foreclosures. This underscores the importance of understanding your HELOC terms and staying proactive in managing your payments.

As we move forward, we'll explore effective strategies to prevent HELOC foreclosure and protect your home. These methods will help you navigate the challenges associated with HELOCs and maintain financial stability.

How to Prevent HELOC Foreclosure

Communicate Early with Your Lender

Don't wait until you miss payments to contact your lender. If you anticipate financial difficulties, reach out immediately. Many lenders offer hardship programs or temporary payment adjustments, but these options are often more accessible before you fall into delinquency.

A recent proposal by the Consumer Financial Protection Bureau aims to make it easier for homeowners to get help when they are struggling to pay their mortgage.

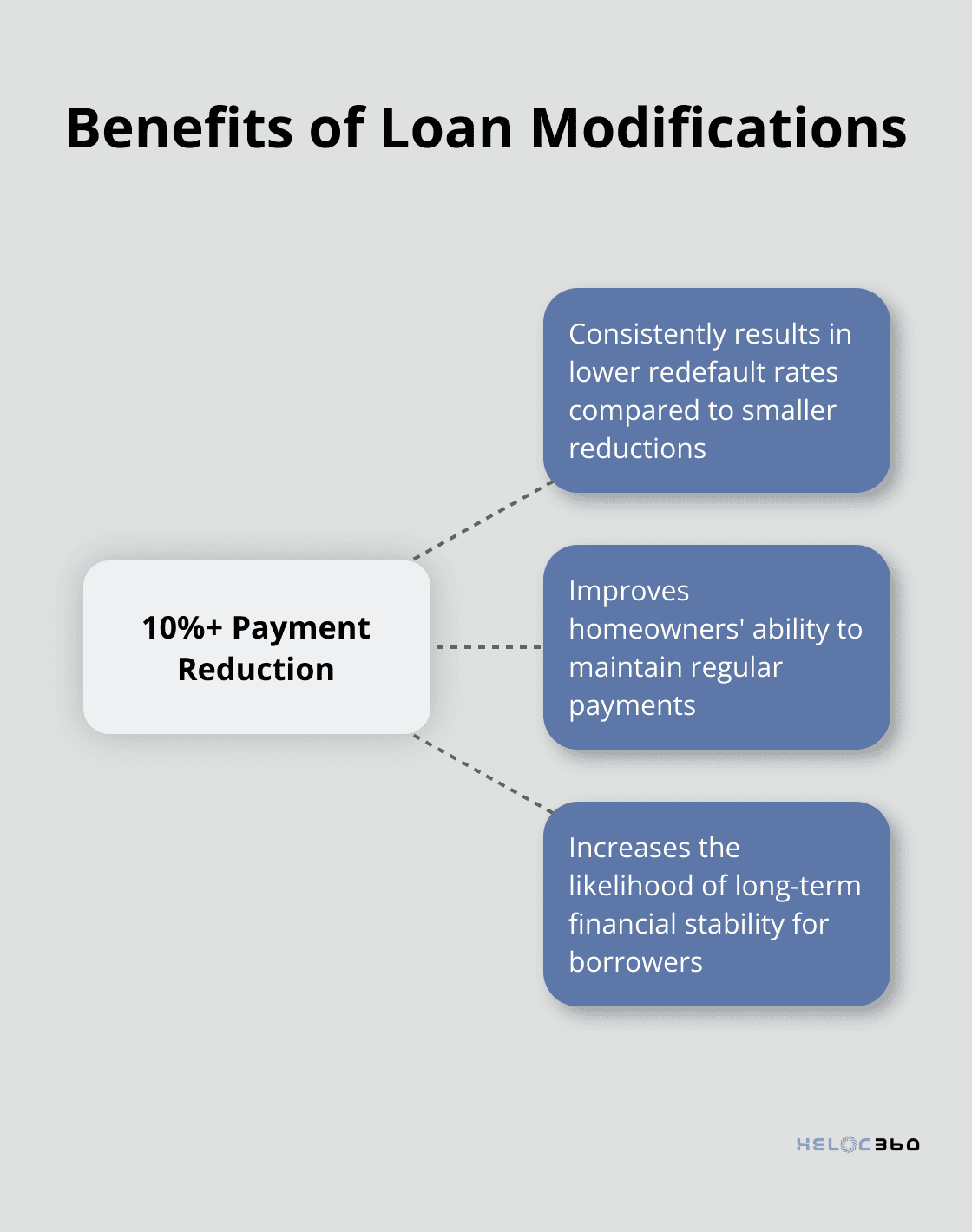

Consider Loan Modification Options

Loan modifications can provide significant relief if you struggle with HELOC payments. These may include:

- Extending the repayment term

- Reducing the interest rate

- Converting a variable-rate HELOC to a fixed-rate loan

Research indicates that modifications reducing mortgage payments by at least 10 percent consistently result in lower redefault rates than modifications that reduce payments by less.

