At HELOC360, we’ve seen how a well-executed HELOC strategy can be a game-changer for wealth building.

Home Equity Lines of Credit (HELOCs) offer a unique opportunity to leverage your home’s value for strategic investments. From real estate ventures to business expansion, HELOCs can fuel various wealth-building initiatives.

In this post, we’ll explore how to use HELOCs effectively, manage risks, and maximize your financial potential.

What Is a HELOC and How Can It Build Wealth?

Understanding HELOCs

A Home Equity Line of Credit (HELOC) allows homeowners to borrow against the equity they’ve built in their property. It functions like a revolving credit line, similar to a credit card, but uses your home as collateral. HELOCs have the most flexibility in terms of how much you can borrow and when you can pay it off, compared with other home equity products. This unique structure offers several advantages for wealth building, but it also comes with risks.

The Mechanics of HELOCs

When you open a HELOC, your lender approves you for a maximum credit limit based on your home’s value and your outstanding mortgage balance. You can draw from this credit line as needed during the draw period (typically 5-10 years). During this time, you often only need to make interest payments on the borrowed amount.

After the draw period ends, you enter the repayment period. You can no longer borrow and must repay both principal and interest. This period usually lasts 10-20 years.

Advantages for Wealth Building

HELOCs offer several benefits that make them attractive for wealth-building strategies:

- Lower interest rates: HELOCs often have lower interest rates compared to unsecured loans or credit cards.

- Flexibility: You only pay interest on the amount you actually borrow, not your entire credit limit. This allows for more strategic use of funds.

- Potential tax benefits: While tax laws have changed, interest on HELOCs used for home improvements may still be tax-deductible. (Always consult a tax professional for specifics.)

