Are you juggling multiple Home Equity Lines of Credit (HELOCs)? HELOC consolidation might be the solution you’re looking for.

At HELOC360, we’ve seen how combining multiple HELOCs into one can simplify finances and potentially save money. This strategy, however, requires careful planning and execution.

In this post, we’ll explore effective HELOC consolidation strategies and how to implement them for optimal results.

What is HELOC Consolidation?

The Concept of HELOC Consolidation

HELOC consolidation combines multiple Home Equity Lines of Credit into a single loan. This strategy simplifies finances and potentially leads to cost savings.

How HELOC Consolidation Works

When you consolidate your HELOCs, you take out a new loan to pay off your existing lines of credit. This new loan comes with its own interest rate and terms. The objective is to secure more favorable conditions than your current multiple HELOCs.

Advantages of Consolidation

HELOC consolidation offers several benefits. It simplifies your financial life by reducing the number of payments you manage each month. Instead of tracking multiple due dates and amounts, you’ll have a single payment to monitor.

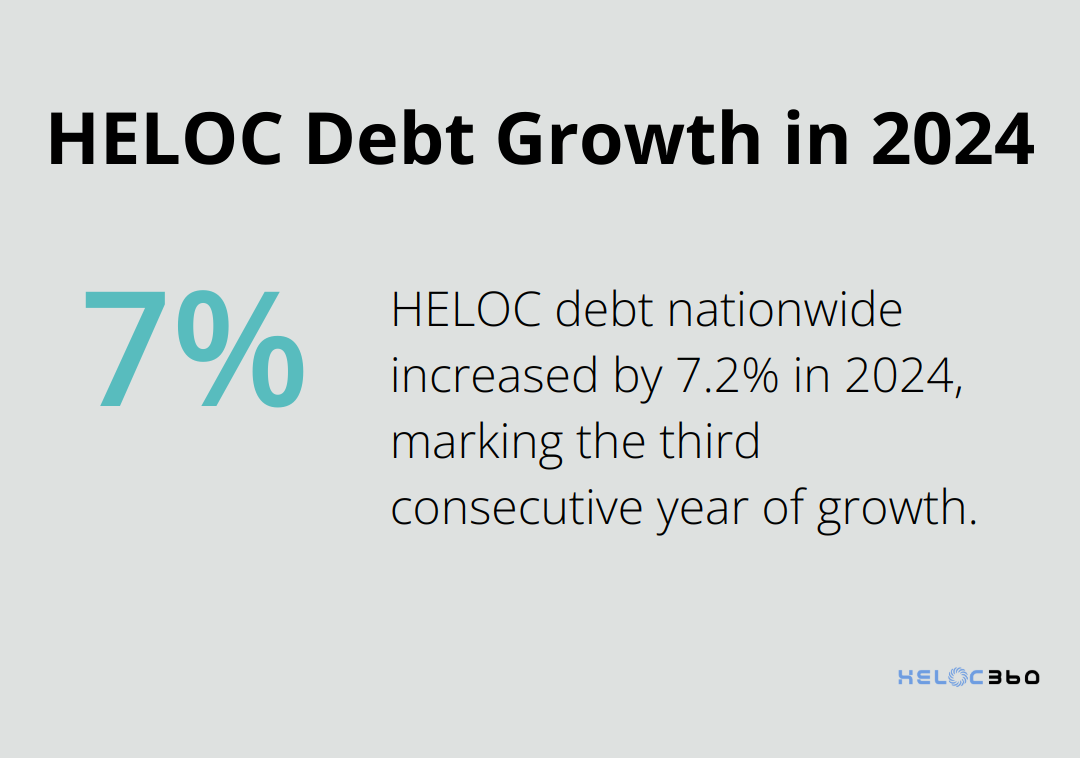

Consolidation can also lead to significant cost savings. If you secure a lower interest rate on your consolidated loan, you’ll pay less in interest over time. HELOC debt nationwide increased by 7.2% in 2024, marking the third consecutive year that HELOC balances have grown after a decade of decline.

Risks to Consider

While HELOC consolidation can benefit many homeowners, it’s not without risks. One major consideration is that you use your home as collateral. If you default on your payments, you could potentially lose your home.

Additionally, consolidation might extend your repayment period. While this could lower your monthly payments, you might end up paying more in interest over the life of the loan. Lenders expect HELOC debt outstanding to increase 2.3 percent in 2024 and 4.8 percent in 2025.

