Understanding the Risks and Rewards of HELOCs

Table of Contents

Home Equity Lines of Credit (HELOCs) offer homeowners a unique way to tap into their property's value. However, understanding HELOC risks is essential before making any financial decisions. At HELOC360, we've seen firsthand how HELOCs can be both beneficial and challenging for homeowners. This post will explore the potential rewards and pitfalls of using a HELOC, helping you make an informed choice about whether it's the right option for your financial needs.

What Exactly Is a HELOC?

Definition and Basic Concept

A Home Equity Line of Credit (HELOC) allows homeowners to borrow against the equity they've built in their property. Unlike traditional loans that provide a lump sum, a HELOC functions more like a credit card, offering ongoing access to funds. It's a revolving line of credit, allowing you to borrow more than once.

How HELOCs Work

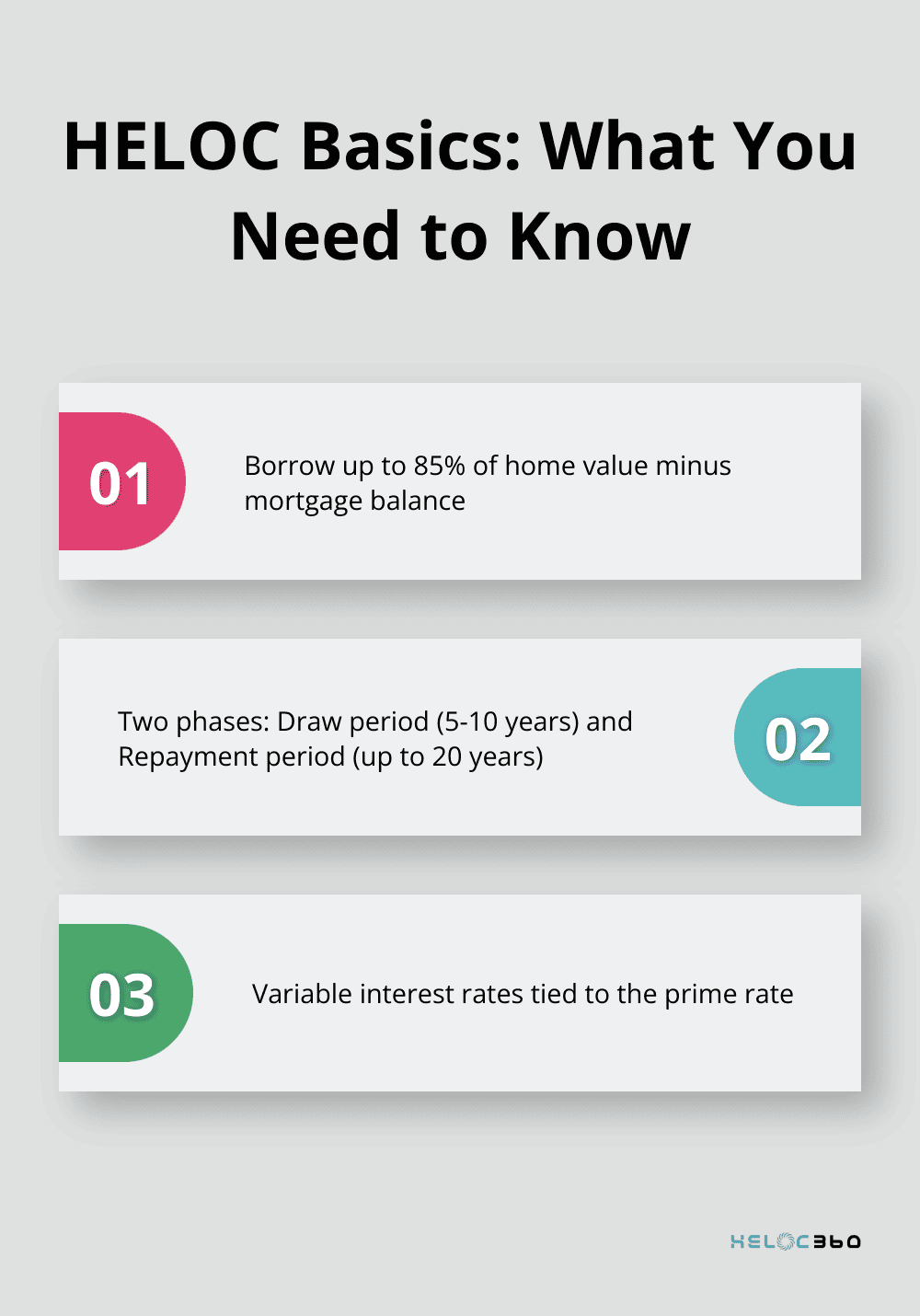

When you receive approval for a HELOC, the lender establishes a credit limit based on your home's value and your outstanding mortgage balance. Most lenders allow borrowing up to 85% of your home's appraised value, minus your remaining mortgage balance. For instance, if your home is worth $300,000 and you owe $200,000 on your mortgage, you might qualify for a HELOC of up to $55,000 (85% of $300,000 = $255,000, minus $200,000 = $55,000).

HELOC Terms and Features

HELOCs typically have two phases: the draw period and the repayment period. The draw period usually lasts 5-10 years, during which you can borrow funds as needed, often making interest-only payments. The repayment period follows, lasting up to 20 years, where you pay back both principal and interest. A key feature of HELOCs is their variable interest rates. These rates often tie to the prime rate, which means your payments can fluctuate over time. As of January 2025, HELOC rates have tumbled, with 15-year home equity loans at 8.49% and 10-year home equity loans at 8.55%.