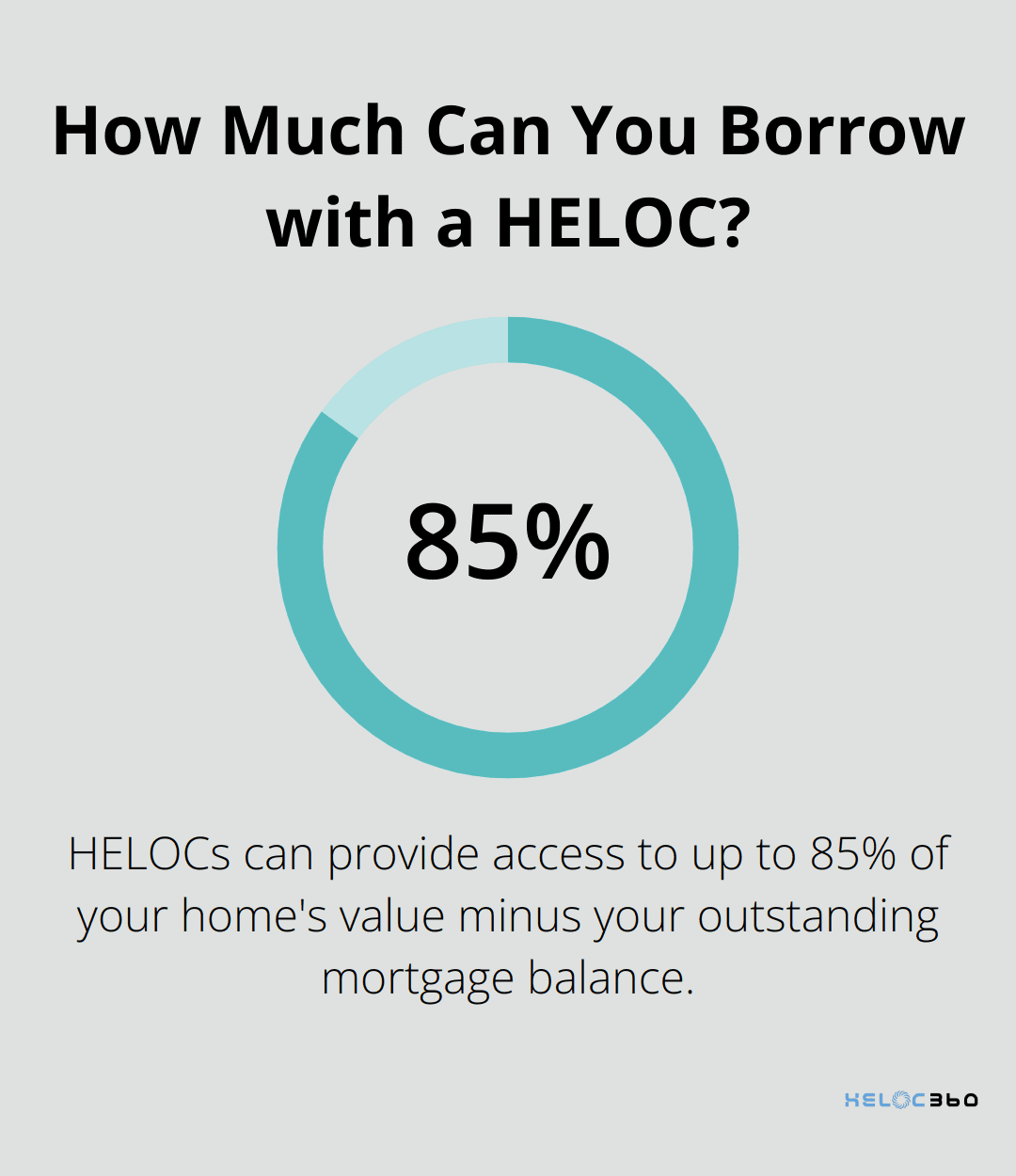

- Access to large sums: HELOCs can provide access to significant amounts of capital, often up to 85% of your home’s value minus your outstanding mortgage balance.

Risks and Considerations

While HELOCs can be powerful wealth-building tools, they come with risks:

- Variable interest rates: Most HELOCs have variable rates, which means your payments could increase if rates rise. As of Mar. 5, 2025, the current average HELOC interest rate is 8.06 percent.

- Potential for overleverage: Easy access to funds can lead to overextension if not managed carefully.

- Foreclosure risk: Since your home is collateral, defaulting on HELOC payments could result in foreclosure.

- Market fluctuations: A decrease in home values could reduce your available credit or even result in owing more than your home is worth.

To mitigate these risks, you must have a solid repayment plan and use HELOC funds strategically. Many financial experts recommend using HELOCs for investments that have the potential to generate returns higher than the interest rate you’re paying.

Strategic Uses of HELOCs

Using a HELOC to fund a home renovation that increases your property value by 20% could be a smart move. Similarly, using HELOC funds as seed money for a business with strong growth potential could pay off significantly.

However, using a HELOC for everyday expenses or depreciating assets like cars is generally not advisable from a wealth-building perspective.

Some clients have successfully used HELOCs to fund real estate investments, start businesses, or even invest in high-yield dividend stocks. The key is to have a clear strategy and understand both the potential rewards and risks involved.

Now that we’ve covered the basics of HELOCs and their potential for wealth building, let’s explore specific investment opportunities that can maximize your HELOC’s potential.

Maximizing Your HELOC for Strategic Investments

Real Estate Investments

Real estate remains one of the most popular investment choices for HELOC users. You can use your HELOC for house flipping or building a rental property portfolio.

For house flipping, a HELOC can cover renovation costs quickly. This allows you to take advantage of time-sensitive opportunities. The National Association of REALTORS® reports that median existing-home sale prices rose 14.6% in 2021, which makes house flipping an attractive option for many investors.

Rental properties offer another avenue for wealth building. You can use your HELOC as a down payment on a rental property to expand your real estate portfolio without tying up all your liquid assets. Zillow’s Observed Rent Index (ZORI) provides a smoothed measure of typical observed market rate rents across regions, which can be useful for assessing potential rental income.

Business Expansion

For entrepreneurs, a HELOC can provide quick access to funds for starting or expanding a business. Unlike traditional business loans, which often require extensive paperwork and can take months to approve, a HELOC offers immediate liquidity.

The U.S. Small Business Administration reports that 20% of businesses fail in their first year, often due to lack of capital. A HELOC can provide the necessary cushion to weather initial challenges and fuel growth.