Evaluating if Consolidation is Right for You

The decision to consolidate your HELOCs should stem from a thorough analysis of your financial situation. Consider factors such as your current interest rates, the remaining balances on your HELOCs, and your long-term financial goals.

If you struggle to keep up with multiple HELOC payments or believe you can secure a significantly lower interest rate, consolidation might be a smart move. However, if your current HELOCs already have favorable terms, consolidation might not offer substantial benefits.

Every financial situation is unique (what works for one homeowner might not be the best solution for another). That’s why it’s important to carefully evaluate your options and consider seeking professional advice before making a decision.

Now that we understand what HELOC consolidation is and its potential benefits and risks, let’s explore effective strategies for consolidation in the next section.

How to Maximize Your HELOC Consolidation

Assess Your Current HELOCs

Start your consolidation journey by collecting all information about your existing HELOCs. Note the interest rates, remaining balances, and monthly payments for each line of credit. This step will help you understand your current financial obligations and identify areas for improvement.

A recent study by the Mortgage Bankers Association included benchmarking data related to home equity lending, such as volume, utilization rates, operational metrics, and growth expectations.

Find the Best Rates

After you have a clear picture of your situation, explore your options. Contact multiple lenders to compare interest rates and terms for consolidation loans. Don’t limit your search to traditional banks; credit unions and online lenders often offer competitive rates.

As of June 2025, HELOC rates are not expected to see a drop as the Federal Reserve is projected to keep the federal funds rate the same. However, rates can vary significantly based on your credit score, loan-to-value ratio, and other factors. Try to secure a rate that’s lower than the weighted average of your current HELOCs.

Negotiate with Lenders

Don’t hesitate to negotiate with lenders for better terms. If you have a strong credit score and a history of timely payments, use this as leverage. Some lenders might offer more favorable rates or waive certain fees to win your business.