HELOCs vs Traditional Loans

Unlike personal loans or credit cards, HELOCs use your home as collateral. This secured nature often results in lower interest rates compared to unsecured debt options. However, it also puts your home at risk if you default on payments. Another difference lies in the flexibility of borrowing. With a HELOC, you only pay interest on the amount you actually use, not the entire credit line. This can benefit you if you're unsure about how much money you'll need or if you plan a long-term project with varying expenses.

Risks and Considerations

While HELOCs offer benefits, they also come with risks. The variable interest rates can lead to higher payments if rates rise, and the easy access to funds might tempt some homeowners to overspend. Your financial situation requires careful consideration before deciding if a HELOC suits your needs. As we move forward, let's explore the potential rewards that make HELOCs an attractive option for many homeowners, despite these inherent risks.

Why HELOCs Appeal to Homeowners

Flexible Borrowing and Repayment

HELOCs allow homeowners to borrow only what they need, when they need it. This feature proves particularly useful for ongoing projects or unexpected expenses. Typically, HELOCs will have lower interest rates and greater payment flexibility, but if you need all the money at once, a home equity loan is better. Consider a kitchen renovation. The National Association of Home Builders reports that the average kitchen remodel costs $78,000 (as of 2024). With a HELOC, homeowners can access funds incrementally, matching their spending to the project timeline. This approach can result in significant interest savings compared to borrowing a lump sum upfront.