Some business owners use their credit line to purchase inventory in bulk, which reduces costs and increases profit margins. Others fund marketing campaigns that significantly expand their customer base within a short period.

Stock Market Investments

While investing borrowed money in the stock market carries risks, it can be a viable strategy for some. High-yield dividend stocks or ETFs can provide regular income to cover HELOC interest payments while potentially appreciating in value.

Historical data suggests that staying invested for longer periods can increase the probability of achieving positive returns.

However, stock market investments can be volatile. You should always consult with a financial advisor before implementing this strategy.

Education and Career Advancement

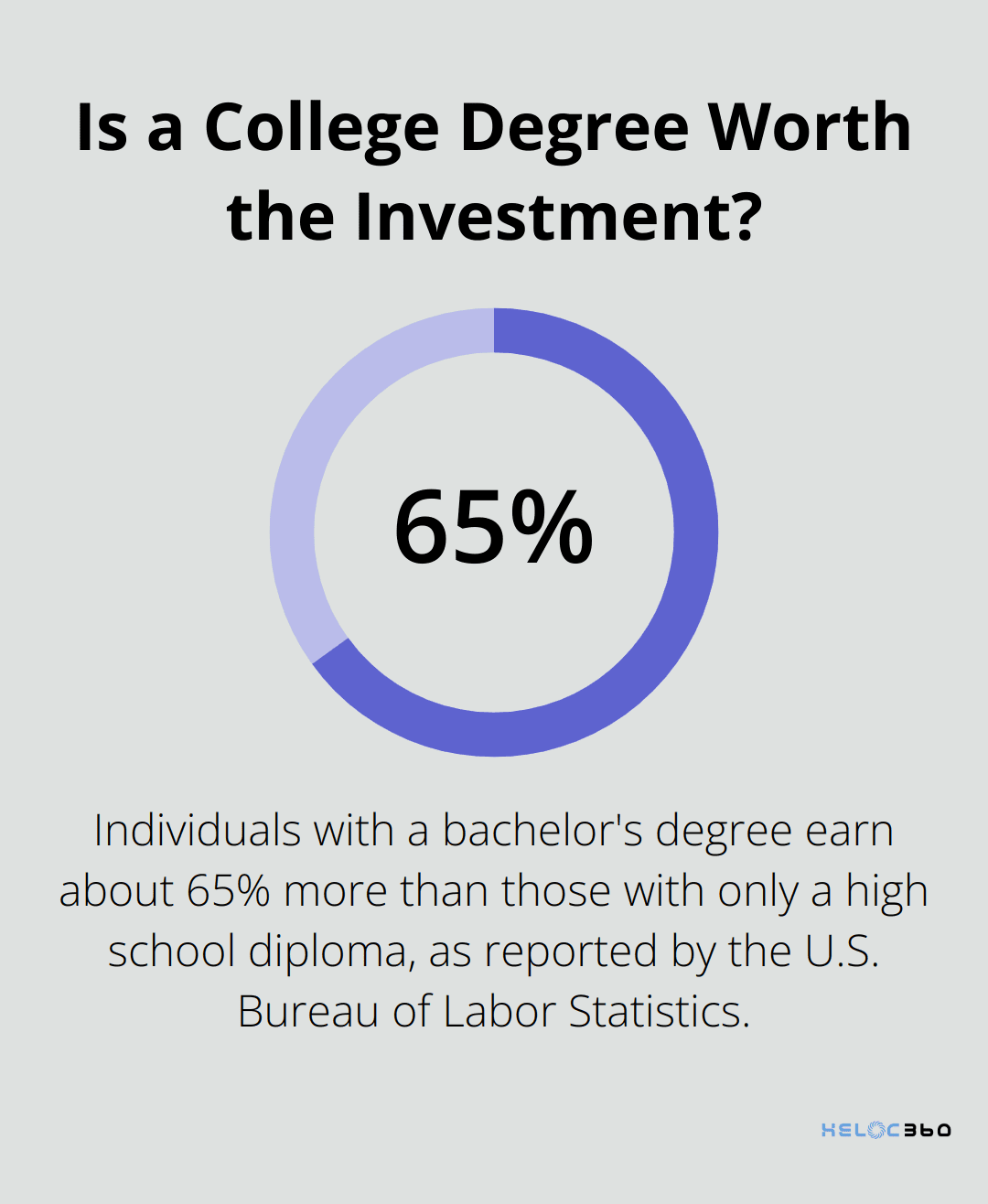

Investing in education can significantly boost your earning potential. The U.S. Bureau of Labor Statistics reports that individuals with a bachelor’s degree earn about 65% more than those with only a high school diploma.