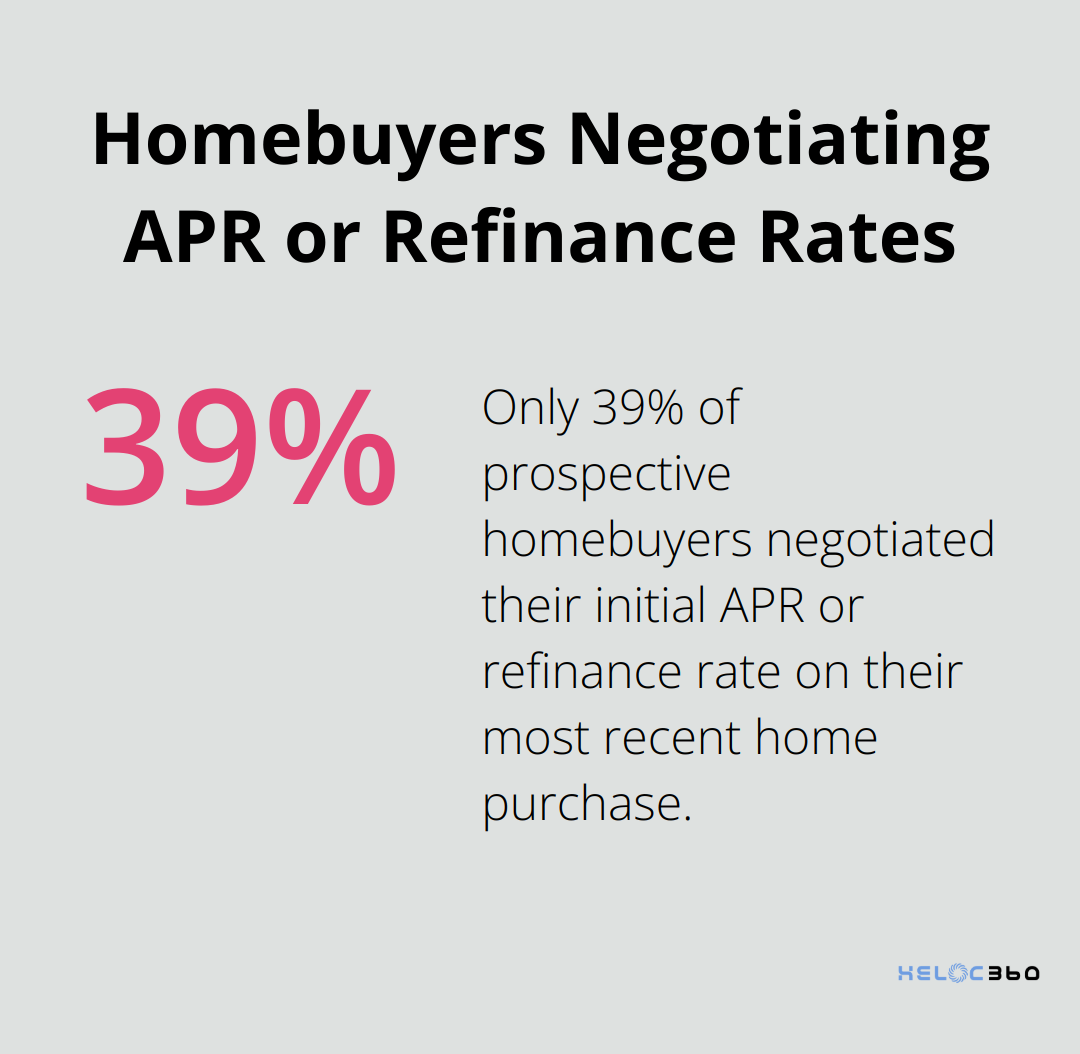

A study by LendingTree found that only 39% of prospective homebuyers negotiated the initial APR or refinance rate on their most recent home purchase, despite the high success rate. This seemingly small difference can translate to thousands of dollars in savings over the life of your loan.

Use Your Home Equity Wisely

Your home equity is a valuable asset, so use it judiciously. The ICE Mortgage Monitor reported that tappable home equity approached $12 trillion in early 2025. While this presents a significant opportunity, it’s important to borrow only what you need.

Consider your long-term financial goals when deciding how much equity to tap into. Avoid the temptation to borrow more than necessary for consolidation, as this could lead to overextending yourself financially.

Leverage Technology for Better Decisions

Modern platforms can help you navigate the consolidation process more effectively. These tools often provide access to multiple lenders, allowing you to compare rates and terms easily. Some even offer personalized recommendations based on your financial profile.

By utilizing such platforms, you can streamline your search for the best consolidation options and make more informed decisions. This approach can save you time and potentially uncover opportunities you might have otherwise missed.

The next step in your HELOC consolidation journey involves implementing your chosen strategy effectively. Let’s explore how to put your plan into action and manage your consolidated HELOC for optimal results.

How to Implement Your HELOC Consolidation Plan

Collect Your HELOC Information

Start your consolidation journey by collecting all necessary information about your existing HELOCs. This includes current balances, interest rates, HELOC minimum payments, and any associated fees. Having this information at hand will streamline the consolidation process and help you make informed decisions.