Explore Refinancing Opportunities

Refinancing your HELOC can be a game-changer, especially if you're nearing the end of your draw period. Through refinancing, you might secure a lower interest rate or extend your repayment term, making monthly payments more manageable.

A recent report indicates that refinance candidates could save about $1.6 billion monthly by refinancing - which works out to average savings per borrower of $275 a month.

Prioritize Your HELOC Payments

Create a strict budget that puts your HELOC payments first. Start by analyzing your spending habits and identify areas where you can cut back. The 50-30-20 rule can serve as a helpful guide: allocate 50% of your income to needs (including HELOC payments), 30% to wants, and 20% to savings or debt repayment.

Financial advisor Dave Ramsey suggests using the "debt snowball" method to tackle multiple debts. This involves paying minimum amounts on all debts except the smallest, which you attack with all available funds. Once that's paid off, move to the next smallest debt. This method can help you build momentum and stay motivated.

Your home is likely your most valuable asset. Protecting it should top your priority list. These strategies can significantly reduce your risk of HELOC foreclosure and maintain financial stability. However, sometimes legal options and protections become necessary. Let's explore these in the next section to ensure you're fully equipped to handle any HELOC challenges that may arise.

Legal Safeguards Against HELOC Foreclosure

Understanding Your Foreclosure Rights

State laws govern foreclosure processes, and they vary widely. In California, lenders must contact borrowers at least 30 days before filing a notice of default. Florida requires lenders to file a lawsuit to foreclose, which gives homeowners more time to respond.

The federal government also provides protections. The Truth in Lending Act gives borrowers a three-day right of rescission for most home equity loans. This means you can cancel the transaction within three business days without penalty.