You can use a HELOC to fund further education or professional certifications. Unlike student loans, HELOCs often offer lower interest rates and more flexible repayment terms.

Some individuals have funded MBA programs with their HELOC, leading to promotions and substantial salary increases within a few years of graduation. These salary boosts can more than cover the HELOC payments and accelerate wealth-building journeys.

While these strategies can be effective, they all come with risks. You must have a solid plan in place and understand the potential downsides before using your HELOC for any investment. The next section will explore best practices for managing your HELOC to maximize its wealth-building potential while minimizing risks.

How to Manage Your HELOC Effectively for Wealth Building

Create a Robust Repayment Plan

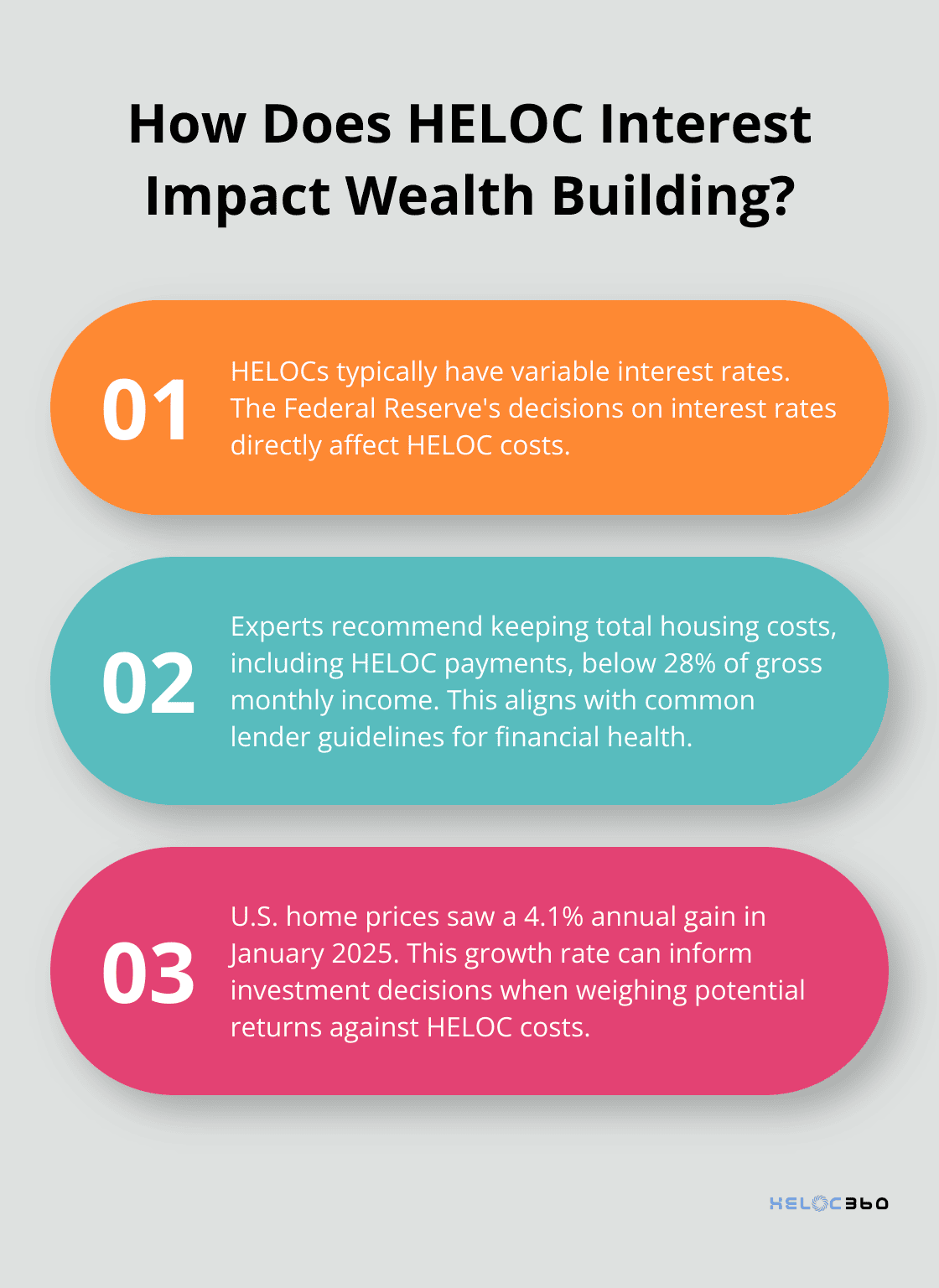

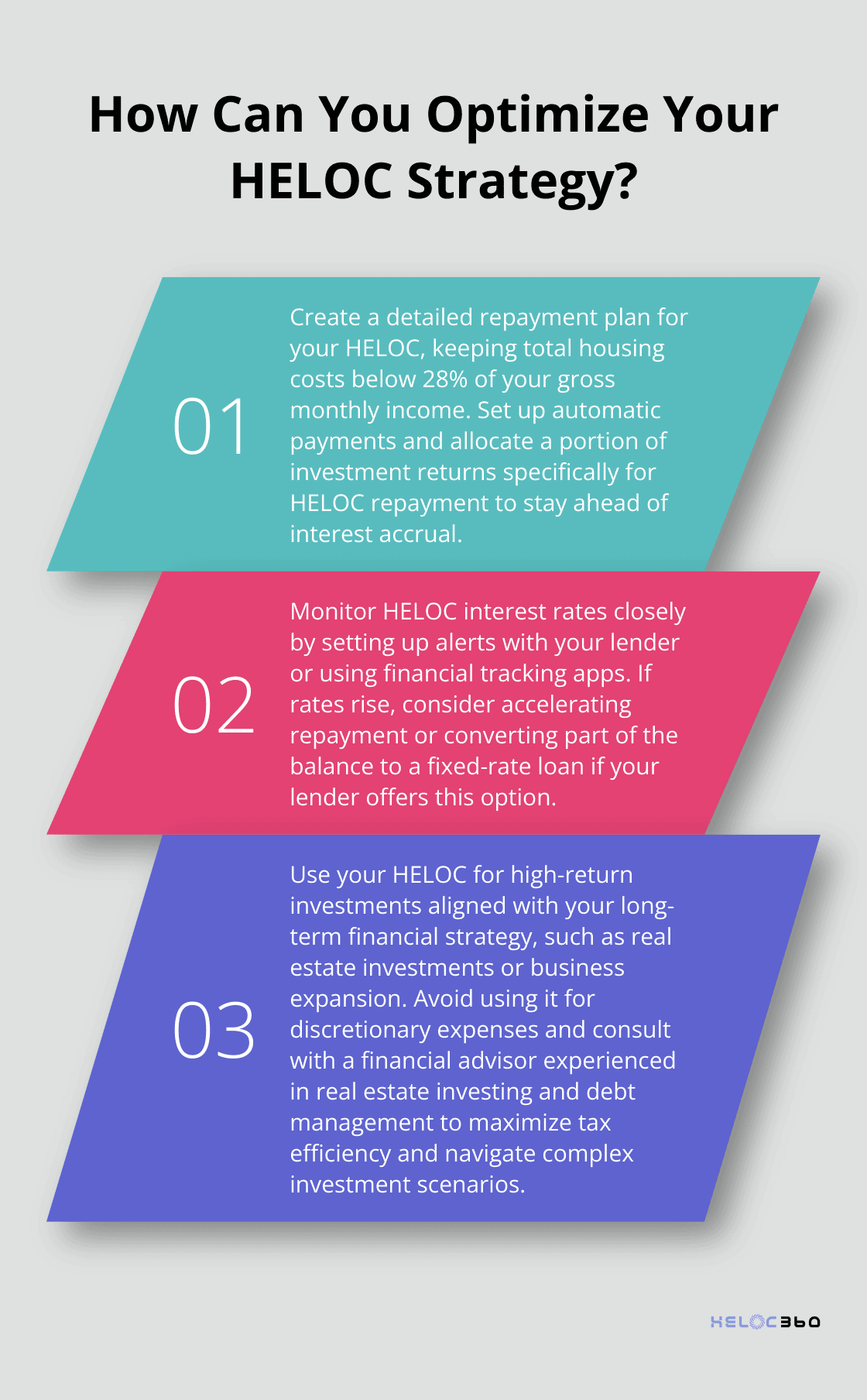

Effective HELOC management starts with a solid repayment plan. Calculate your total monthly expenses, including current mortgage payments and potential HELOC withdrawals. Try to keep your total housing costs (including HELOC payments) below 28% of your gross monthly income. This percentage aligns with guidelines often used by lenders.

Set up automatic payments to avoid missing due dates. While many HELOC providers offer interest-only payments during the draw period, we recommend paying more than the minimum whenever possible to reduce your principal balance.

Allocate a portion of any investment returns or additional income specifically for HELOC repayment. This strategy will help you stay ahead of interest accrual and build equity faster.

Monitor Interest Rates Closely