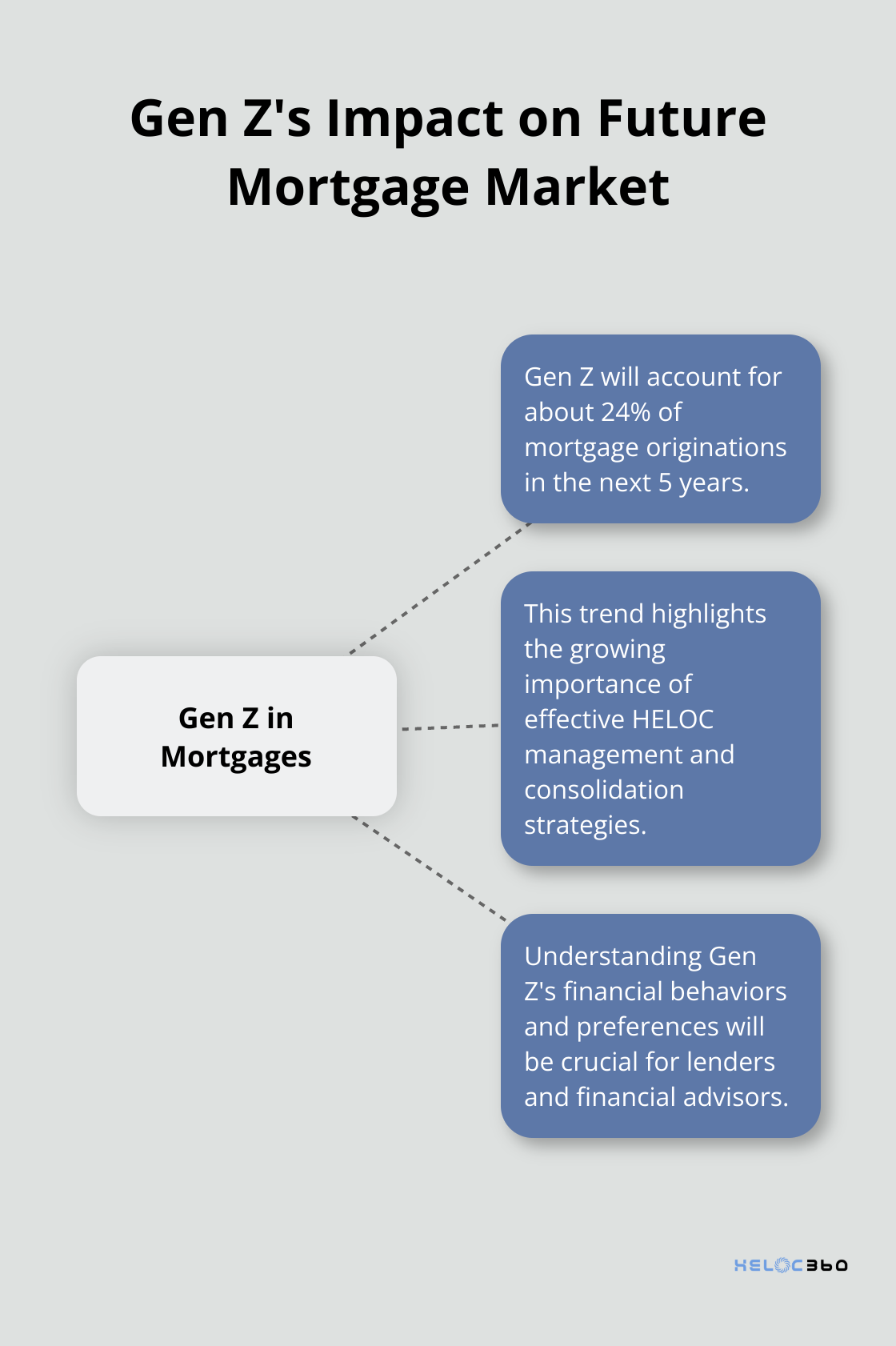

A recent study by the Mortgage Bankers Association revealed that in the next 5 years, Gen Z will account for about 24% of mortgage originations. This trend highlights the growing importance of effective HELOC management and consolidation strategies.

Select Your Consolidation Method

You have several options to consolidate your HELOCs. The most common approach involves taking out a new HELOC or home equity loan to pay off your existing lines of credit. Another option is to refinance your primary mortgage and use the cash-out option to consolidate your HELOCs.

Each method has its advantages and disadvantages. A new HELOC might offer flexibility but come with a variable interest rate, while a home equity loan provides a fixed rate but less flexibility. Your choice should align with your financial goals and risk tolerance.

Submit Your Loan Application

After you choose your consolidation method, apply for your new loan. This process typically requires you to submit financial documents, including proof of income, tax returns, and information about your existing HELOCs.

Close Your Existing HELOCs

Once your new loan receives approval and funding, use the proceeds to pay off your existing HELOCs. Confirm that these lines of credit are fully paid and closed to avoid any potential future charges or complications.

Manage Your Consolidated HELOC

With your consolidation complete, focus on effective management of your new loan. Set up automatic payments to ensure you never miss a due date. If your new loan has a draw period, be mindful of how much you borrow and create a clear plan for repayment.

ICE Mortgage Monitor reported that 48M homeowners sit on $11.5T in tappable equity entering Q2 2025. While this represents significant potential, it’s important to use your home equity judiciously. Try to resist the temptation to overborrow, even if your new consolidated HELOC offers a higher credit limit.

Final Thoughts

HELOC consolidation provides homeowners with a powerful strategy to simplify their finances and potentially save money. This approach combines multiple Home Equity Lines of Credit into a single loan, which can streamline monthly payments and secure more favorable terms. The success of HELOC consolidation depends on careful planning and execution, including a thorough assessment of your current financial situation and comparison of rates from multiple lenders.

Strategic planning plays a vital role in maximizing the benefits of HELOC consolidation. This includes evaluating existing HELOCs, negotiating with lenders for better terms, and selecting the right consolidation method that aligns with your financial goals. HELOC360 offers valuable assistance to homeowners who want to navigate the complexities of HELOC consolidation.

HELOC360 simplifies the process by providing expert guidance and connecting you with lenders that match your specific needs. The platform empowers you to make informed decisions about your home equity, helping you unlock new financial opportunities and achieve your goals. As you consider HELOC consolidation, take the time to carefully evaluate your options and make decisions that align with your long-term financial objectives.

Our advise is based on experience in the mortgage industry and we are dedicated to helping you achieve your goal of owning a home. We may receive compensation from partner banks when you view mortgage rates listed on our website.