Cost-Effective Borrowing

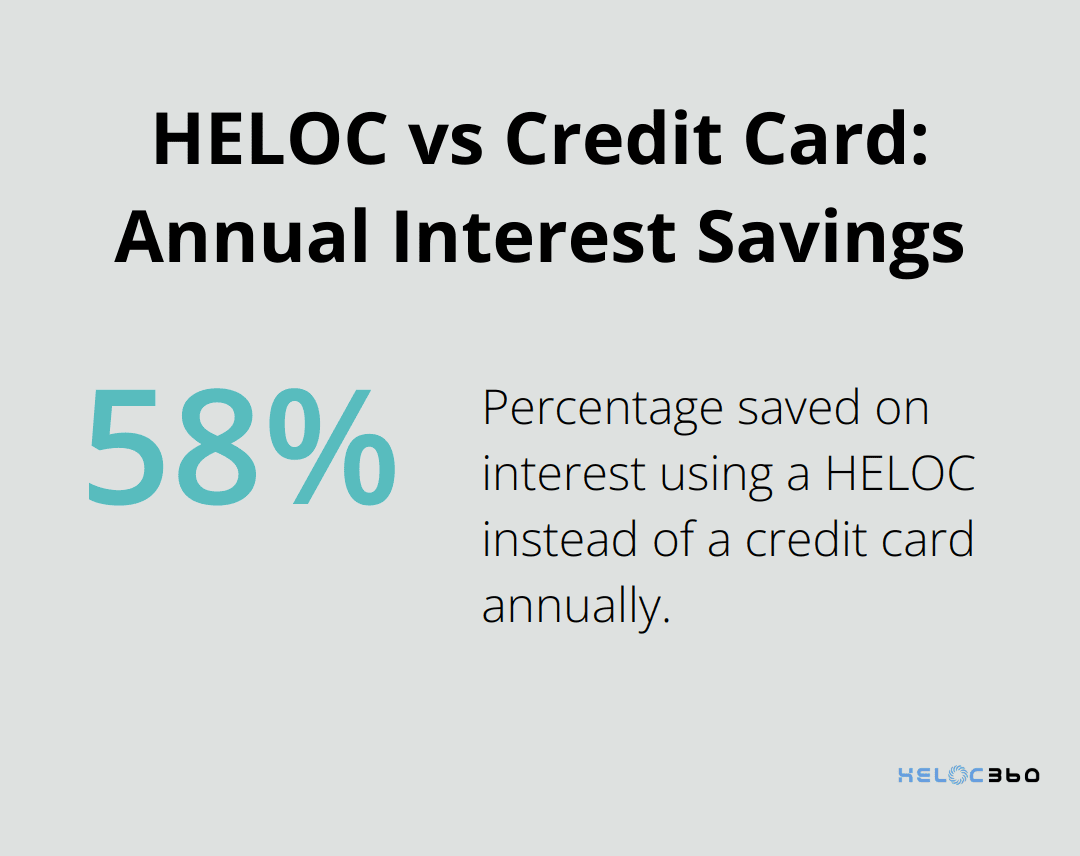

HELOCs typically offer lower interest rates than credit cards and personal loans. As of January 2025, HELOC rates are forecasted to continue falling, with the average HELOC expected to reach 7.25 percent by the end of the year, a low not seen since 2022. This difference translates to substantial savings. For a $50,000 loan, the interest over a year would amount to approximately $4,275 with a HELOC, compared to $10,370 with a credit card. That's a potential saving of over $6,000 in just one year.

Potential Tax Advantages

As of 2025, the interest paid on a HELOC may be tax-deductible if the funds are used for home improvements. However, homeowners should consult with a tax professional to understand the current regulations and how they apply to their specific situation. The IRS provides guidelines on what qualifies as a home improvement for tax deduction purposes. These generally include projects that add value to the home, prolong its useful life, or adapt it to new uses.

Access to Substantial Funds

HELOCs often provide access to larger amounts of money compared to other forms of credit. Most lenders enforce a maximum LTV ratio between 80% and 85%, although some may offer higher limits. For a home worth $300,000 with a $200,000 mortgage balance, a homeowner might qualify for a HELOC of up to $55,000. This access to substantial funds makes HELOCs an attractive option for major expenses such as home renovations, debt consolidation, or education costs. While HELOCs offer numerous benefits, they also come with potential risks. The next section will explore these risks in detail, providing a balanced view to help homeowners make informed decisions about leveraging their home equity.

What Are the Hidden Dangers of HELOCs?