HELOCs typically come with variable interest rates, so you must keep a close eye on rate fluctuations. The Federal Reserve’s decisions on interest rates can directly impact your HELOC costs. Home equity loan rates are impacted by changes in the federal funds rate, which the Fed adjusts to influence economic conditions.

Set up alerts with your lender or use financial tracking apps to monitor rate changes. If rates rise, consider accelerating your repayment or explore options to convert part of your HELOC balance to a fixed-rate loan (if your lender offers this option).

In a falling rate environment, you might find opportunities to borrow more cheaply for strategic investments. However, always weigh the potential returns against the cost of borrowing.

Align HELOC Usage with Your Financial Goals

Balance HELOC use with your other financial objectives. Prioritize high-return investments that align with your long-term financial strategy.

For instance, if you use your HELOC for real estate investments, consider how this fits with your retirement planning or your children’s education funds. U.S. home prices posted a 4.1% annual gain in January, up marginally from 3.9% annual growth in December. This growth rate can inform your investment decisions and help you gauge potential returns against your HELOC costs.

Avoid using your HELOC for discretionary expenses or investments with uncertain returns. Instead, focus on opportunities that have a high probability of generating returns exceeding your HELOC’s interest rate.

Leverage Professional Advice

Working with financial advisors is often a smart move to navigate the complexities of HELOC management and wealth-building strategies. A financial planner is a type of financial advisor who specializes in helping you set financial goals and develop strategies to reach them.