Exploring Bankruptcy as a Last Resort

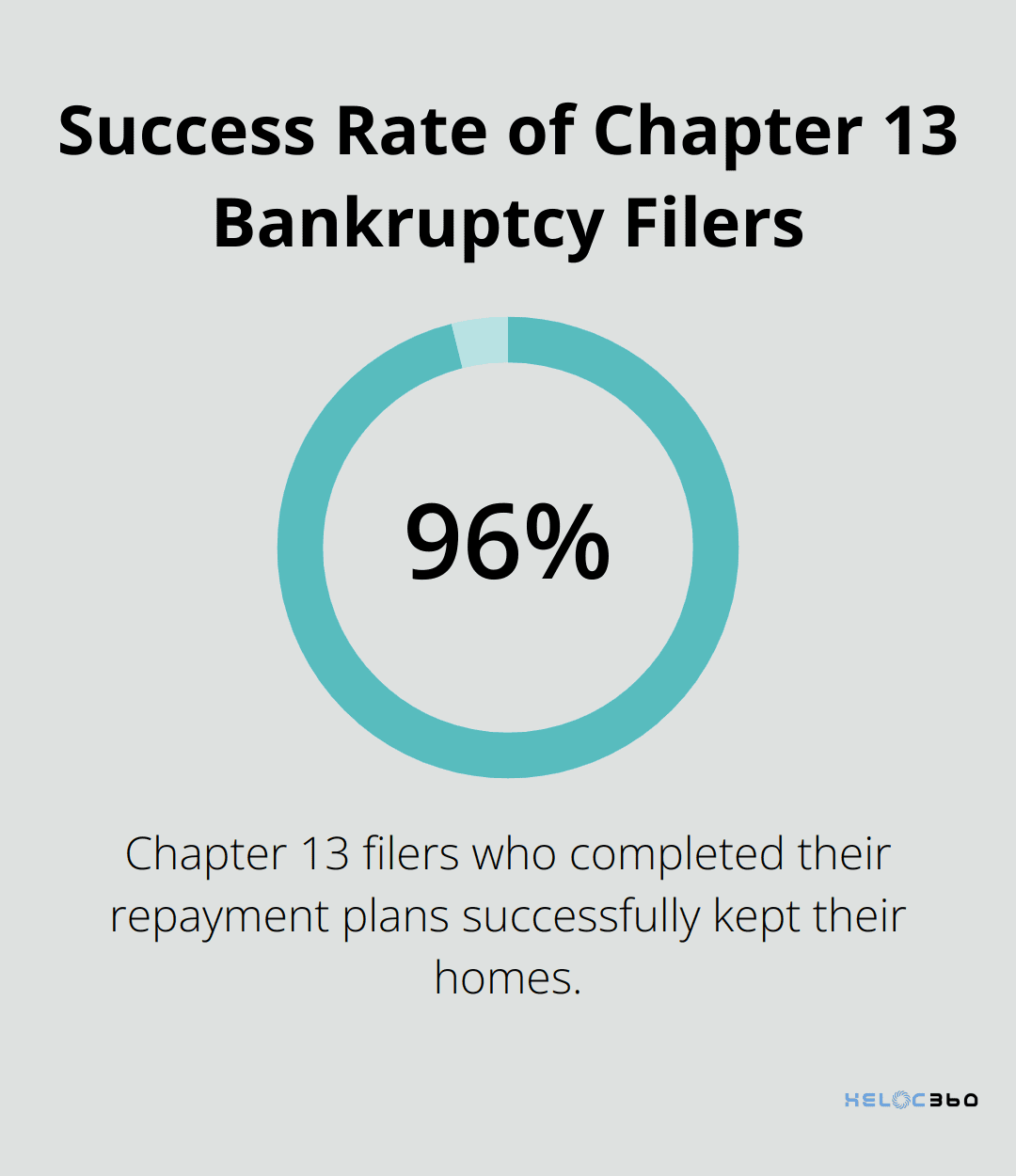

Bankruptcy can be an effective tool to stop foreclosure proceedings, but it should be considered a last resort. Chapter 13 bankruptcy allows homeowners to restructure their debts and create a repayment plan.

The American Bankruptcy Institute reports that about 96% of Chapter 13 filers who completed their repayment plans kept their homes. However, bankruptcy has long-lasting consequences on your credit score and financial future (often lasting up to 10 years). You should consult with a bankruptcy attorney before proceeding with this option.

Seeking Help from Housing Counselors

HUD-approved housing counselors provide invaluable guidance when you navigate HELOC foreclosure. These professionals offer free or low-cost advice on various options, including loan modifications and foreclosure alternatives.

A study by the Urban Institute found that homeowners who received counseling were 2.83 times more likely to receive a loan modification than those who didn't. Additionally, counseled homeowners were 70% more likely to remain current on their mortgage nine months after receiving a loan modification.

Utilizing Foreclosure Mediation Programs

Many states offer foreclosure mediation programs to help homeowners and lenders find mutually beneficial solutions. These programs bring both parties together with a neutral third party to discuss alternatives to foreclosure.

A report from the National Consumer Law Center found that foreclosure mediation programs have helped participating homeowners avoid foreclosure. These programs can lead to loan modifications, repayment plans, or other alternatives that allow homeowners to keep their properties.

Leveraging Consumer Protection Laws

Several federal laws protect homeowners from unfair lending practices. The Real Estate Settlement Procedures Act (RESPA) requires lenders to provide clear and timely information about your loan. The Fair Debt Collection Practices Act (FDCPA) protects you from abusive debt collection practices.

You should familiarize yourself with these laws (and others like them) to ensure your rights are protected throughout the foreclosure process. If you believe a lender has violated these laws, you can file a complaint with the Consumer Financial Protection Bureau.

When you default on HELOC payments, the lender may start foreclosure proceedings. The foreclosure process duration varies by state, with some taking longer than others. It's crucial to understand your rights and options to potentially avoid or delay foreclosure.

Final Thoughts

HELOC foreclosure presents significant challenges, but homeowners can protect their assets with the right strategies. Early communication with lenders, exploration of loan modifications, and consideration of refinancing options serve as powerful tools to prevent foreclosure. Prioritization of HELOC payments within a well-structured budget proves vital for long-term financial stability.

Legal safeguards provide additional protection for homeowners facing HELOC foreclosure. Understanding rights under state and federal laws, exploration of bankruptcy as a last resort, and guidance from HUD-approved housing counselors can make a significant difference. Foreclosure mediation programs and consumer protection laws further empower homeowners in their efforts to keep their homes.

HELOC360 understands the challenges homeowners face when managing home equity lines of credit. Our platform helps you unlock the full potential of your home equity while providing expert guidance to navigate HELOC complexities. HELOC360 offers tailored solutions to meet your unique needs and goals, whether you want to fund renovations, consolidate debt, or create financial flexibility.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.