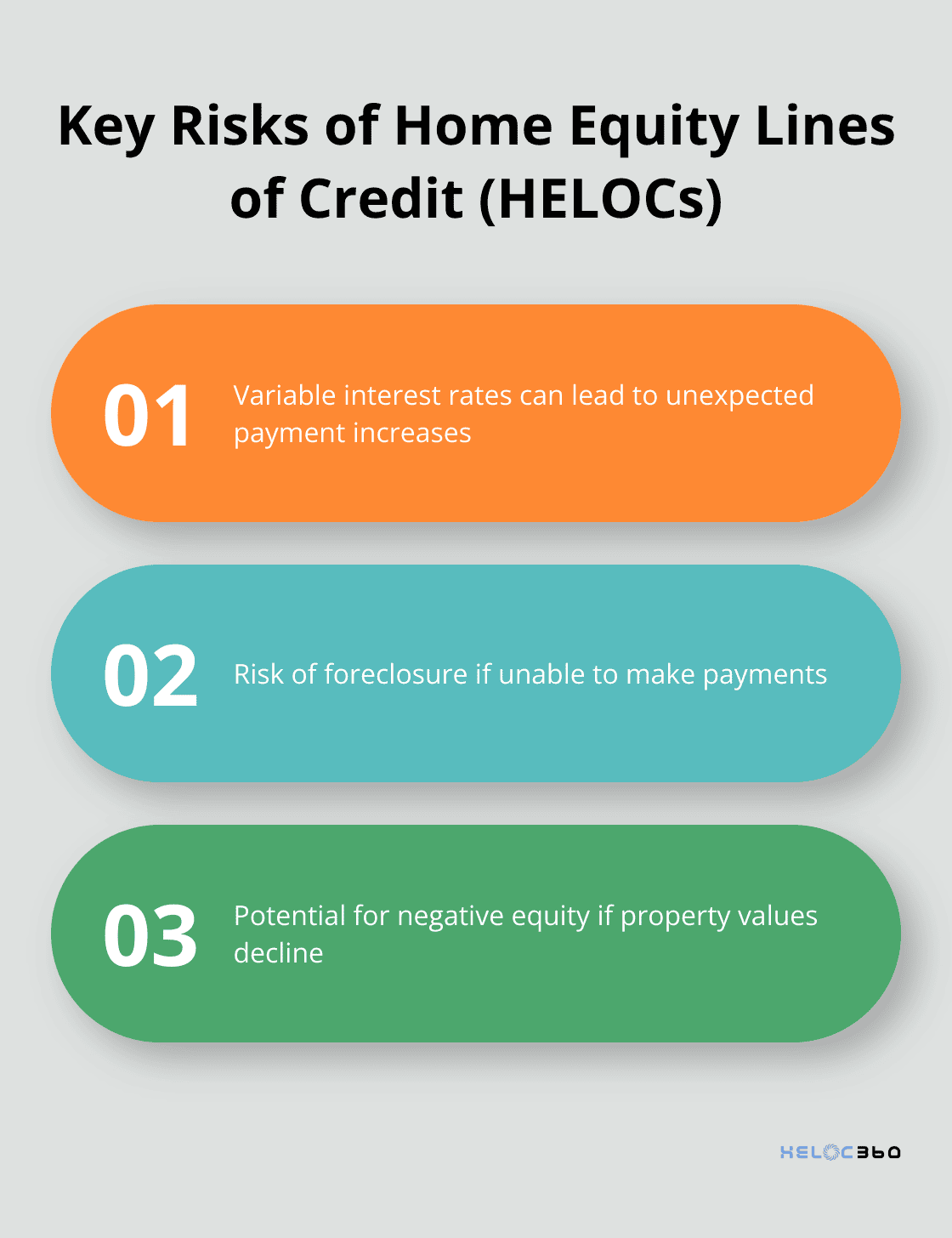

HELOCs can be a double-edged sword for homeowners. While they offer flexibility and access to funds, they also come with significant risks that can jeopardize your financial stability and even your home ownership.

The Unpredictable Nature of Variable Interest Rates

One of the most significant risks of HELOCs is their variable interest rates. These rates typically tie to the Prime rate, which means your payment will rise or fall as the Prime rate does. This volatility can lead to unexpected increases in your monthly payments.

The Looming Threat of Foreclosure

The most severe risk associated with HELOCs is the potential for foreclosure. Your home serves as collateral for the loan, so failing to make payments can result in losing your property. However, as of Q4 2024, foreclosures are ultra-low, with the number of consumers with foreclosures declining to 41,220.

The Slippery Slope of Overspending

The easy access to funds that HELOCs provide can lead to a temptation to overspend. This behavior can lead to a cycle of debt that's difficult to break. To avoid this pitfall, create a strict budget for your HELOC funds before you start spending. Allocate the money to specific purposes and resist the urge to use it for discretionary expenses.

The Danger of Negative Equity

If property values decline, you could end up owing more on your home than it's worth - a situation known as negative equity or being "underwater" on your mortgage. Negative equity can be a significant risk, with research finding that about 40 percent of new mortgage defaults during the housing crisis were driven by active home equity extraction. Before taking out a HELOC, research your local real estate market trends. Look at historical data and future projections to gauge the stability of home values in your area.

Final Thoughts

HELOCs offer homeowners a powerful financial tool, but they come with both advantages and risks. The flexibility to access funds as needed and potentially lower interest rates compared to other forms of credit make HELOCs attractive for many. However, variable interest rates, foreclosure risk, and potential overspending require careful consideration. Weighing these pros and cons is crucial before deciding to tap into your home equity. It's essential to have a clear purpose for the funds and a solid repayment plan in place. Your home is on the line, so treat a HELOC with the same seriousness as your primary mortgage. For homeowners who want to navigate the complexities of HELOCs, HELOC360 offers valuable assistance. Our platform provides comprehensive solutions tailored to your specific financial goals (we simplify the process, offer expert guidance, and connect you with lenders that match your unique needs). A HELOC can be a valuable financial tool when used wisely.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.