Look for advisors with experience in real estate investing and debt management. They can provide valuable insights on market trends, tax implications, and risk management strategies specific to HELOC usage.

A skilled advisor might help you structure your investments to maximize tax efficiency, potentially saving you thousands of dollars annually. They can also help you navigate complex scenarios, such as using your HELOC to invest in a business or fund a major life event.

Final Thoughts

HELOCs offer a powerful tool for wealth building when used strategically and responsibly. You can access funds for high-potential investments like real estate, business expansion, or education by leveraging your home’s equity. A well-executed HELOC strategy can accelerate your wealth-building journey, but it requires diligence and informed decision-making.

Effective HELOC management involves creating a robust repayment plan, monitoring interest rates, and aligning usage with your broader financial goals. You should always consider the potential returns against the costs and risks involved. Your home serves as collateral, so it’s important to approach HELOC usage with a clear plan and realistic expectations.

At HELOC360, we understand the complexities of using home equity for wealth building. Our platform helps homeowners unlock the full potential of their home’s value (through tailored solutions and expert guidance). Whether you’re considering a HELOC for home improvements, debt consolidation, or investment opportunities, HELOC360 can support you in navigating the process with confidence.

Our advise is based on experience in the mortgage industry and we are dedicated to helping you achieve your goal of owning a home. We may receive compensation from partner banks when you view mortgage rates listed on our website.